As the trading week draws to a close, Dollar appears to be finally capitalizing on heightened risk aversion, extending its recent surge. Major European stock indexes are painting a gloomy picture, while US futures points to negative opens. British Pound, once the darling of the markets, has started to wane after an unexpectedly dismal retail sales report from the UK. Simultaneously, the Japanese Yen attempting a stronger rebound, especially against European and commodity currencies.

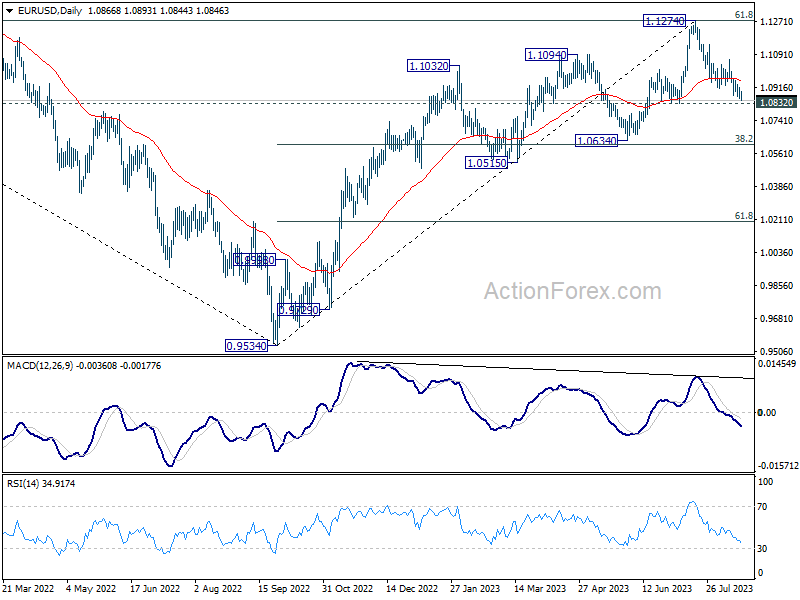

Technically, EUR/USD is now inching closer to 1.0832 support. Decisive break there will further solidify the case that it’s at least in correction to whole up trend from 0.9543. Deeper fall would be then seen to 1.0634 support next, which is close to 38.2.% retracement of the up trend from 0.9543 to 1.1274. If materializes, that would likely be accompanied by equally strong rally in the greenback elsewhere.

In Europe, at the time of writing, FTSE is down -0.99%. DAX is down -1.01%. CAC is down -1.06%. Germany 10-year yield is down -0.0827 at 2.627. Earlier in Asian Nikkei dropped -0.55%. Hong Kong HSI dropped -2.05%. China Shanghai SSE dropped -1.00%. Singapore Strait Times dropped -0.71%. Japan 10-year JGB yield dropped -0.0238 to 0.631.

Eurozone CPI finalized at 5.3% in Jul, core CPI at 5.5%

Eurozone CPI was finalized at 5.3% yoy in July, down from June’s 5.5% yoy. Core CPI (ex energy, food, alcohol & tobacco) was finalized at 5.5%, unchanged from June’s reading. The highest contribution came from services (+2.47%), followed by food, alcohol & tobacco (+2.20%),), non-energy industrial goods (+1.26%),) and energy (-0.62%),).

EU CPI was finalized at 6.1% yoy, down from prior month’s 6.4% yoy. The lowest annual rates were registered in Belgium (1.7%), Luxembourg (2.0%) and Spain (2.1%). The highest annual rates were recorded in Hungary (17.5%), Slovakia and Poland (both 10.3%). Compared with June, annual inflation fell in nineteen Member States, remained stable in one and rose in seven.

UK retail sales volumes down -1.2% in Jul, sales value down -1.0% mom

UK retail sales volumes dropped -1.2% mom in July, much worse than expectation of -0.4% mom. Ex-automotive fuel sales volume dropped -1.4% mom. In value term, sales dropped -1.0% mom while ex-fuel sales contracted -1.4% mom.

