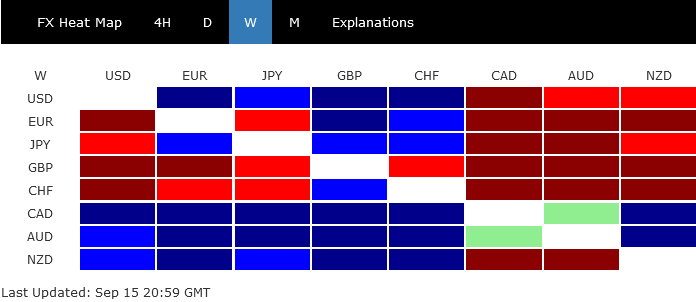

Commodity currencies were the biggest winners last week as the global tightening cycle draw closer to a prolonged pause. There was some optimism that China’s economy is moving past the worst with improving economic data. The change in sentiment also lift oil prices, which was already lifted by tight supply outlook, and feed back into the currency markets.

While Euro was under some selling pressure after ECB’s dovish hike, the situation was not disastrous. ECB was the most recent one to indicate explicitly that interest rates have possibly peaked. But it shouldn’t be the only central bank. Indeed, the single currencies was just the third worst performer, with Sterling and Swiss France being worse.

Dollar and Yen ended mixed, up against European but down against commodity currencies. The development argues that Dollar traders were indeed holding their bets ahead of FOMC rate decision, which is just a few days away. Dollar index is now pressing a key near term resistance zone and would probably reveal next move soon.

Dollar Index presses key resistance zone, fate on hands of Fed

Last week saw Dollar index continue its recent rally, peaking at 105.43 before settling at 105.32. This surge was significantly buoyed by a sell-off in Euro, although the downward momentum of EUR/USD seemed to decelerate upon reaching the 1.0634 support level. Parallelly, the breach of 147.88 resistance by USD/JPY seemed to lack conviction, leaving the fate of Dollar index in the critical resistance area between 150.37/88 hanging in the balance.

As the ripple effects of ECB’s rate decision potentially subside, market attention is pivoting to the upcoming Fed and BoJ decisions, scheduled for Wednesday and Friday, respectively. The overwhelming consensus is that Fed will maintain its current interest rate range of 5.25-5.50%. Market speculations regarding further rate hikes have been inconsistent, akin to the unpredictability of a coin toss. Under the most optimistic assumptions, Fed is unlikely to cut interest rates until at least the coming June. However, such forecasts might undergo significant adjustments post revelation of Fed’s updated economic projections and dot plot. Concurrently, traders will be vigilant to any policy tweak by BoJ priming for a departure from negative interest rates in 2024.

Analyzing from a technical standpoint, rejection by 38.2% retracement of 114.77 to 99.57 at 105.37 and 105.88, followed by break of 104.42 support, will indicate short term topping in Dollar Index. Deeper decline would then be seen in the near term back to 55 D EMA (now at 103.42). That would at best render the medium-term outlook neutral.

Nevertheless, a steadfast break above the barrier at 105.37 and preferably past the 105.88 resistance could initiate a more substantial rally, possibly reaching 61.8% retracement at 108.96. For such an optimistic scenario to materialize, the greenback must assert itself robustly against both Euro and Yen.

No disastrous selling on Euro after ECB’s dovish hike

Euro found itself amidst a whirlpool of selling pressure, triggered predominantly by ECB’s dovish 25bps rate hike. Following the adjustment, the main refinancing and deposit rates now stand at 4.50% and 4.00%, respectively. However, ECB has indicated its intent to keep interest rates at this restrictive for an extended duration to steer inflation back to target.

Market sentiments have since solidified around expectation of a 25bps rate reduction by ECB by June of the upcoming year. This is in light of the central bank’s downgraded GDP growth projections spanning from 2023 to 2025. A growing cluster of analysts are voicing concerns about growth dynamics, which they perceive as a more pressing issue in comparison to inflation.

However, bucking the trend of widespread anticipation, Euro found some traction courtesy of ECB officials, including President Lagarde, who emphasized that rate cuts were not a topic of current discussions at the ECB. This support from ECB allowed Euro to finish the week on a stronger note against Sterling and Swiss Franc, albeit confined to a near-term range. In upcoming financial events, both BoE and SNB could make potentially their final rate hikes in this cycle.

