Dollar is showing impressive strength in the early US session, boosted by job growth figures that nearly doubled market predictions. While wage growth figures mildly underwhelmed, it didn’t deter traders’ enthusiasm, propelling the Dollar to potentially conclude the week as the dominant currency.

Notably, Dollar has made up for its earlier losses against Yen, stemming from Japan’s intervention. Market watchers are now keenly observing if USD/JPY pair has the vigor to assault 150 psychological mark again and if this could precipitate another round of intervention from Japan.

Elsewhere, the Canadian Dollar is also witnessing an uplift, buoyed by its own positive employment figures. However, Loonie still lags as one of this week’s underperformers, together with Australian and New Zealand Dollars. This is largely attributable to the preceding plunge in oil prices. The impending question is whether prevailing risk aversion in the market could exacerbate the decline in these commodity currencies. European majors are ceding ground to the resurgent dollar but are managing to hold their own against the commodity currencies and yen.

The pivotal question is whether Dollar can capitalize on the current surge of buying interest to surpass recent highs against other major currencies. Alternatively, it might require an additional boost, potentially from the U.S. CPI data slated for release next week.

From a technical standpoint, key levels to watch include 1.0447 support in EUR/USD, 1.2036 support in GBP/USD, 0.6284 support in AUD/USD, 0.9243 resistance in USD/CHF, 150.15 resistance in USD/JPY, and 1.3784 resistance in USD/CAD.

In Europe, at the time of writing, FTSE is up 0.16%. DAX is up 0.26%. CAC is up 0.21%. Germany 10-year yield is up 0.081 at 2.961. Earlier in Asia, Nikkei dropped -0.26%. Hong Kong HSI rose 1.58%. Singapore Strait Times rose 0.61%. Japan 10-year JGB yield dropped -0.0025 to 0.803.

US NFP soars 336k in Sep, double of expectations

US non-farm payroll employment rose 336k in September, well above expectation of 168k. That’s also well above the average monthly growth of 267k over the prior 12 months. Prior month’s figure was also revised up from 187k to 227k.

Unemployment rate was unchanged at 3.8%, versus expectation of a drop to 3.7%. Labor force participation rate was unchanged at 62.8%.

Average hourly earnings rose 0.2% mom to USD 33.88, below expectation of 0.3% mom. Over the past 12 months, average hourly earnings have increased by 4.2% yoy.

Canada employment grew 64k in Sep, unemployment rate unchanged at 5.5%

Canada employment grew 64k in September, well above expectation of 28.0k. On average, employment has grown by 30,000 per month since the beginning of the year.

Unemployment rate was unchanged at 5.5% for the third consecutive month. Employment rate rose 0.1% to 62.0%, offsetting the decline recorded in August.

On a year-over-year basis, average hourly wages rose 5.0% yoy, up from 4.9% yoy in August, same as July’s figure.

ECB’s Schnabel warns against complacency, “last kilometre” the most difficult

In an interview with Jutarnji List, ECB Executive Board Isabel Schnabel underlined the unpredictability surrounding the current inflation trajectory, cautioning against premature optimism despite recent encouraging data.

Schnabel stated, “We cannot say that we are at the peak (interest rates) or for how long rates will need to be kept at restrictive levels.”

She emphasized the importance of closely monitoring three key metrics to make future monetary policy decisions: inflation outlook, dynamics of underlying inflation, the efficacy of monetary policy transmission. Encouragingly, she noted that “all of them are moving in the right direction.”

However, the Board member didn’t shy away from highlighting possible headwinds. She pointed out, “I still see upside risks to inflation,” flagging potential supply-side shocks and stronger-than-anticipated wage growth, which could be offset by lower productivity growth. Firms might also face difficulty in absorbing these increased costs, which, if realized, could necessitate further hikes in interest rates.

While Schnabel acknowledged the downward trend in inflation as “encouraging,” she emphasized that it still remains considerably above the ECB’s 2% target. The aim, she said, should be to hit this target by 2025 to ensure inflation expectations “firmly anchored”. However, she cautioned about the challenges in reaching this goal, noting that the “last kilometre” may be the most challenging.

The recent surge in oil prices was another point of concern for Schnabel, suggesting that inflation could face upward pressures from unforeseen supply shocks, especially in sectors like energy and food. She added a call for vigilance, urging that “we must not be complacent, and we should not declare victory over inflation prematurely.”

Japanese wages growth underwhelm as real income sinks for 17th mth

Subdued wage growth data in Japan is raising eyebrows, particularly at BoJ. An essential element for the central bank’s policy normalization is the establishment of a harmonious cycle between wage growth and prices. The recent figures, however, indicate that this equilibrium remains elusive.

In August, labor cash earnings in Japan rose by a meager 1.1% yoy. This increase, while consistent with the prior month, fell short of the anticipated 1.5% growth. Furthermore, base salary growth, although increasing to 1.6% yoy from the preceding month’s 1.4%, has yet to manifest signals of a robust and sustainable upward momentum.

The bright spot, perhaps, is the increase in overtime pay, which is often used as an indicator of business vibrancy, as 1.0% yoy ascent was observed, rebounding from July’s flat growth.

However, inflation-adjusted real wages continued their downward spiral for the 17th consecutive month. August’s real wages declined by -2.5% yoy, surpassing the projected -2.1% yoy dip. This trend starkly reveals that despite any increments, wages are struggling to keep up with the consistent price surges, placing added strain on the average consumer’s pocket.