Food stores sales volumes fell by -2.6% mom. Non-food stores sales volumes fell by -1.7% mom. Automotive fuel stores sales volumes rose by 0.7% mom. Non-store retailing sales volumes rose by 2.8% mom.

ONS also noted, shoppers switching to online shopping because of poor weather and increased promotions led to 27.4% of retail sales taking place online in July 2023, up from 26.0% in June 2023; this is the highest proportion since February 2022 (28.0%).

Japan CPI core eased to 3.1% in Jul, but core-core back at four decade high

Japan’s core CPI, which excludes fresh food, eased slightly from 3.3% yoy in June to 3.1% yoy in July, aligning with market expectations. Notably, this metric continued its streak above BoJ’s 2% inflation target for a commendable 16 consecutive months.

Diving deeper, core-core CPI, which subtracts both fresh food and energy, inched higher to 4.3% yoy, equalling the peak seen in May. This current rate hasn’t been witnessed since 1981, underscoring the latent inflationary pressures within the Japanese economy.

Processed food costs are a particular hotspot, skyrocketing by 9.2% yoy – a surge not seen in nearly half a century. Adding to this, durable goods saw a robust rise of 6.0% yoy. Furthermore, possibly driven by travel and vacationing demand, accommodation fees witnessed a significant 15.1% yoy hike during the prime summer holiday period.

Conversely, energy prices painted a contrasting picture, plummeting by -8.7% yoy. This decline can largely be attributed to government interventions, with subsidies introduced to mitigate household utility expenses. These subsidies, in turn, have played a pivotal role, dragging the core CPI lower by approximately one percentage point.

Service prices also shifted gears, moving up to 2% yoy from 1.6% yoy – the most substantial leap since 1993 if we set aside the aftermath of the 1997 sales tax hike.

Despite these intricate dynamics, headline CPI remained steadfast at 3.3% yoy.

RBNZ Silk: Housing the biggest upside risks to inflation

RBNZ Assistant Governor Karen Silk said today, “Near term, there are still some risks on the upside to inflation.” She further identified the housing market as a significant factor, mentioning, “The OCR track is slightly higher and we’re saying potentially retaining rates at a higher level for longer. Probably the biggest driver of that is really housing.”

The bank’s recent projections indicate that OCR could reach its peak at 5.59% by mid-2024, and then slightly pull back to 5.36% by early 2025. This revised forecast surpasses earlier predictions laid out in the previous Monetary Policy Statement.

Silk expressed uncertainty regarding how the stability observed in the housing market, combined with a potential recovery next year, might impact inflation.

“We are looking at it as a gradual resumption in house price trend,” Silk elaborated, “but in an environment where labor market pressures continue to ease and at the same time you’ve got a higher interest rate environment.”

Additionally, Silk pointed out broader concerns beyond the local scenario. “One of the medium-term risks for us is global growth,” she said. Expressing a keen interest in international trajectories, she added, “We’re really focused on global growth and in particular how weak is China. Is China really going to be able to deliver the growth that they’re suggesting?”

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8761; (P) 0.8785; (R1) 0.8810; More….

