Dollar is stabilizing after earlier selloff but remains the weakest performer for the week. Its modest recovery can be partly attributed to a bounce back against Euro, which is currently under pressure due to Germany’s lower-than-expected CPI readings. Meanwhile, Australian Dollar is experiencing a delayed reaction to Australia’s lower-than-expected monthly CPI readings too. As a result, both Aussie and Euro are the worst performers for the day.

On the other hand, the New Zealand Dollar continues to soar, bolstered by RBNZ’s (RBNZ) hawkish holds. Swiss Franc is also showing strength, particularly in its recovery against Euro. Sterling and Canadian Dollar, meanwhile, display mixed performances amidst these currency movements.

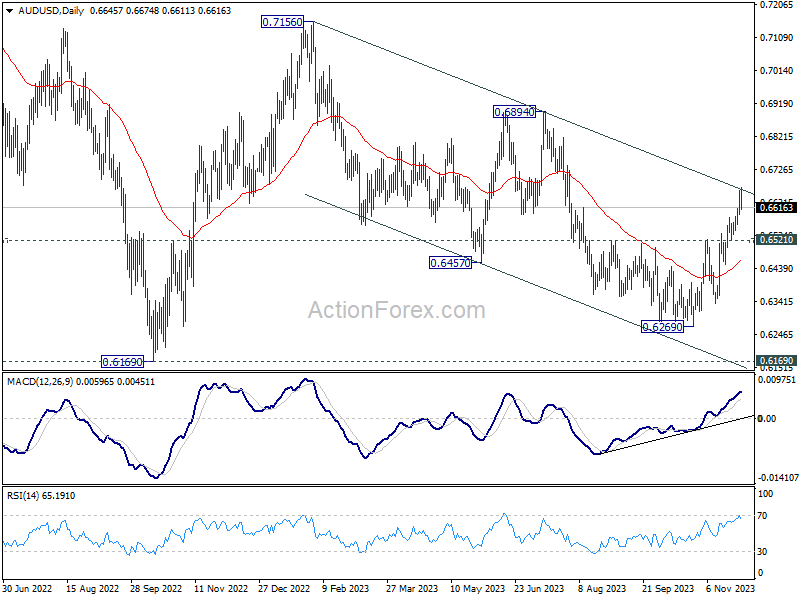

From a technical analysis perspective, AUD/USD is now at a critical juncture, pressing medium term falling channel resistance. Decisive break there will solidify the case that whole fall from 0.7156 has completed with waves down to 0.6269. Further rally should then be seen to 0.6894 resistance.

On the other hand, rejection by the channel resistance at this stage will bring consolidations first. However, break of 0.6521 support will revive medium term bearishness for deeper fall. The upcoming China PMI data, expected tomorrow, could be a significant catalyst for the next move in this currency pair.

In Europe, at the time of writing, FTSE is up 0.02%. DAX is up 1.14%. CAC is up 0.55%. Germany 10-year yield is down -0.040 at 2.456. Earlier in Asia, Nikkei fell -0.26%. Hong Kong HSI fell -2.08%. China Shanghai SSE fell -0.56%. Singapore Strait Times rose 0.61%. Japan 10-year JGB yield fell -0.074 to 0.681.

US goods trade deficit widens to USD -89.8B in Oct

US goods exports fell -1.7% mom to USD 170.8B in October. Goods imports was flat 0.0% mom at 260.7B. Goods trade deficit widened from USD -86.8B to USD -89.8B, larger than expectation of USD -86.7B.

Wholesale inventories fell -0.2% mom to USD 899.4B. Retail inventories was virtually unchanged at USD 796.6B.

Eurozone economic sentiment rose to 93.8, EU rose to 93.7

Eurozone Economic Sentiment Indicator ticked up from 93.5 to 93.8 in November. Employment Expectations Indication fell from 102.8 to 102.1 Economic Uncertainty Indicator fell from 22.7 to 22.4.

Eurozone industry confidence fell from -9.2 to -9.5. Services confidence rose from 4.6 to 4.9. Consumer confidence rose from -17.8 to -16.9. Retail trade confidence rose from -7.4 to -7.0. Construction confidence rose from -5.5 to -4.8.

EU Economic Sentiment Indicator rose from 93.2 to 93.7. Employment Expectations Indicator fell from 102.3 to 101.8. Economic Uncertainty Indicator fell from 22.2 to 21.8.

