In today’s currency markets, Australian Dollar is notably weaker across the board, a development that comes as a surprise considering the hawkish tone of the latest RBA Statement on Monetary Policy. The statement, which leaned towards the possibility of another rate hike, seemed insufficient to bolster the Aussie. Factors such as global risk aversion and specific worries about China’s economic recovery path significantly overshadowed RBA’s more aggressive policy outlook.

Meanwhile, Dollar is showing renewed vigor. The greenback’s strength is partly attributed to a rebound in 10-year Treasury yield, a response to Fed Chair Jerome Powell’s recent hawkish comments. Sterling, on the other hand, is experiencing some softness as market participants eagerly await release of GDP data. This upcoming economic indicator is crucial for reviving the chance of another BoE rate hike in the near term.

In a broader weekly perspective, Dollar stands out as the strongest currency, maintaining its lead despite not yet breaking through the highs of the previous week. Swiss Franc and Euro are trailing behind, drawing strength from their resilience against Sterling and various commodity currencies. Contrarily, Australian Dollar finds itself at the bottom of the performance chart, trailed by New Zealand Dollar and Japanese Yen, with Canadian Dollar exhibiting a mixed performance.

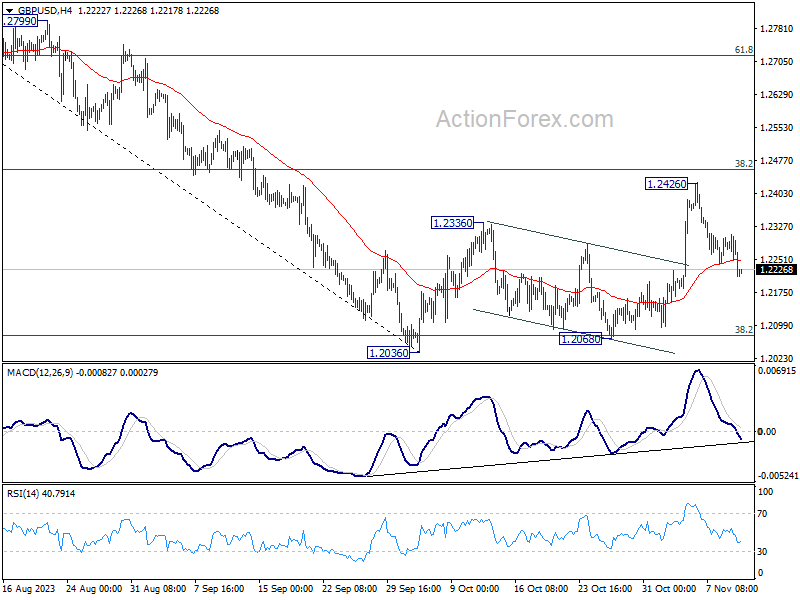

Technically, GBP/USD’s break of 55 4H EMA now argues that recovery from 1.2068 has completed at 1.2426. That came just ahead of 38.2% retracement of 1.3141 to 1.2036 at 1.2458. Rejection by 1.2458 keeps outlook in GBP/USD for declining through 1.2068 to resume the whole fall from 1.3141. Firm break of 55 4H EMA in EUR/USD will affirm the underlying bullish momentum in Dollar, and help drags GBP/USD lower towards 1.2068 next.

In Asia, at the time of writing, Nikkei is down -0.38%. Hong Kong HSI is down -1.59%. China Shanghai SSE is down -0.45%. Singapore Strait Times is down -0.85%. Overnight, DOW dropped -0.65%. S&P 500 dropped -0.81%. NASDAQ dropped -0.94%. 10-year yield rose 0.107 to 4.630.