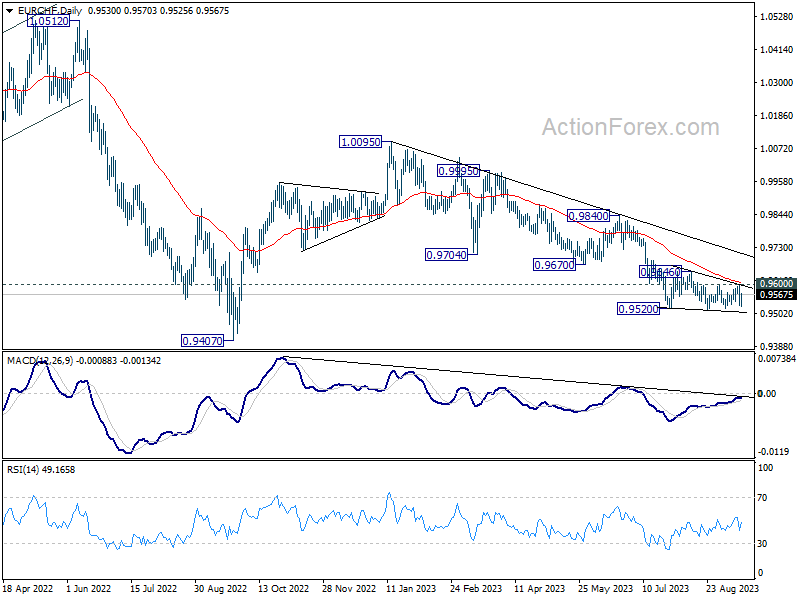

For EUR/CHF, being capped below falling 55 D EMA, risk remains on the downside. Another fall through 0.9513 to extend the down trend from 1.0095 remains in favor. But based on the current downside momentum as seen in D MACD, strong support could emerge above 0.9407 low to floor the cross, at least on first attempt.

WTI breaks 90 with three-week winning streak, ready for 100?

Oil prices soared to a ten-month high last week, marking their third consecutive weekly gain. The current pace indicates that oil is set for its most significant quarterly surge since the upheaval caused by Russia’s invasion of Ukraine in the early months of 2022.

Dominating the drivers behind this upsurge are the ongoing supply concerns. These concerns have been accentuated since Saudi Arabia and Russia jointly announced the continuation of their supply cut measures. The positive momentum was further bolstered by China’s economic data last week, indicating industrial production and retail sales performance surpassing expectations, thereby giving an added boost to oil prices.

Interestingly, the appetite among traders remains undeterred, even as prices are hovering above the 90 mark. This indicates a leaning towards further bullish movement, with oil market likely remaining tight for a bit more time. Yet, the market might still require a new significant driving force to propel oil prices into the triple-digit territory.

On the flip side, break of the 90 threshold has rekindled concerns surrounding inflation. As WTI oil inches further to 100, these apprehensions are likely to amplify, potentially disrupting inflation expectations and impeding the disinflation initiatives set by global central banks.

Technically, the break above 38.2% retracement of 131.82 to 63.67 at 89.70 is also significant. It opens the way to 61.8% retracement at 105.78, even if rise from 63.67 is a corrective move. But WTI would need to overcome the next near term hurdle first, 100% projection of 66.94 to 64.91 from 77.95 at 95.92. The momentum towards this projection level would be watched closely to gauge the odds of further rally beyond that.