Amongst the largest EU economies, the ESI improved in the Netherlands (+2.9), France (+2.0) and Poland (+1.7), while it eased in Spain (-1.5) and, to a lesser extent, in Germany (-0.5) and Italy (-0.3).

BoE’s Bailey dismisses rate cut speculations again

BoE Governor Andrew Bailey, in an interview, emphasized, “Two percent is our (inflation) target and we will do what it takes to get there.”

Bailey also addressed the speculation around interest rate cuts, categorically stating, “We are not in a place now where we can discuss cutting interest rates – that is not happening.”

He noted, “We need to see how the final part of the journey down to 2% inflation plays out; we have not seen enough of that journey yet to be confident.”

He acknowledged the ongoing economic challenges, including some weakening in economic activity. However, he described this observation as a “realist view” rather than an “ultra-pessimist” outlook, as some critics have suggested.

RBNZ raises rate track, signaling additional rate hike

RBNZ decided to keep the Official Cash Rate steady at 5.50%, aligning with market expectations. However, a significant aspect of their announcement is the upward revision of their “rate track.”

According to the bank’s forecasts in the Monetary Policy Statement, OCR is expected to peak at 5.70% in Q2 of 2024 and maintain this level throughout the year. Looking ahead, RBNZ anticipates a rate cut in Q2 of 2025, bringing it down to 5.4%.

In the accompanying statement, RBNZ noted, “ongoing excess demand and inflationary pressures are of concern, given the elevated level of core inflation.”

RBNZ also emphasized its readiness to hike again. “If inflationary pressures were to be stronger than anticipated, the OCR would likely need to increase further.”

Moreover, RBNZ underlined the necessity of maintaining interest rates at a restrictive level for a sustained period, aiming at ensuring consumer price inflation returns to target level and to support maximum sustainable employment.

Australia’s monthly CPI slowed to 4.9% in Oct, below exp 5.2%

Australia monthly CPI slowed from 5.6% you to 4.9% yoy in October, below expectation of 5.20%. Excluding volatile items and holiday travel, CPI slowed from 5.5% yoy to 5.1% yoy. Annual trimmed mean CPI also slowed from 5.4% yoy to 5.3% yoy.

The most significant contributors to the October annual increase were Housing (+6.1%), Food and non-alcoholic beverages (+5.3 per cent) and Transport (+5.9%).

BoJ’s Adachi: Not at a stage to discuss exit from ultra-loose policy

BoJ board member Seiji Adachi acknowledged that while there are early indications of a positive wage-inflation cycle emerging, these are not yet sufficient to consider exiting ultra-loose monetary policy.

He emphasized the importance of continuing with monetary easing approach, stating today, “For now, it’s appropriate to patiently continue with our monetary easing.”

Adachi specifically pointed out the challenges posed by China’s slowing growth and the potential impacts of aggressive US interest rate hikes, noting that these factors make it difficult to predict whether Japanese firms will substantially increase wages next year.

He also addressed the disparity in wage increase capabilities between large and small companies. While some big companies seem prepared to continue raising wages, many smaller firms, particularly in regional areas, are struggling to do so due to challenging business conditions.

He emphasized, “We’re not at a stage yet where we can discuss an exit” from ultra-loose policy.

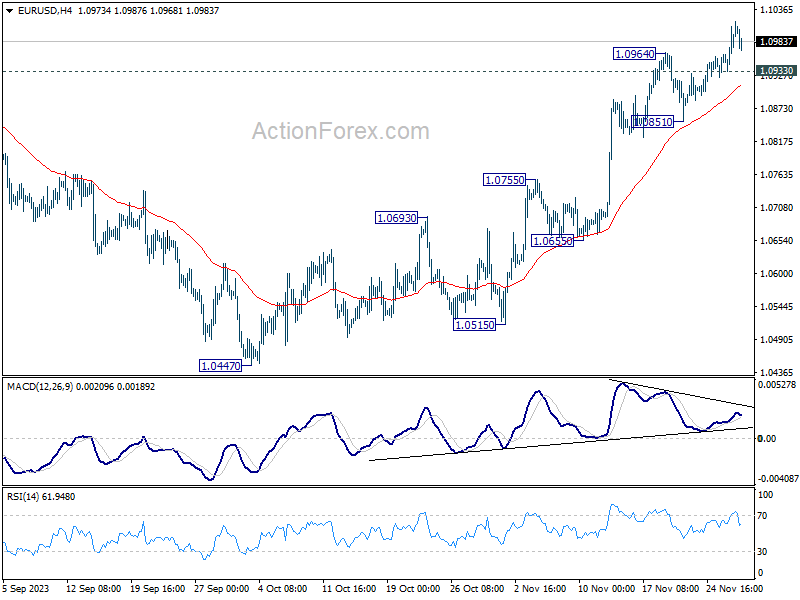

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0950; (P) 1.0980; (R1) 1.1024; More…