Also released, household spending, a critical driver of economic activity, contracted by -2.5% yoy, a figure that, while better than the anticipated -4.3% yoy decline and an improvement from July’s -5.0% yoy reduction, still underscores constrained consumer expenditure.

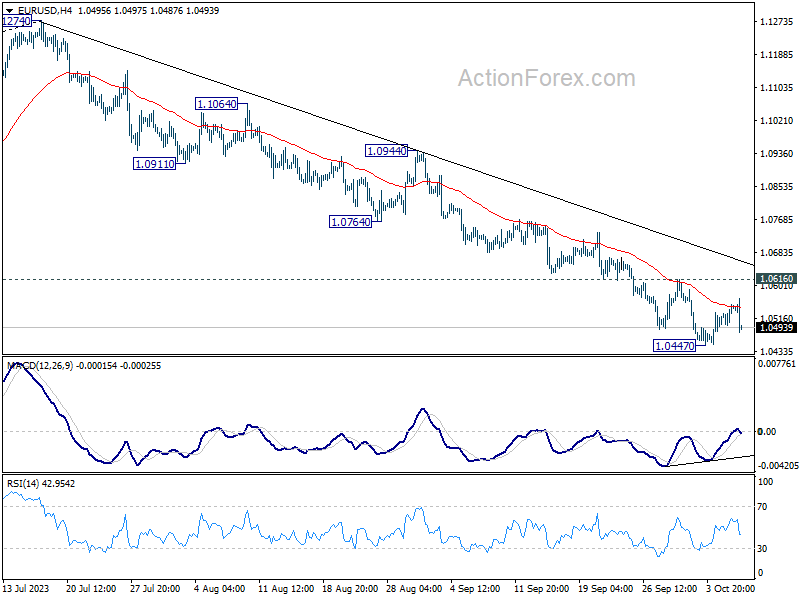

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0517; (P) 1.0534; (R1) 1.0569; More…

EUR/USD falls notably after rejection by 55 4H EMA but stays above 1.0447 support. Intraday bias remains neutral first. Outlook will stay bearish as long as 1.0616 resistance holds. Break of 1.0477 will resume the fall from 1.1274 to 1.0199 fibonacci level next. Nevertheless, firm break of 1.0616 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

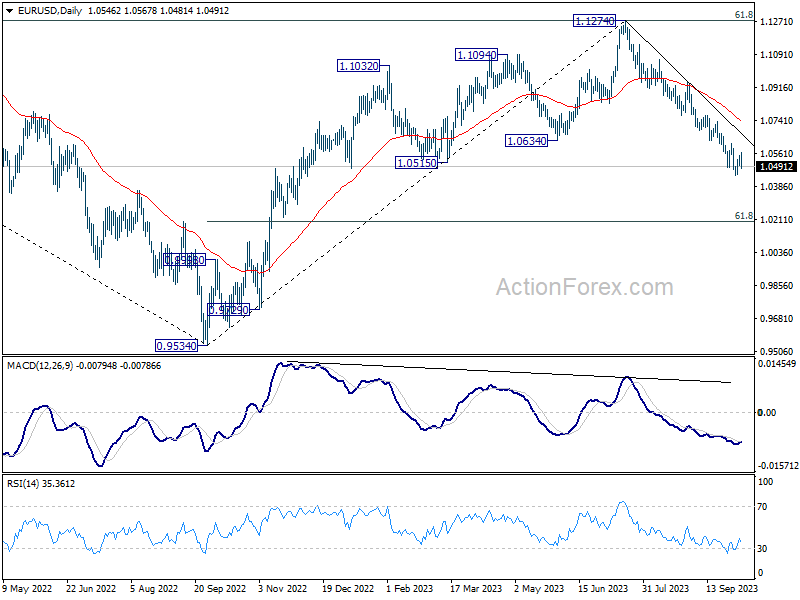

In the bigger picture, fall from 1.1274 medium term top could still be a correction to rise from 0.9534 (2022 low). But chance of a complete trend reversal is rising. In either case, current fall should target 61.8% retracement of 0.9534 to 1.1274 at 1.0199 next. For now, risk will stay on the downside as long as 55 D EMA (now at 1.0759) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Aug | 1.10% | 1.50% | 1.30% | 1.10% |

| 23:30 | JPY | Overall Household Spending Y/Y Aug | -2.50% | -4.30% | -5.00% | |

| 05:00 | JPY | Leading Economic Index Aug P | 109.5 | 109 | 108.2 | |

| 05:45 | CHF | Unemployment Rate Sep | 2.10% | 2.10% | 2.10% | |

| 06:00 | EUR | Germany Factory Orders M/M Aug | 3.90% | 1.50% | -11.70% | -11.30% |

| 06:45 | EUR | France Trade Balance (EUR) Aug | -8.2B | -8.9B | -8.1B | |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Sep | 678B | 694B | ||

| 08:00 | EUR | Italy Retail Sales M/M Aug | -0.40% | 0.00% | 0.40% | |

| 12:30 | USD | Nonfarm Payrolls Sep | 336K | 168K | 187K | 227K |

| 12:30 | USD | Unemployment Rate Sep | 3.80% | 3.70% | 3.80% | |

| 12:30 | USD | Average Hourly Earnings M/M Sep | 0.20% | 0.30% | 0.20% | |

| 12:30 | CAD | Net Change in Employment Sep | 63.8K | 28.0K | 39.9K | |

| 12:30 | CAD | Unemployment Rate Sep | 5.50% | 5.60% | 5.50% |