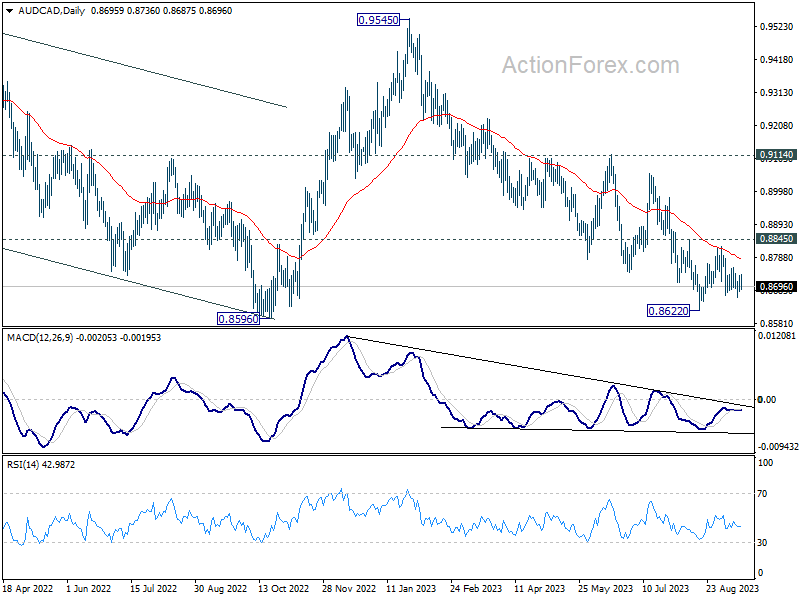

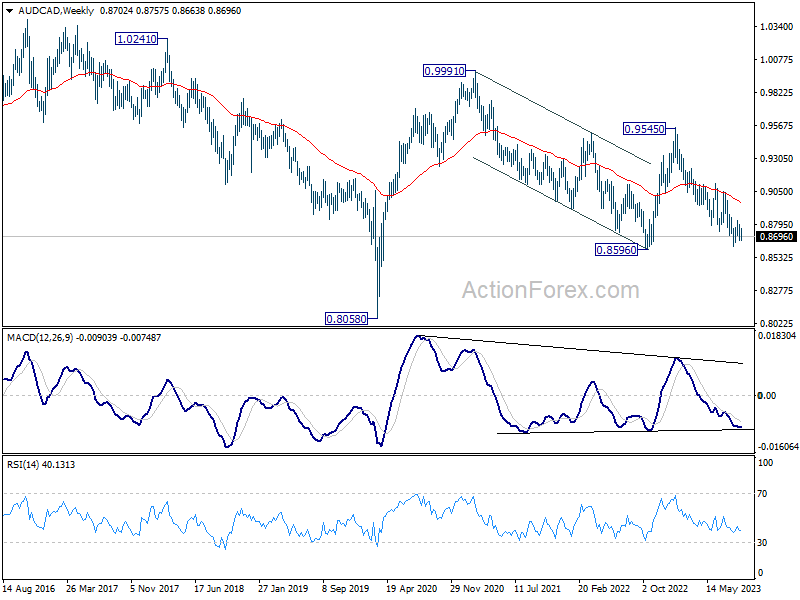

A deep dive into Aussie and Loonie as commodity currencies jumped

Commodity currencies showed remarkable strength last week, flourishing on the back of increasingly optimistic sentiment as anticipation builds around culmination of global tightening cycle. Australian Dollar enjoyed a boost, courtesy of encouraging economic figures pouring out of China. Simultaneously, Canadian Dollar rode the wave of rising oil prices. The vitality of these commodity currencies was especially pronounced when juxtaposed with European majors.

