Sterling has emerged as the predominant force in today’s currency market, a surge attributed to the dramatic escalation in UK gas prices, which have ascended to their peak since June. Concerns about potential sabotage exacerbating supply constraints are rife, especially after a leak was detected in the Balticconnector pipeline—a crucial conduit for gas transmission between Estonia and Finland. Finland’s Prime Minister Petteri Orpo’s indication that “external action” is likely behind the leak amplifies concerns. These developments spell trouble for BoE’s efforts to tame inflation. The sudden jolt in energy prices, if sustained, could trickle down into broader inflation metrics, complicating the central bank’s policy calculus.

On the other side of the Atlantic, Dollar is languishing at the lower echelons of the weekly chart, a situation reflecting the ongoing pullback. Global unrest stemming from the Middle East conflict has temporarily taken a backseat. At the same time, attention shifted to anticipations of an extended pause in Fed’s tightening cycle. Both developments buoyed US stocks while optimism spilled over positively into the Asian session.

A chorus of Fed officials have begun to sing a similar tune, suggesting that elevated Treasury yields could potentially alleviate the necessity for accelerated rate hikes. However, the plot thickens as 10-year yield underwent a significant pullback, fueled by a safe-haven rush to bonds amid geopolitical tensions. Market participants are now casting their gaze towards upcoming data releases, including US PPI and FOMC minutes today, as well as the pivotal CPI figures due tomorrow, for clearer directional cues.

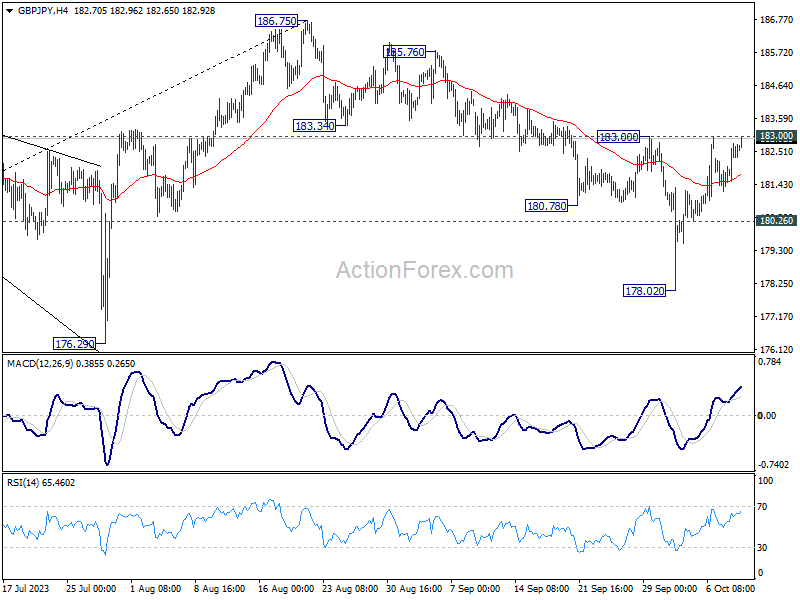

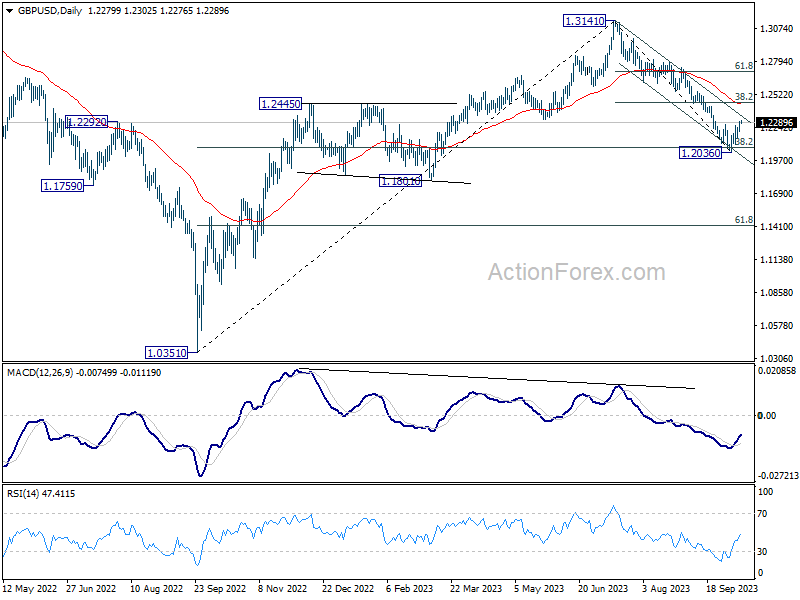

In the technical arena, a noteworthy development is the surge in GBP/USD, breaking the 1.2270 resistance and indicating short-term bottoming at 1.2036. Concurrently, EUR/GBP pierced through 0.8629 support, resuming the choppy decline from 0.8704. The spotlight now falls on 183.00 resistance in GBP/JPY; decisive break could pave the way for a retest of 186.75 high.