Intraday bias in EUR/USD stays on the upside with 1.0933 minor support intact. Current rise from 1.0447 should target 1.1274 resistance next. But strong resistance should be seen there to limit upside. On the downside, below 1.0933 minor support will turn intraday bias neutral and bring consolidations. But further rally will remain in favor as long as 1.0851 support holds.

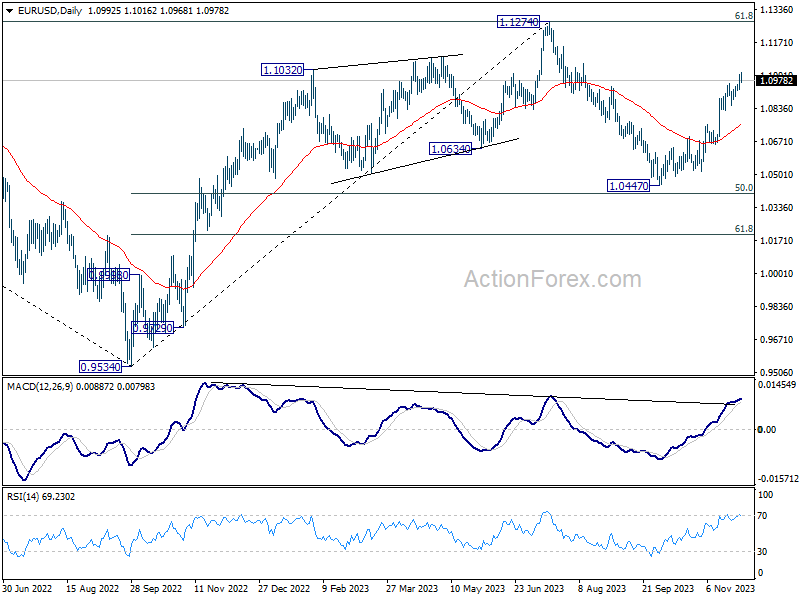

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Oct | 4.90% | 5.20% | 5.60% | |

| 01:00 | NZD | RBNZ Rate Decision | 5.50% | 5.50% | 5.50% | |

| 07:00 | EUR | Germany Import Price M/M Oct | 0.30% | 0.10% | 1.60% | |

| 09:00 | CHF | Credit Suisse Economic Expectations Nov | -29.6 | -37.8 | ||

| 09:30 | GBP | M4 Money Supply M/M Oct | 0.30% | -0.20% | -1.10% | |

| 09:30 | GBP | Mortgage Approvals Oct | 47K | 44K | 43K | 44K |

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Nov | 93.8 | 93.7 | 93.3 | 93.5 |

| 10:00 | EUR | Eurozone Industrial Confidence Nov | -9.5 | -8.9 | -9.3 | -9.2 |

| 10:00 | EUR | Eurozone Services Sentiment Nov | 4.9 | 4.3 | 4.5 | 4.6 |

| 10:00 | EUR | Consumer Confidence Nov F | -16.9 | -16.9 | -16.9 | |

| 13:00 | EUR | Germany CPI M/M Nov P | -0.40% | -0.10% | 0% | |

| 13:00 | EUR | Germany CPI Y/Y Nov P | 3.20% | 3.50% | 3.80% | |

| 13:30 | CAD | Current Account (CAD) Q3 | -3.2B | 0.7B | -6.6B | |

| 13:30 | USD | GDP Annualized Q3 P | 5.20% | 5.00% | 4.90% | |

| 13:30 | USD | GDP Price Index Q3 P | 3.60% | 3.50% | 3.50% | |

| 13:30 | USD | Goods Trade Balance (USD) Oct P | -89.8B | -86.7B | -86.8B | |

| 13:30 | USD | Wholesale Inventories Oct P | -0.20% | 0.10% | 0.20% | |

| 15:30 | USD | Crude Oil Inventories | -0.1M | 8.7M | ||

| 19:00 | USD | Fed’s Beige Book |