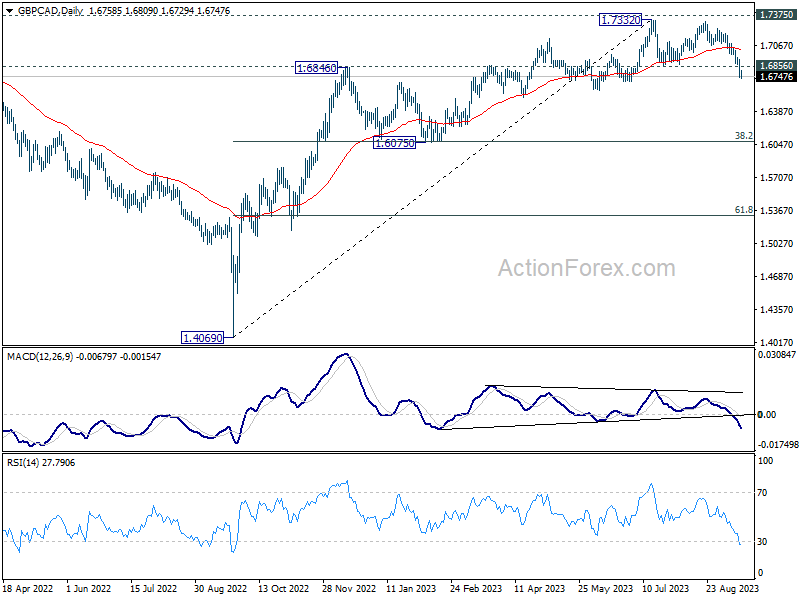

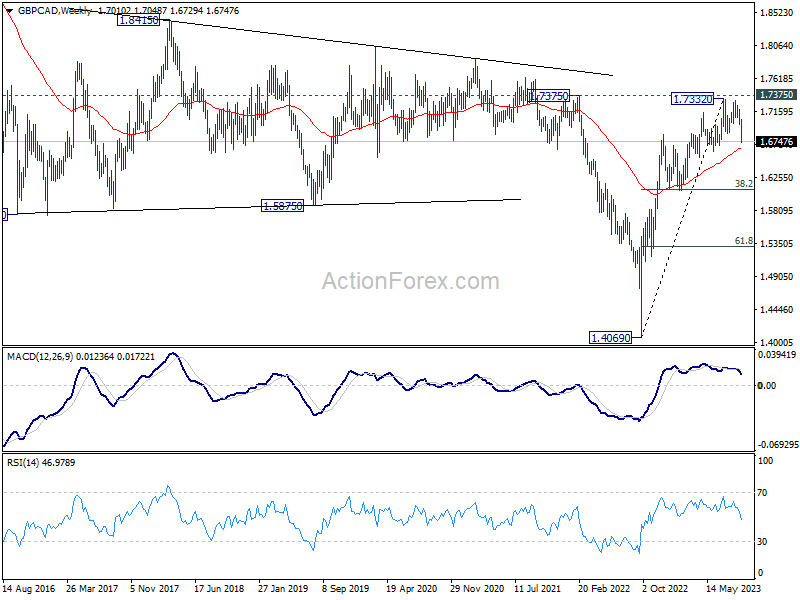

After accelerating down to 1.6729 last week, next focus for GBP/CAD is now on 55 W EMA (now at 1.6653). Sustained break there should confirm rejection by 1.7375 structural resistance, and that 1.7332 is medium term top. Fall from there would at least be a correction to whole rise from 1.4069 (2022 low). That would pave the way to 1.6075 cluster support (38.2% retracement of 1.4069 to 1.7332 at 1.6086) next.