RBA’s hawkish SoMP points to another rate hike

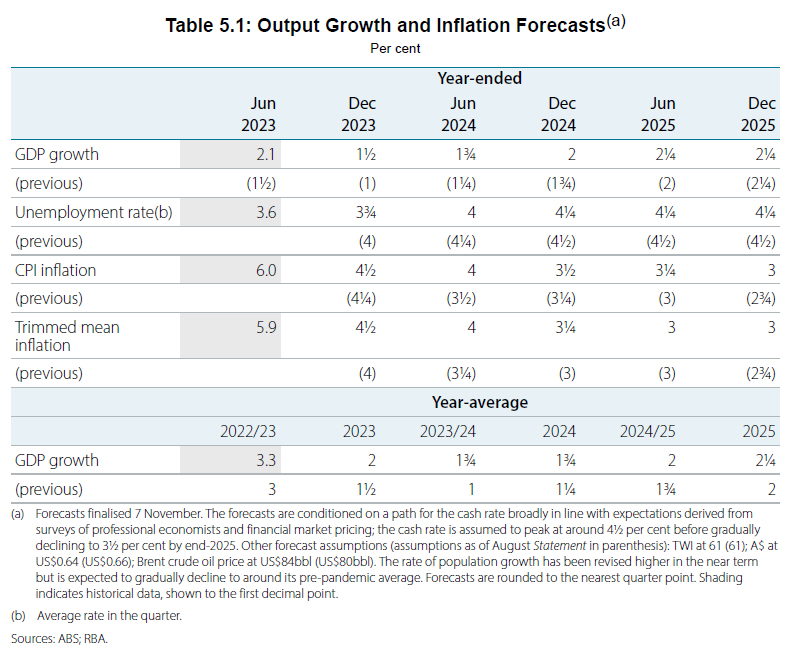

RBA’s latest Statement on Monetary Policy presents a more hawkish picture than market observers anticipated, with upward revisions in both headline and underlying inflation projections, alongside stronger growth outlook.

More importantly, these projections rest on the assumption that cash rate will peak around 4.50%, comparing to the current 4.35%, suggesting another rate hike could be imminent.

RBA’s heightened vigilance against inflation is clear: “The weight of recent information suggests that the risk of inflation remaining higher for longer has increased,” the bank stated, highlighting domestic inflation persistence and possible global factors, such as energy market disruptions and food price hikes tied to El Niño effects.

Economic projections now show a year-average GDP growth expected to hit 2.00% in 2023, rising to 1.75% in 2024, and reaching 2.25% in 2025. These figures mark an upgrade from June’s forecast of 1.50%, 1.25%, and 2.00% respectively, suggesting a resilient economy that could withstand tighter monetary policy.

Inflation forecasts have also been adjusted upward, with headline CPI inflation now seen at 4.50% at the year’s end in 2023, followed by 3.50% in 2024, and softening to 3.00% in 2025. They are upgraded from 4.25%, 3.25% and 2.75% respectively.

The trimmed mean inflation follows a similar upward trajectory, projected to be at 4.50% in year-ended 2023, 3.25% in 2024, and 3.00% in 2025, up from prior forecast of 4.00%, 3.00%, and 2.75% respectively.

Underpinning these projections are technical assumptions of a cash rate peaking at around 4.50%, with a gradual decline to a pproximately 3.50% by the end of 2025, indicating a higher rate path than previously used.

pproximately 3.50% by the end of 2025, indicating a higher rate path than previously used.

NZ BNZ PMI fell to 42.5, manufacturing downturn reaches lowest point since 2009

October has marked a significant downturn for New Zealand’s manufacturing sector, with BusinessNZ Performance of Manufacturing Index plummeting from 45.1 to 42.5. This figure not only represents the fifth consecutive month of declining activity but also stands as the lowest activity level for a month unaffected by COVID-19 restrictions since May 2009, deeply underscoring the sector’s distress.

Delving into the components, the bleak picture becomes clearer: Production has taken a hit, sliding down from 44.3 to 41.5, and employment in the sector is also suffering, with a drop from 45.1 to 43.3. New orders barely held ground, marginally decreasing from 44.8 to 44.1. A significant retreat was seen in finished stocks, which contracted from 51.2 to 45.7, and deliveries were also on the downturn from 44.3 to 42.9.

Amidst these figures, the voice of the industry has tilted towards concern, with 65.1% of comments categorized as negative, albeit slightly less pessimistic than previous months, at 68.8% in September and 66.7% in August.

BNZ Senior Economist, Doug Steel, highlighted the potential ramifications for the broader economy: “Today’s PMI is not a good look for GDP and employment growth,” he noted. With the current forecasts including a downturn in manufacturing for the latter half of 2023, Steel warned, “There’s a chance that decline is bigger than we think, if the PMI does not bounce in the final months of the year.”

