Yen, Swiss Franc, and Dollar are weakening in early US session, with a discernible shift in European market sentiment that suggests a mild recovery. Major European stock indexes have inched upwards, and US futures market also indicates a higher opening. Despite early signals suggesting Yen might rebound, likely in light of tomorrow’s BoJ policy announcement, such hopes were short-lived. Yen reversed quickly and, as a result, it’s is currently the day’s most underperforming currency.

Conversely, commodity currencies, led by Australian Dollar, are rebounding. The unexpected robustness in retail sales data has bolstered Aussie’s momentum. This is set against the backdrop of anticipated monetary policy action from RBA, with market watchers keenly anticipating another rate hike on November 7.

Euro and Sterling are currently showing mixed performance, though Euro seems to be holding a slight advantage. This can be attributed, in part, to comments from ECB officials who downplayed the likelihood of rate cut in the first half of the upcoming year. Lower than expected German inflation data is ignored.

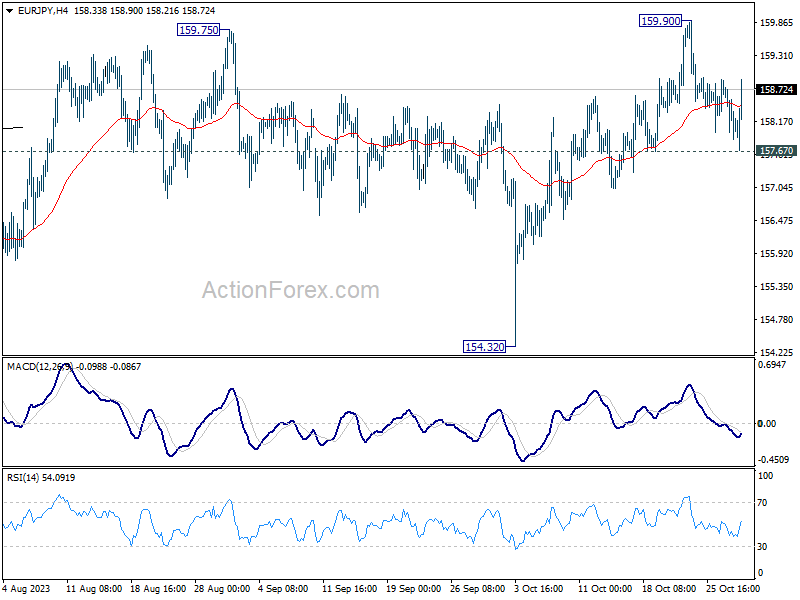

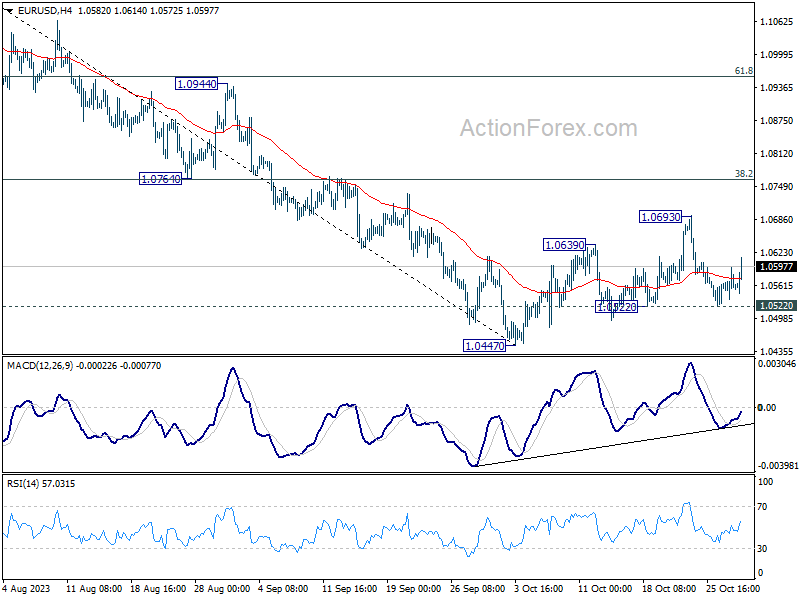

From a technical perspective, the spotlight is on Euro’s movement during the remainder of the session. Both EUR/USD and EUR/JPY have seen rebounds from support levels of 1.0522 and 157.67 respectively. Further break of 1.0693 and 159.90 resistance levels will resume their near term rises. Additionally, surpassing the 0.8739 resistance in EUR/GBP might also signify the continuation of its ascent from 0.8491. Should all these levels be surpassed, it would be a strong indication of burgeoning bullish momentum for the Euro.