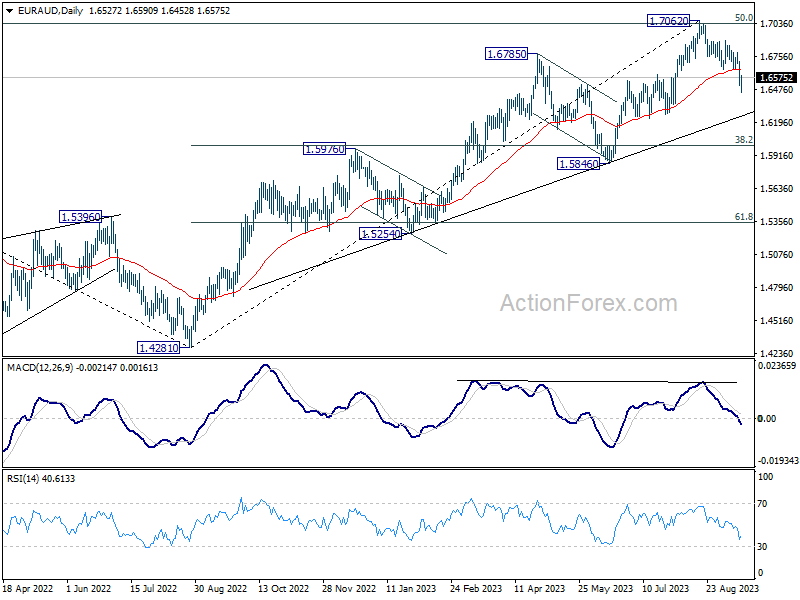

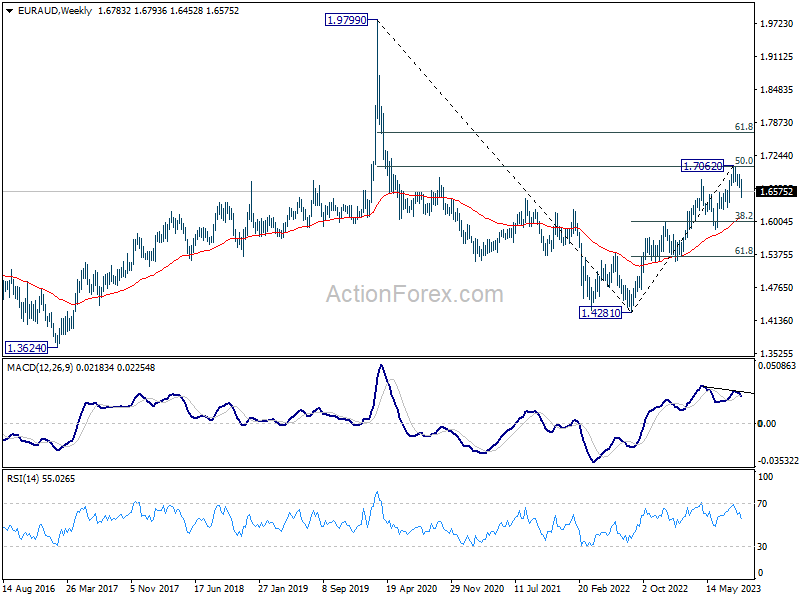

Considering bearish divergence condition in W MACD, EUR/AUD has also likely made a medium term top at 1.7062, after hitting 50% retracement of 1.9799 to 1.4281 at 1.7040. Fall from 1.7062 is likely correcting whole rise from 1.4281. Deeper decline is expected to 38.2 retracement of 1.4281 to 1.7062 at 1.6000.

Comparing Aussie and Loonie, AUD/CAD is still clearly staying in the down trend from 0.9545. Further fall will remain in favor as long as 0.8845 resistance holds. However, as the cross have struggle to build downside momentum for a few months already, downside potential below 0.8596 could be limited. On the other hand, firm break of 0.8845 could present bullish reversal opportunity for at least a take on 0.9114 resistance.

