Dollar staged a notable comeback overnight, accompanied by a sharp ascent in treasury yields and a downtick in stocks. This resurgence was catalyzed by the release of US CPI data that stoked concerns of another Fed rate hike this year. However, this speculation has yet to be significantly mirrored in futures pricing, which currently pegs the likelihood of a December hike at a mere 33%. Despite this, the prevailing risk-off sentiment, marked by red-tinged major indexes, extends into Asian session.

Investors are now pivoting their attention towards the impending release of the University of Michigan consumer sentiment and inflation expectations data. A surprise revelation in these metrics could potentially catapult Dollar to close the week as the dominant currency.

In the broader currency arena, New Zealand Dollar is languishing as the week’s underperformer, its decline exacerbated by unimpressive manufacturing data unveiled in today’s Asian session. Australian Dollar trails closely behind, with Euro also succumbing to downward pressures. Conversely, Swiss Franc stands as the week’s prime performer, although the revitalized Dollar threatens to usurp this lead. Canadian Dollar is exhibiting moderate strength, the Sterling and Yen are locked in a mixed performance standoff.

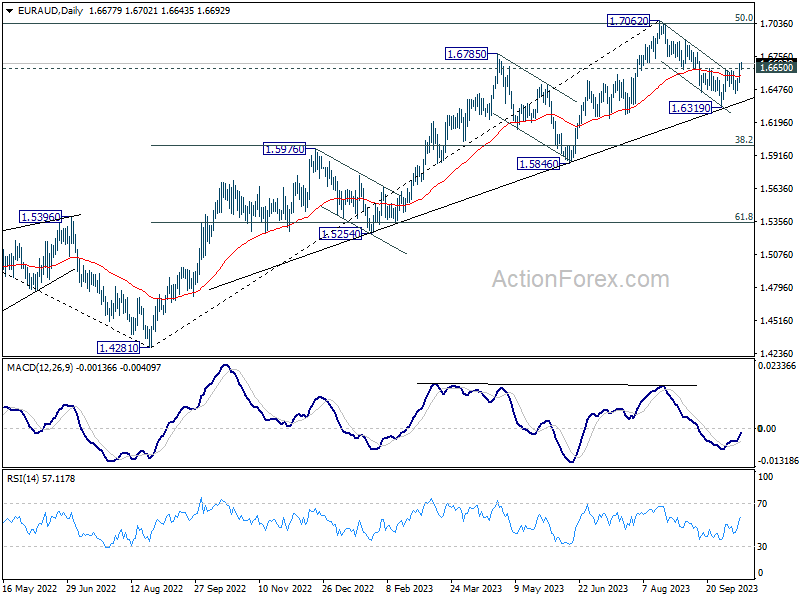

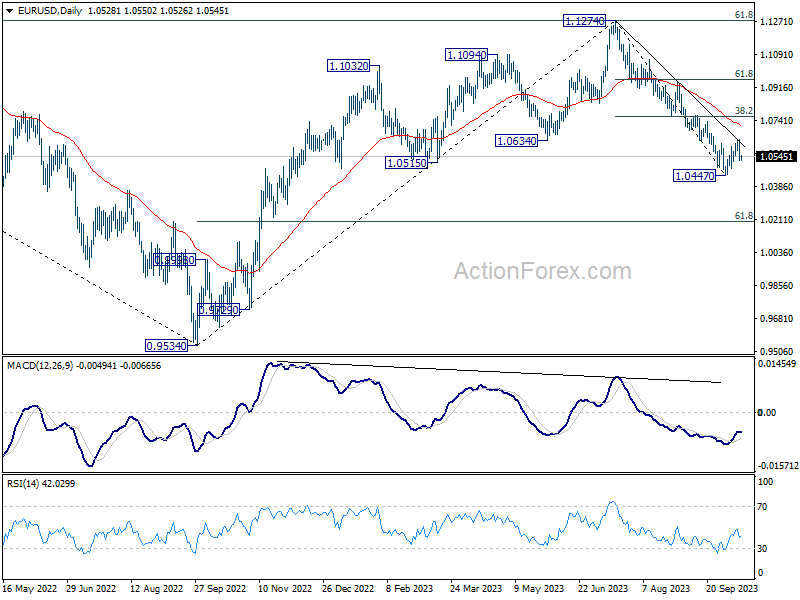

On the technical front, EUR/AUD’s break of 1.6650 resistance now argues that correction from 1.7062 has completed at 1.6319 already, after drawing support from medium term trend line. Further rally is now in favor back to retest 1.7062 high. At the same time, EUR/USD’s recovery from 1.0447 short term bottom could have completed at 1.0639. Break of 1.0518 minor support will resume EUR/USD fall from 1.1274 through 1.0447 support. If both scenarios play out as mentioned, AUD/USD should experience downside acceleration and power through 0.6284 to resume the larger down trend.

In Asia, at the time of writing, Nikkei is down -0.66%. Hong Kong HSI is down -2.05%. China Shanghai SSE is down -0.66%. Singapore Strait Times is down -0.86%. Japan 10-year JGB yield is up 0.0086 at 0.764. Overnight, DOW dropped -0.51%. S&P 500 dropped -0.62%. NASDAQ dropped -0.63%. 10-year yield rose 0.117 to 4.701.