In Europe, at the time of writing, FTSE is up 0.75%. DAX is up 0.45%. CAC is up 0.55%. Germany 10-year yield is up 0.019 at 2.852. Earlier in Asia, Nikkei dropped -0.95%. Hong Kong HSI rose 0.04%. China Shanghai SSE rose 0.12%. Singapore Strait Times rose 0.08%. Japan 10-year JGB yield rose 0.0209 to 0.897.

ECB’s Kazimir dismisses rate cut expectations; urges patience on policy decisions

ECB Governing Council member Peter Kazimir dismissed speculations of impending rate cuts in the early months of 2024. Speaking earlier today, he stated emphatically, “Bets on rate cuts happening already in the first half of next year are entirely misplaced.” Instead, he alluded to a persistent approach, suggesting that “We will have to stay at the peak for the next few quarters.”

Addressing the growing sentiment that the current policy cycle is nearing its end, Kazimir urged caution. “All those voices coining this as the end of the cycle should hold their horses,” he remarked. “It’s too soon to declare victory and say the job’s done.”

While not entirely closing the door on further adjustments, Kazimir implied that any future policy decisions would be data-driven. “Additional tightening could come, if incoming data force us to take such a step,” he explained.

The unfolding situation in the Middle East remains a concern, especially given its potential implications on inflation. Kazimir shared, “I will eagerly await the December update of our inflation forecast to get a clearer picture, confirmation, that the decline in inflation is sustained. I hope that renewed upside inflation risks from the escalating tragic conflict in the Middle East will not materialize.”

Furthermore, Kazimir highlighted the significance of upcoming milestones before any definitive policy stance is taken. “December forecasts are one of two key milestones needed to pass. March is the latter. By then, it should have become clearer how wage negotiations for the whole year turned out and whether the risks of a spiral of high prices and high wages were off the table,” he added.

ECB’s Simkus: Current restrictive rates sufficient, talk about cuts premature

ECB Governing Council member Gediminas Simkus said today, “In my view, if there’s no new staggering data, current restrictive levels are sufficient,” to steer inflation back to target.

Highlighting the bank’s current approach, Simkus clarified, “There is and there was no need to raise rates at this point.” But, “Will we need this in the future? We still have to wait and see. I’m hopeful this won’t be needed.”

Addressing the speculation around potential rate cuts, Simkus was clear in his stance. “Inflation is still high, too high. Any talk about cuts is premature. We need strategic patience to keep rates at restrictive levels,” he asserted.

Dispelling any immediate expectations of a rate reduction, he added, “I’d be highly surprised to see a rate cut in the first half. I don’t think so.”

Eurozone economic sentiment ticks down to 93.3

Eurozone Economic Sentiment Indicator fell slightly from 93.4 to 93.3 in October. Employment Expectations Indicator fell from 102.9 to 102.8. Economic Uncertainty Indicator rose from 21.5 to 22.7. Industrial confidence fell from -8.9 to -9.3. Services confidence rose from 4.1 to 4.5. Consumer confidence ticked down from -17.8 to -17.9. Retail trade confidence fell from -5.7 to -7.8. Construction confidence rose from -6.0 to -5.9.

EU ESI rose from 92.9 to 93.1. EEI fell from 102.6 to 102.3. EUI rose from 21.1 to 22.2. Amongst the largest EU economies, the ESI improved in Poland (+1.4), Spain (+1.2) and Germany (+0.5). By contrast, sentiment deteriorated markedly in France (-2.9) and, to a lesser extent, Italy (-0.9). The ESI remained unchanged in the Netherlands (±0.0).

German GDP contracts -0.1% qoq in Q3, less severe than expected

Germany’s GDP (price, seasonally, and calendar adjusted) shrank by -0.1% qoq in Q3. This decline, however, was slightly less severe than the anticipated -0.2% qoq contraction. This contraction comes in the wake of a modest 0.1% growth in Q2 and a state of stagnation in Q1.

On a year-over-year basis, the picture appears more pronounced. GDP was down by -0.8% (price adjusted) and down by -0.3% (price and calendar adjusted) compared to the same quarter a year earlier.

Destatis said a key factor contributing to the contraction was decrease in household final consumption expenditure. There were positive contributions from gross fixed capital formation in machinery and equipment.

Swiss KOF ticked down to 95.8, stable but underwhelming

Swiss KOF Economic Barometer demonstrated a minor dip, decreasing by -0.1 to settle at 95.8 in September. This figure modestly surpassed the expected mark of 95.6, indicating a slightly more favorable scenario than anticipated.

However, this marginal decrease also reflects that Barometer is continuing its trend of hovering just below the long-term average. The KOF (Swiss Economic Institute) elaborated on this trend, noting that “together with the small movements of the Barometer since the summer, this indicates a weak but stable development of the Swiss economy towards the end of this year.”