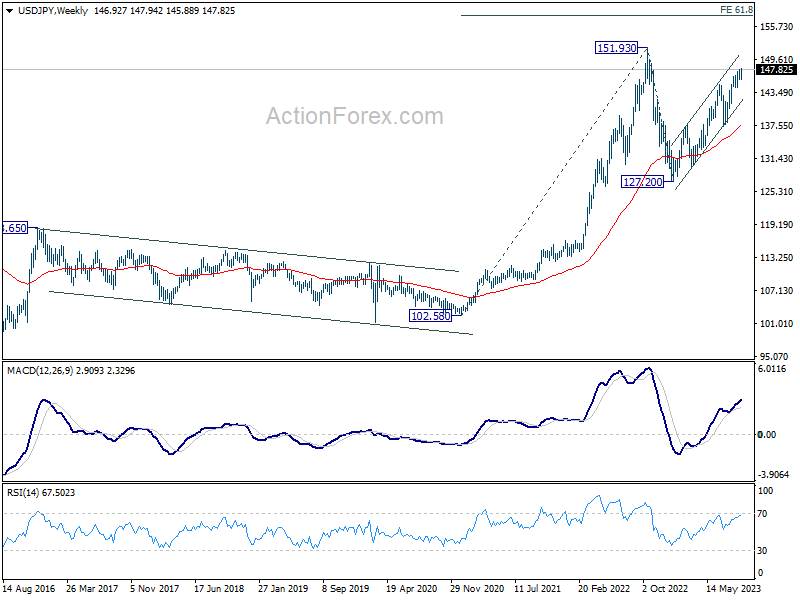

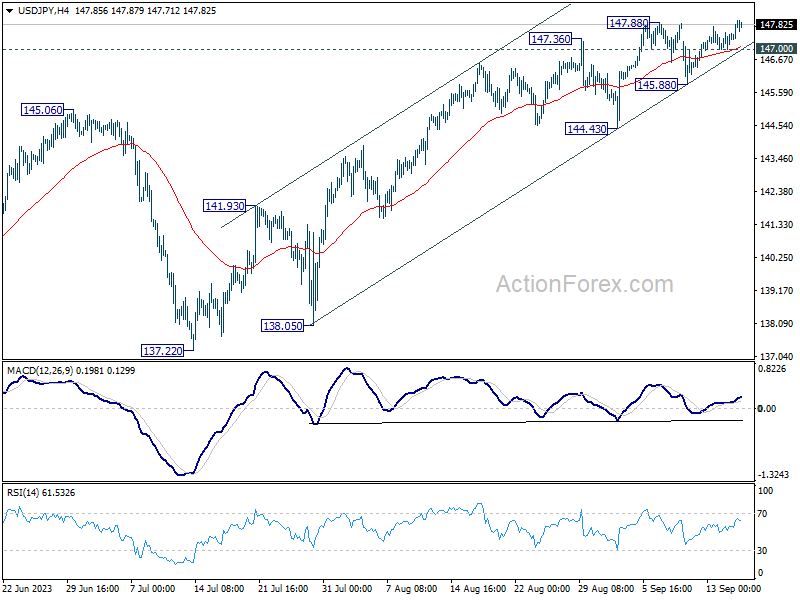

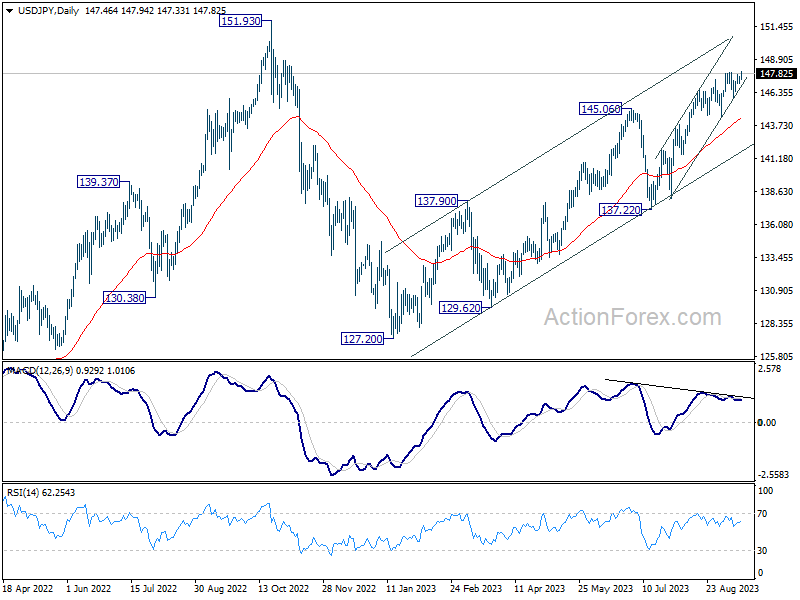

USD/JPY Weekly Outlook

USD/JPY’s late breach of 147.88 resistance suggests that rise from 127.20 is resuming. Initial bias is mildly on the upside this week for 151.93 high. On the downside, below 147.00 minor support will turn intraday bias neutral again first. But outlook will remain bullish as long as 145.88 support holds.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 137.22 support will indicate that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

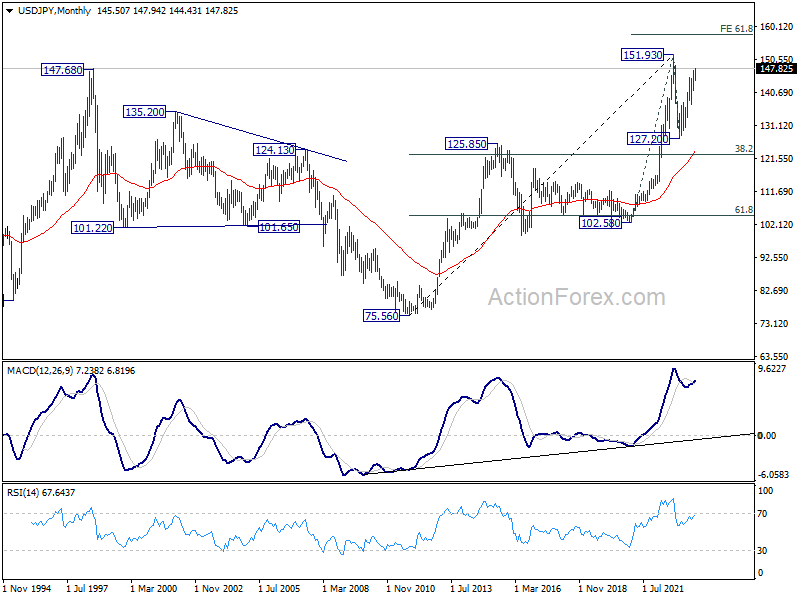

In the long term picture, price action from 151.93 is seen as developing into a corrective pattern to up trend from 75.56 (2011 low). Another falling leg could be seen, but in that case, downside should be contained by 38.2% retracement of 75.56 to 151.93 at 122.75. On resumption, next target would be 61.8% projection of 102.58 to 151.93 from 127.20 at 157.69.