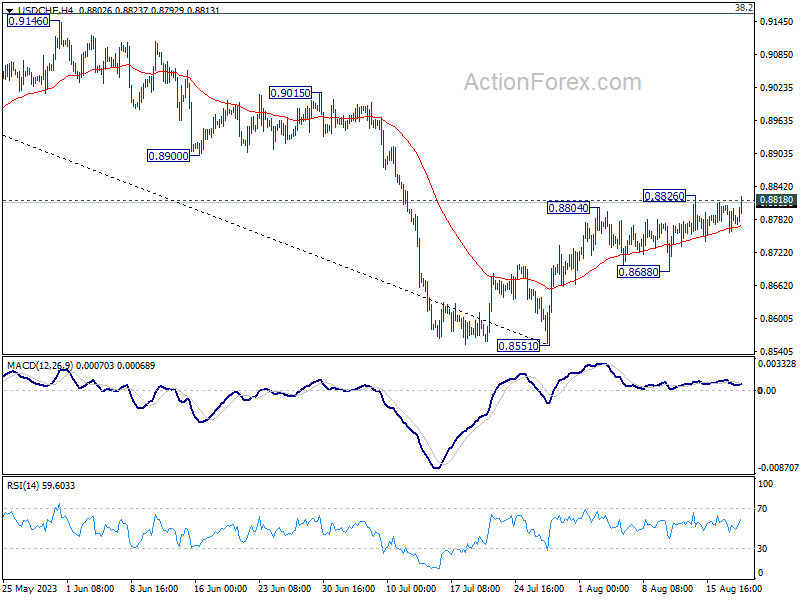

USD/CHF rises slightly again after drawing support from 55 4H EMA (now at 0.8770). Immediate focus is back on 0.8818 support turned resistance and 0.8826 temporary top. Decisive break there will carry larger bullish implication. Further rally should then be seen to 0.9146 cluster resistance next. However, break of 0.8688 support will indicate rejection by 0.8818, and turn bias back to the downside for retesting 0.8551 low.

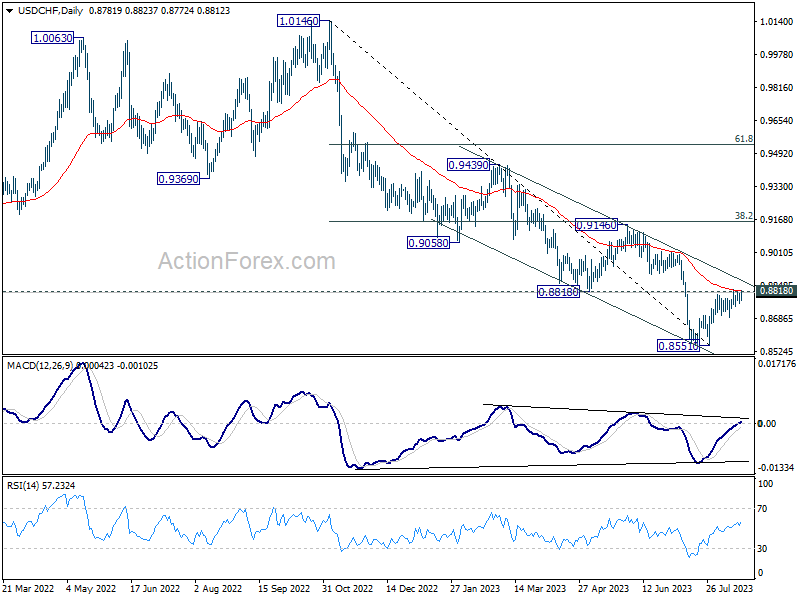

In the bigger picture, a medium term bottom could be in place at 0.8551 already, on bullish convergence condition in D MACD. Sustained trading above 0.8818 will bring further rise to 0.9146 cluster resistance (38.2% retracement of 1.0146 to 0.8551 at 0.9160), even as a correction. Nevertheless, break of 0.8851 will resume the down trend from 1.0146 instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Y/Y Jul | 3.30% | 3.30% | ||

| 23:30 | JPY | National CPI ex-Fresh Food Y/Y Jul | 3.10% | 3.10% | 3.30% | |

| 23:30 | JPY | National CPI ex Food Energy Y/Y Jul | 4.30% | 4.20% | ||

| 06:00 | GBP | Retail Sales M/M Jul | -1.20% | -0.40% | 0.70% | 0.60% |

| 09:00 | EUR | Eurozone CPI Y/Y Jul F | 5.30% | 5.30% | 5.30% | |

| 09:00 | EUR | Eurozone Core CPI Y/Y Jul F | 5.50% | 5.50% | 5.50% | |

| 12:30 | CAD | Industrial Product Price M/M Jul | 0.40% | 0.20% | -0.60% | |

| 12:30 | CAD | Raw Material Price Index Jul | 3.50% | 2.10% | -1.50% |