KOF pointed out that “the slight decline is primarily attributable to bundles of indicators from the manufacturing sector and to indicators concerning foreign demand.”

It’s not all subdued tones. KOF also highlighted some positive aspects, stating, “Indicators from the finance and insurance sector and the hospitality sector are sending positive signals.”

Australian retails rose 0.9% mom, strong Sep in subdued 2023

Australia’s retail sales turnover registered a 0.9% mom growth in September to AUD 35.87B. This robust performance dwarfed the modest analyst expectations of a 0.3% mom growth. On an annual basis, sales turnover presented a rise of 2.0% yoy compared to the same month in the preceding year.

Speaking on the development, Ben Dorber, ABS head of retail statistics, elucidated, “The strong rise in September came from a diverse range of factors across the Retail industry.” He pinpointed the uncommonly warm onset of spring as a significant catalyst while technology and energy-conscious programs also had their roles.

However, while September’s figures paint a buoyant picture, Dorber pointed to a more restrained broader context.

“While the rise in September was the largest since January, subdued spending for most of 2023 means that underlying growth in Retail turnover remains historically low,” he said.

Adding weight to this perspective, he shared that “Retail turnover in trend terms is up only 1.5 per cent compared to September 2022 – the smallest trend growth over 12 months in the history of the series.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0534; (P) 1.0566; (R1) 1.0596; More…

EUR/USD rebounded notably today but stays below 1.0693 resistance at this point. Intraday bias remains neutral first. On the downside, break of 1.0522 support will turn bias back to the downside for retesting 1.0447 low. Break there will resume larger fall from 1.1274. On the other hand, strong bounce from current level, followed by break above 1.0693, rebound from 1.0447 to 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763).

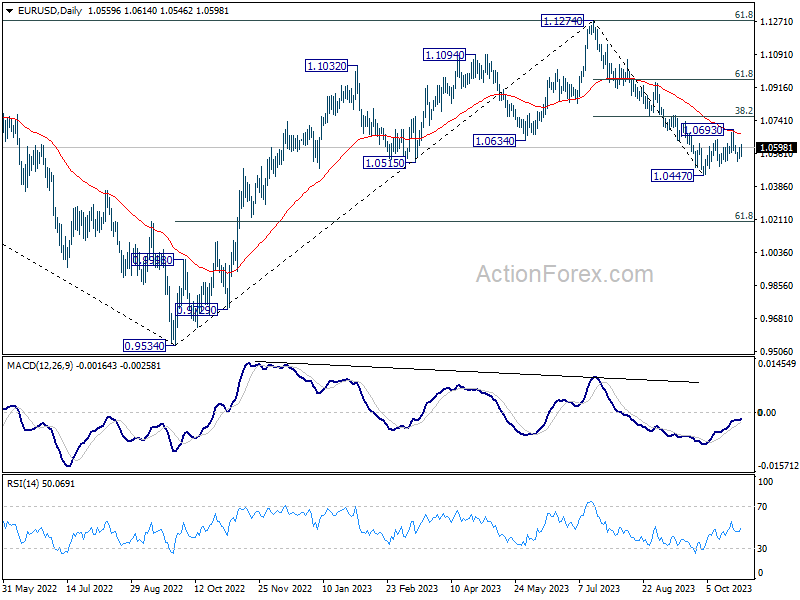

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0665) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Sep | 0.90% | 0.30% | 0.20% | 0.30% |

| 08:00 | CHF | KOF Economic Barometer Oct | 95.8 | 95.6 | 95.9 | |

| 09:00 | EUR | Germany GDP Q/Q Q3 P | -0.10% | -0.20% | 0.00% | |

| 09:30 | GBP | Mortgage Approvals (GBP) Sep | 43K | 44K | 45K | |

| 09:30 | GBP | M4 Money Supply M/M Sep | -1.10% | 0.10% | 0.20% | |

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Oct | 93.3 | 93.3 | 93.3 | |

| 10:00 | EUR | Eurozone Industrial Confidence Oct | -9.3 | -9.5 | -9 | |

| 10:00 | EUR | Eurozone Services Sentiment Oct | 4.5 | 3.4 | 4 | |

| 10:00 | EUR | Eurozone Consumer Confidence Oct F | -17.9 | -17.9 | -17.9 | |

| 13:00 | EUR | Germany CPI M/M Oct P | 0.00% | 0.20% | 0.30% | |

| 13:00 | EUR | Germany CPI Y/Y Oct P | 3.80% | 4.00% | 4.50% |

This “NEW CONCEPT” Trading Strategy Prints Money!… (INSANE Results!)

This “NEW CONCEPT” Trading Strategy Prints Money!… (INSANE Results!) RULE-BASED Pocket Option Strategy That Actually Works | Live Trading

RULE-BASED Pocket Option Strategy That Actually Works | Live Trading