Australian Dollar weakens broadly in Asian session, as Australian employment data and shifting global risk sentiment take center stage. The mixed nature of the latest Australian jobs report is causing a rethink among investors regarding RBA’s next steps. Despite robust increase in overall employment numbers, a nuanced look reveals cracks in the job market’s strength.

The unexpected uptick in the unemployment rate and deceleration in work hours growth are clear indicators of a cooling labor market. This cooling trend reinforces expectation for RBA to hit pause on its interest rate hikes again in December meeting. RBA is likely to closely monitor the economic indicators over the festive season to gauge the need for further monetary policy adjustments in February.

Australian Dollar’s descent is also exacerbated by a cooling of risk-on sentiment that had buoyed the global markets earlier in the week. Investors are seemingly taking a breather and reassessing their positions. A key event that has captured the market’s attention is the meeting between US President Joe Biden and Chinese President Xi Jinping, which occurred on the sidelines of APEC summit. Although the meeting marked a step forward in re-establishing high-level military communications, it fell short of offering substantial breakthroughs in broader geopolitical tensions. The absence of a new defense minister appointment in China, following the unexplained dismissal of Gen. Li Shangfu, adds to the air of uncertainty affecting market sentiment.

In the broader currency spectrum, New Zealand Dollar is joining Australian Dollar as one of the day’s weakest performers so far, alongside British Pound and Canadian Dollar. On the flip side, Japanese Yen is emerging as the strongest currency for the day at this point, with t Dollar and Swiss Franc also showing resilience. Euro’s performance remains uneven across different pairings.

Despite the daily fluctuations, when looking at the weekly performance, Dollar continues to be at the bottom of the league, with Japanese Yen and Canadian Dollar also underperforming. Australian and New Zealand Dollars, along with Swiss Franc and Euro, are experiencing the strongest gains, whereas British Pound exhibits mixed results across the board.

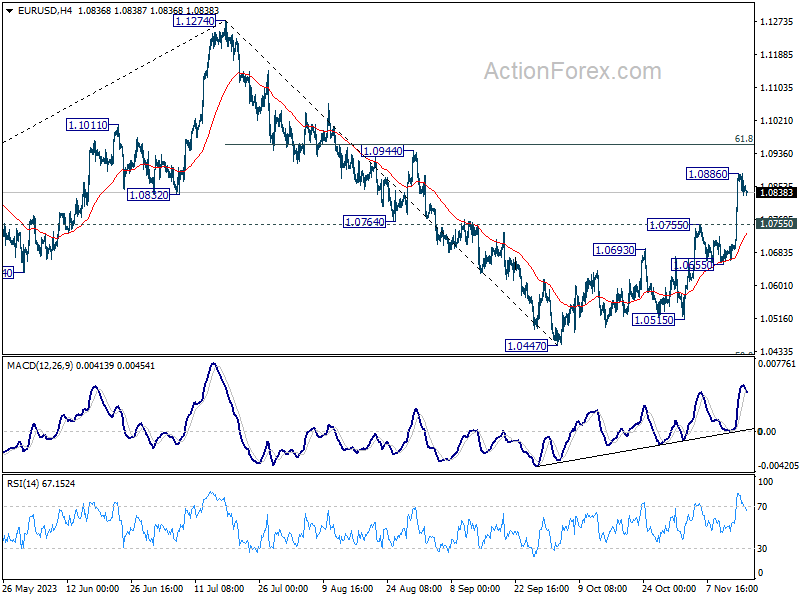

Technically, EUR/USD turned into consolidation after surging to 1.0886 earlier in the week. Some consolidations would be seen in the near term, but outlook will stay bullish as long as 1.0755 resistance turned support holds. Above 1.0886 will resume the rebound from 1.0447 to 61.8% retracement of 1.1274 to 1.0447 at 1.0958. Upside momentum will likely start to wane above 1.0958 fibonacci level. But any acceleration above there could be an early signal of more intense selloff in Dollar elsewhere.

In Asia, Nikkei closed down -0.27%. Hong Kong HSI is down -1.11%. China Shanghai SSE is down -0.49%. Singapore Strait Times is up 0.11%. Japan 10-year JGB yield is down -0.002 at 0.795. Overnight, DOW rose 0.47%. S&P 500 rose 0.16%. NASDAQ rose 0.07%. 10-year yield rose 0.094 to 4.535.