Fed’s Collins believes rates may have peaked in current cycle

Boston Fed President Susan Collins highlighted that recent rise in long-term yields implies some tightening of financial conditions. “If it persists, it likely reduces the need for further monetary-policy tightening in the near term,” she noted in a speech yesterday.

Such market dynamics further bolstered Collins’ perspective on the current tightening cycle led. “This reinforces my view that we are very near, and perhaps at, the peak federal funds rates for this tightening cycle,” she stated, indicating that the cycle could be nearing its zenith.

However, Collins maintained a flexible stance on the future course of action, and clarified, “I would not take further tightening off the table yet.”

Weighed in on yesterday’s CPI data, which revealed that September’s headline inflation held steady at 3.7% and core inflation eased to 4.1%. Collins said, “Today’s CPI release is a reminder that restoring price stability will take time.”

New Zealand BNZ PMI falls to 45.3, entrenched manufacturing downturn deepens

New Zealand manufacturing sector has further sunk into troubled waters, as evidenced by the continued and deepening contraction observed in recent data.

BusinessNZ Performance of Manufacturing Index for September highlighted this slowdown by dropping to 45.3, down from 46.1 the previous month. This marks its most dismal performance for a month unaffected by COVID-19 since May 2009 and sits notably below the long-term average activity rate of 52.9.

Delving into the specifics, there’s a discernible decline across most metrics. While production saw a slight uptick, moving from 43.8 to 44.6, other areas weren’t as fortunate. Employment indicators slid from 47.7 to 45.2, and new orders also receded from 46.6 to 44.9. Meanwhile, finished stocks dwindled, albeit marginally, from 52.0 to 51.6, and deliveries plunged from 47.8 to 44.3.

Catherine Beard, BusinessNZ’s Director of Advocacy, highlighted the sustained downturn, pointing out that the sector “has now been in contraction for seven consecutive months, with little sign it is showing any improvement.”

On the economic front, BNZ Senior Economist Doug Steel provided a bleak perspective, remarking, “the trend remains firmly downward.” He also touched upon the challenges in discerning the exact causes of any PMI result but cited “falling sales, rising costs, and election uncertainty” as significant factors currently impacting the sector..

China’s export slump persists but softens; imports shrink further as CPI stalls

China’s trade figures for September revealed a continued, albeit moderating, decline in exports, marking the fifth consecutive month of contraction. Exports dropped by -6.2% yoy to USD 229.1B, an improvement from the -8.8% yoy decline recorded in the previous month. Despite this easing contraction, prolonged declines in shipments to major trade partners underscore the persisting challenges in the external sector.

A breakdown of the data shows exports to ASEAN countries contracted by -15.8% yoy, hitting USD 55B. The US, amidst a 14-month streak of declines, saw a -9.3% yoy contraction in goods from China, totaling USD 46B. European Union imports from China also fell by -11.6% yoy. In contrast, Russia exhibited a robust appetite for Chinese goods, with exports soaring by 20.6% yoy.

On the import front, China’s inbound shipments contracted by -6.2% yoy to USD 221.4B, marking the seventh consecutive monthly decline but showing a slower pace compared to August’s -7.3% yoy contraction. Consequently, trade surplus widened to USD 77.7B, outperforming market expectations.

Inflation dynamics within the country presented another layer of economic intricacies. China’s CPI stagnated at 0.0% yoy in September, pulled down by a -3.2% yoy decline in food prices, and falling short of the anticipated 0.2% yoy increase. The National Bureau of Statistics cited a high base of comparison with last year and abundant food supply ahead of the Golden Week holiday as key factors behind the subdued inflation.

Simultaneously, PPI showed a -2.5% yoy decline, extending the 12-month streak of contraction yet revealing an easing trend from August’s -3.0% yoy drop.

Looking ahead

Swiss PPI and Eurozone industrial production will be released in European session. Later in the day, US will release import price index and U of Michigan consumer sentiment.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0489; (P) 1.0565; (R1) 1.0603; More…

Immediate focus is back on 1.0518 minor support in EUR/USD with current fall. Firm break there will confirm that corrective recovery from 1.0447 has completed at 1.0639, after hitting near term falling trend line. Larger decline from 1.1274 should then be resumed through 1.0447 to 1.0119 fibonacci level. On the upside, though, above 1.0639 will resume the recovery to 1.0764 resistance.

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0709) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Sep | 45.3 | 46.1 | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Sep | 2.40% | 2.40% | 2.50% | |

| 01:30 | CNY | CPI Y/Y Sep | 0.00% | 0.20% | 0.10% | |

| 01:30 | CNY | PPI Y/Y Sep | -2.50% | -2.40% | -3.00% | |

| 03:00 | CNY | Trade Balance (USD) Sep | 77.7B | 73.7B | 68.4B | |

| 06:30 | CHF | Producer and Import Prices M/M Sep | 0.20% | -0.20% | ||

| 06:30 | CHF | Producer and Import Prices Y/Y Sep | -0.80% | |||

| 09:00 | EUR | Eurozone Industrial Production M/M Aug | 0.10% | -1.10% | ||

| 12:30 | USD | Import Price Index M/M Sep | 0.60% | 0.50% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Oct P | 68 | 68.1 |