US m/m inflation CPI

This week is dismal on the economic data front but next week begins to get interesting because of the November 14 release of the latest US CPI report.

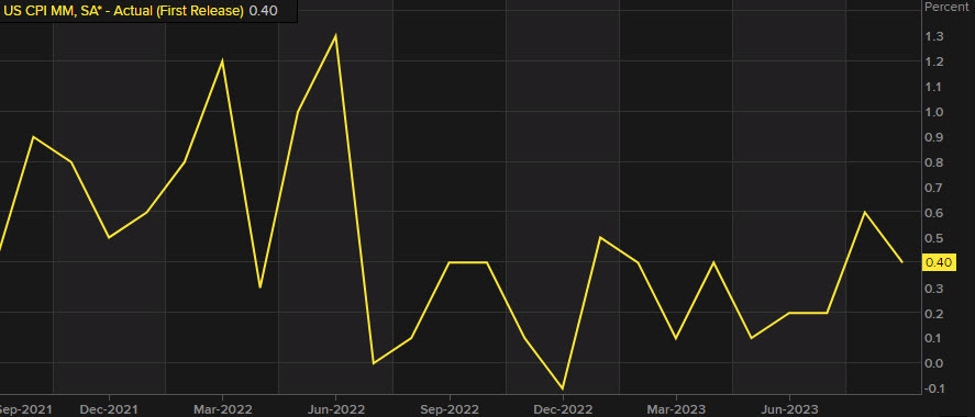

It’s still early for estimates but the consensus so far is +0.1% m/m on the headline. That’s coming on the heels of +0.6% and +0.4% m/m readings but with oil prices reversing, so should CPI. In addition, the latest fall in oil prices should weigh heavily on November CPI and it’s now not out of the question that we get 0.1% readings for both months.

On the y/y side, the September reading was +3.7% but a +0.4% m/m reading rolls off so we should get some downward pressure and potentially below 3.5%. The comps get tough again in Nov/Dec before offering some major help in Jan and Fed (+0.5% and +0.4%, respectively).

With these numbers and the declines in oil and gas, there’s a good chance we see sub 3% inflation in the US within 3 months.

That’s obviously good news but the Fed is more-focused on core inflation and core-services inflation in particular. The early consensus for core is +0.3%. The details of will matter and is likely and a high reading could give markets pause in pricing in 88 bps in cuts next year.

The best signals might becoming from the bond market, where US 10-year yields are back down to 4.51%. Today’s auction demand was decent and suggests that real money is on board with the move lower in rates, and likely sensing lower inflation.

US 10y yield