Fed’s Daly cautions against premature end to rate hikes, emphasizes need for patience

San Francisco Fed President Mary Daly, in an interview with the Financial Times, acknowledged the “very, very encouraging” signs of falling inflation in this week’s data. However, she cautioned against hastily concluding the rate-raising cycle, emphasizing the importance of a cautious and informed approach.

Daly expressed concern about prematurely ending the cycle, noting the potential risks involved. “We have to be bold enough to say ‘we don’t know’ and bold enough to say ‘we need to take the time to do it right’,” she stated. She warned that a premature halt could lead to a ‘stop-start’ scenario, which could ultimately harm the Fed’s credibility.

In her view, rate cuts are not on the immediate horizon. “Rate cuts are ‘not happening for a while’,” Daly remarked, suggesting a continued commitment to the current restrictive monetary policy direction until there is substantial evidence of a sustainable return to the 2% inflation target.

Australia’s employment grows 55k, yet signs of cooling emerge

Australia’s labor market displayed stronger-than-anticipated performance in October, with employment figures surpassing expectations. The economy added 55k jobs, well above forecasted growth of 22.8k. This increase was driven by both full-time and part-time employment, which rose by 17k and 37.9k respectively.

Despite this robust job growth, unemployment rate edged up slightly from 3.6% to 3.7%, aligning with market expectations. Pparticipation rate also saw an uptick, rising by 0.2% to 67.0%. Additionally, month-over-month hours worked in the economy increased by 0.5%.

Bjorn Jarvis, ABS head of labour statistics, noted that over the past two months, this equates to an average monthly employment growth of approximately 31k people, slightly lower than average growth of 35k people a month since October 2022.

He also highlighted that annual growth rate in hours worked has slowed to 1.7%, down from around 5% mid-year, and lower than annual employment growth of 3.0%. This slowdown may suggest that “the labour market is starting to slow, following a particularly strong period of growth.”

Japan’s exports increase for second month, despite persistent decline in China shipments

In October, Japan experienced a mixed bag in its trade sector. Exports saw a modest rise of 1.6% yoy to JPY 9167B, marking the second consecutive month of growth, albeit at a slower pace compared to September’s 4.3% yoy increase.

One notable aspect was the continued decline in shipments to China, which fell by -4.0% yoy. This marks the eleventh consecutive month of decline, underscoring the strained trade relations and potentially shifting economic alliances in the region.

Conversely, exports to the US surged by 8.4% yoy, buoyed by robust demand for hybrid vehicles and mining and construction machinery. This surge propelled the value of U.S.-bound shipments to record levels. Similarly, exports to Europe experienced a healthy increase of 8.9% yoy, indicating diversified trade relations.

On the import front, Japan witnessed a significant drop of -12.5% yoy to JPY 9810B. The trade balance resulted in a deficit of JPY -663B.

Looking at seasonally adjusted terms, both exports and imports saw month-on-month declines, with exports decreasing by -1.2% mom to JPY 8800B and imports falling by -0.7% mom to JPY 9262B. Consequently, trade deficit widened from September’s JPY -420B to JPY -462B.

Looking ahead

The European economic calendar is empty today. Canada will release housing starts in North American session. US will release jobless claims, Philly Fed survey, and industrial production.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6481; (P) 0.6512; (R1) 0.6540; More…