Fed Chair Powell vows to tighten further if needed amid inflation head fakes

Fed Chair Jerome Powell, speaking at an IMF event, conveyed a vigilant stance on monetary policy, expressing uncertainty over whether current interest rates are adequate to curb inflation. With a steadfast commitment to FOMC’s inflation target, Powell emphasized the readiness to adjust policy in response to economic indicators.

“The FOMC is committed to achieving a stance of monetary policy that is sufficiently restrictive to bring inflation down to 2 percent over time; we are not confident that we have achieved such a stance,” Powell stated

At the same time, “we are not confident that we have achieved such a stance,” he added.

Highlighting the deceptive nature of recent inflation trends, he added, “Inflation has given us a few head fakes”. Hence, “ongoing progress toward our 2 percent goal is not assured”

Powell was unequivocal about the Fed’s resolve: “If it becomes appropriate to tighten policy further, we will not hesitate to do so.”

Fed’s Bostic and Barkin discuss restrictive policy and inflation outlook

In a dual appearance at an event in New Orleans overnight, Richmond Fed President Thomas Barkin and Atlanta Fed President Raphael Bostic provided insights into the Federal Reserve’s ongoing efforts to tame inflation.

Bostic expressed confidence in the current policy stance, which it “likely sufficiently restrictive”, predicting that it should be enough to curb inflationary pressures, albeit with potential challenges ahead. “Inflation is going to get to 2%,” he assured, committing to maintaining a restrictive policy until that target is firmly within sight.

Barkin focused on the anticipated impacts of Fed’s policies, noting that “we are still not seeing the full effects of policy”. He forecasted an economic downturn as necessary for achieving the Fed’s targets: “I believe there’s a slowdown coming. I believe we’re going to need that slowdown, because I think that’s what it’s going to take to convince price-setters the days of pricing power are over.”

Fed’s Barkin suggests inflation might ease back to target with no further rate hikes

Richmond Fed President Thomas Barkin deliberated on Fed’s monetary policy stance in light of the ongoing economic slowdown and its implications for inflation during an MNI Webcast.

Barkin addressed the possibility that the current economic environment might not necessitate further intervention: “Whether a slowdown that settles inflation requires more from us remains to be seen, which is why I supported our decision to hold rates at our last meeting,” he remarked.

He emphasized the opportunity for Fed to assess the economic outlook before taking further action: “With rates restrictive and financial conditions tightened, we have time to reconcile competing narratives on demand and to test different views on the trajectory of inflation,” Barkin explained.

He also allowed for the possibility that the current policy stance might suffice, suggesting, “perhaps inflation could return to target without more help from us and without too much damage to demand.”

Fed’s Paese emphasizes prudence, awaits data before additional tightening

St. Louis Fed President Kathleen O’Neill Paese emphasized the current effectiveness of monetary policy in exerting “modest downward pressure on inflation.”

“We can afford to await further data before concluding that additional policy tightening is appropriate,” Paese stated.

Despite this cautious approach, she warned against complacency, asserting that prompt action must be taken if the downward trend in inflation shows signs of stalling.

“However, if progress toward achieving 2% inflation stalls, I believe that the committee should act promptly to ensure that high inflation does not become entrenched,” she noted.

Paese also reminded that the high-interest-rate environment is expected to persist as part of the long-term strategy to rein in inflation.

Looking ahead

UK GDP, production, and goods trade balance are the main focuses in European session. Later in the day, US Michigan University consumer sentiment will be the highlight.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6344; (P) 0.6387; (R1) 0.6409; More…