In Asia, at the time of writing, Nikkei is up 0.78%. Hong Kong HSI is up 1.44%. China Shanghai SSE is up 0.19%. Singapore Strait Times is down -0.27%. Japan 10-year JGB yield is down -0.002 at 0.772. Overnight, DOW rose 0.40%. S&P 500 rose 0.52%. NASDAQ rose 0.58%. 10-year yield dropped -0.142 to 4.655.

Fed’s Kashkari expresses perplexity over rising treasury yields

Minneapolis Fed President Neel Kashkari expressed a sense of bewilderment regarding recent surge in 10-year Treasury yields. He noted yesterday, “The 10-year Treasury yield has gone up quite a bit. It’s a little bit perplexing what is driving them to go up as much as they have in recent months.”

He outlined a spectrum of possible explanations, from growing investor optimism about long-term economic strength to expectations of a more aggressive Fed stance on curbing inflation. Additionally, the rise in debt issued by the federal government could be another influencing factor.

“It is that combination of factors that is a little bit puzzling right now,” Kashkari commented, reflecting the multifaceted nature of the economic signals currently at play.

The relationship between inflation and long-term yields was another topic Kashkari addressed. He acknowledged the potential of elevated long-term yields to aid in reining in inflation, saying, “It’s certainly possible that higher long-term yields may do some of the work for us in terms of bringing inflation back down.”

However, he introduced a caveat – if these yields are reflective of changed expectations about the Fed’s actions, a conformity to these anticipations might be necessary to sustain the yields.

“But if those higher long-term yields are higher because their expectations about what we’re going to do has changed, then we might actually need to follow through on their expectations in order to maintain those yields,” he added.

Looking to the immediate future, Kashkari reiterated what he shared last month, suggesting there’s a 60% chance Fed would implement one more rate hike this year.

Fed’s Daly: Risks of over- and under-tightening roughly balanced

San Francisco Fed President Mary Daly noted overnight that the risks of over-tightening versus under-tightening are currently “roughly balanced”.

The tightening of financial conditions, as indicated by surging treasury yields, may influence the extent of Fed’s policy adjustments.

Daly noted, “If that’s tight, maybe the Fed doesn’t need to do as much. That’s why I said, depending on whether it unravels, or whether the momentum in the economy changes, that could be equivalent to another rate hike.”

However, Daly remains watchful, indicating that depending on economic momentum and other variables, “that could be equivalent to another rate hike.”

Beyond domestic considerations, Daly expressed concerns about “geopolitical uncertainty,” noting its potential impact on the US economy.

The repercussions of international events on elements like oil prices and export demand are being closely monitored by the Fed. She encapsulated the Fed’s vigilant stance by stating, “It’s part of a large dashboard of data”

RBA’s Kent: Some further tightening may be required

In a speech, RBA Assistant Governor, Chris Kent, indicated that while the effects of previous monetary tightening have not yet been fully realized, “some further tightening ” might be on the horizon to keep inflation in check.

Kent asserted that the policies currently in place are beginning to stymie demand growth, a crucial step towards mitigating inflation.

“The lags of transmission mean that some further effects of rate increases to date are still to be felt through the economy, which will provide further impetus to lower inflation in the period ahead,” he added.

However, with inflation persisting at elevated levels, Kent hinted at the necessity for additional measures. “The Board is paying close attention to economic developments here and overseas, and some further tightening of monetary policy may be required to ensure that inflation, which is still too high, returns to target in a reasonable timeframe.”

Looking ahead

European calendar is empty. Main focuses are US PPI and FOMC minutes.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2235; (P) 1.2263; (R1) 1.2314; More

GBP/USD’s break of 1.2270 resistance suggests that a short term bottom was already formed at 1.2036, after hitting 1.2075 fibonacci level. Intraday bias is back on the upside. Firm break of near term channel resistance (now at 1.2347) will target 38.2% retracement of 1.3141 to 1.2036 at 1.2458 next. Nevertheless, break of 1.2161 minor support will revive near term bearishness and bring retest of 1.2036 low.

In the bigger picture, fall from 1.3141 medium term top could still be a correction to up trend from 1.0351 (2022 low) only. But risk of complete trend reversal is rising. Sustained break of 38.2% retracement of 1.0351 to 1.3141 at 1.2075 will pave the way to 61.8% retracement at 1.1417. For now, risk will stay on the downside as long as 55 D EMA (now at 1.2440) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | EUR | Germany CPI M/M Sep F | 0.30% | 0.30% | ||

| 06:00 | EUR | Germany CPI Y/Y Sep F | 4.50% | 4.50% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Sep F | -17.60% | |||

| 12:30 | CAD | Building Permits M/M Aug | -1.50% | |||

| 12:30 | USD | PPI M/M Sep | 0.40% | 0.70% | ||

| 12:30 | USD | PPI Y/Y Sep | 1.60% | |||

| 12:30 | USD | PPI Core M/M Sep | 0.20% | 0.20% | ||

| 12:30 | USD | PPI Core Y/Y Sep | 2.20% | |||

| 18:00 | USD | FOMC Minutes |