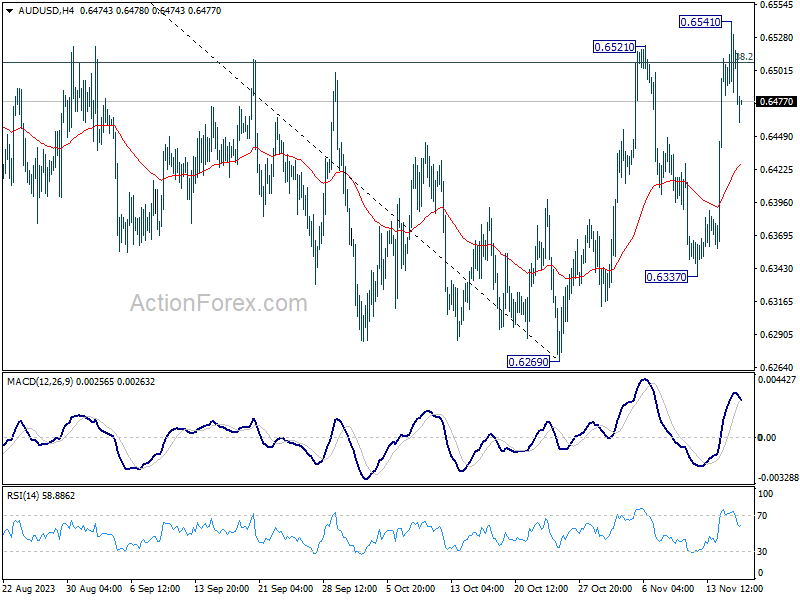

Despite spiking higher to 0.6541, subsequent retreat in AUD/USD suggests that a temporary top was formed. Intraday bias is turned neutral for some consolidations first. Downside should be contained by 55 4H EMA (now at 0.6427) to bring rebound. Break of 0.6541, and sustained trading above 38.2% retracement of 0.6894 to 0.6269 at 0.6508, will argue that whole corrective fall from 0.7156 has completed with three waves down to 0.6269. Stronger rally should seen to falling channel resistance (now at 0.6684) next.

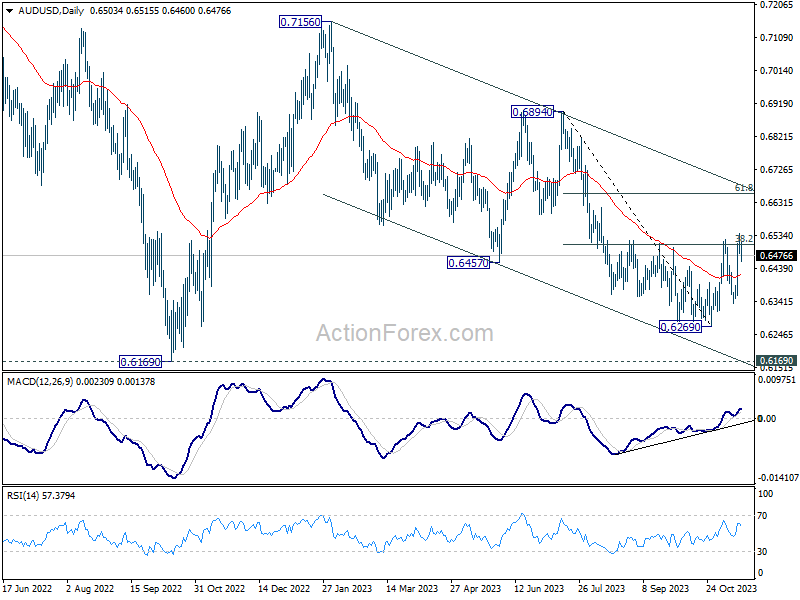

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. While current rebound from 0.6269 might extend higher, it could be the third leg of the corrective pattern from 0.6169 (2022 low) only. For now, medium term bearishness will remain as long as 0.6894 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (USD) Oct | -0.46T | -0.71T | -0.43T | |

| 23:50 | JPY | Machinery Orders M/M Sep | 1.40% | 0.90% | -0.50% | |

| 00:00 | AUD | Consumer Inflation Expectations Nov | 4.90% | 4.80% | ||

| 00:30 | AUD | Employment Change Oct | 55.0K | 22.8K | 6.7K | |

| 00:30 | AUD | Unemployment Rate Oct | 3.70% | 3.70% | 3.60% | |

| 04:30 | JPY | Tertiary Industry Index M/M Sep | -1.00% | -0.10% | -0.10% | 0.70% |

| 13:15 | CAD | Housing Starts Y/Y Oct | 255K | 270K | ||

| 13:30 | USD | Initial Jobless Claims (Nov 10) | 222K | 217K | ||

| 13:30 | USD | Import Price Index M/M Oct | -0.30% | 0.10% | ||

| 13:30 | USD | Philadelphia Fed Manufacturing Survey Nov | -11 | -9 | ||

| 14:15 | USD | Industrial Production M/M Oct | -0.40% | 0.30% | ||

| 14:15 | USD | Capacity Utilization Oct | 79.40% | 79.70% | ||

| 15:00 | USD | Natural Gas Storage |