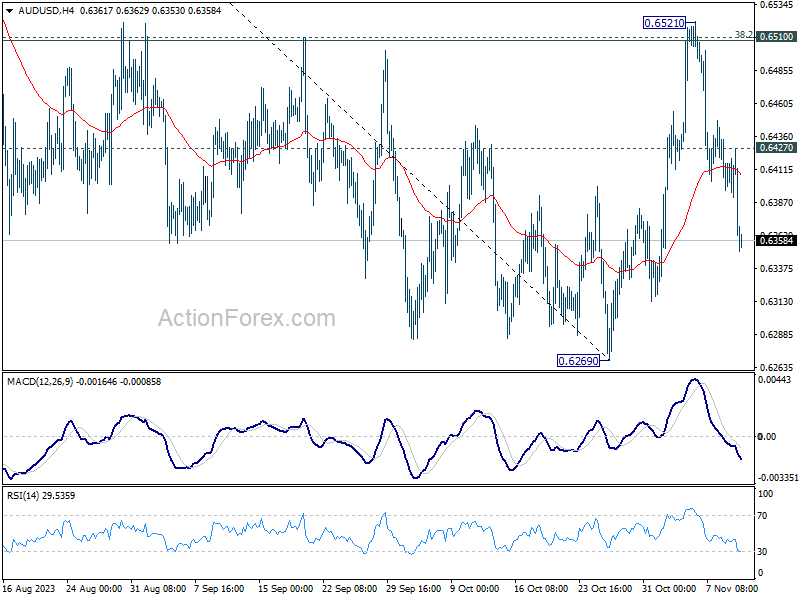

AUD/USD’s steep decline now suggests that rebound from 0.6269 has completed at 0.6521. The development also indicates rejection by 0.6510 cluster resistance (38.2% retracement of 0.6894 to 0.6269 at 0.6508), and retain near term bearishness. Intraday bias is back on the downside for retesting 0.6269 low. Firm break there will resume larger fall from 0.7156, to retest 0.6169 low. On the upside, above 0.6427 minor resistance will turn intraday bias neutral first.

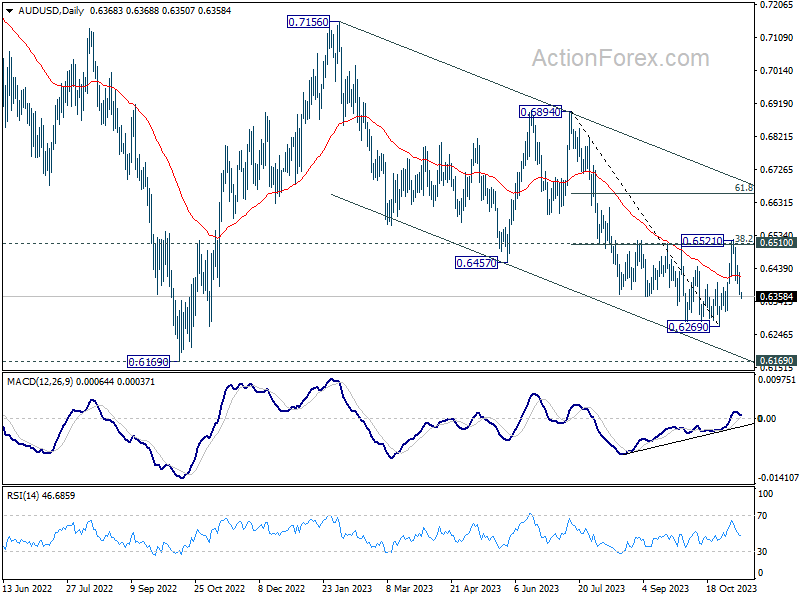

In the bigger picture, there is no confirmation that down trend from 0.8006 (2021 high) has completed. While current rebound from 0.6269 might extend higher, it could be the third leg of a corrective pattern from 0.6169 (2022 low) only. For now, medium term bearishness will remain as long as 0.6894 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Oct | 42.5 | 45.3 | 45.1 | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Oct | 2.40% | 2.40% | ||

| 00:30 | AUD | RBA Monetary Policy Statement | ||||

| 07:00 | GBP | GDP M/M Sep | 0.00% | 0.20% | ||

| 07:00 | GBP | GDP Q/Q Q3 P | -0.10% | 0.20% | ||

| 07:00 | GBP | Manufacturing Production M/M Sep | 0.30% | -0.80% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Sep | 2.80% | |||

| 07:00 | GBP | Industrial Production M/M Sep | -0.10% | -0.70% | ||

| 07:00 | GBP | Industrial Production Y/Y Sep | 1.10% | 1.30% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Sep | -15.3B | -16.0B | ||

| 09:00 | EUR | Italy Industrial Output M/M Sep | -0.10% | 0.20% | ||

| 12:00 | GBP | NIESR GDP Estimate (3M) Oct | -0.10% | |||

| 15:00 | USD | Michigan Consumer Sentiment Index Nov P | 63.6 | 63.8 |