The strongest to the weakest of the major indices

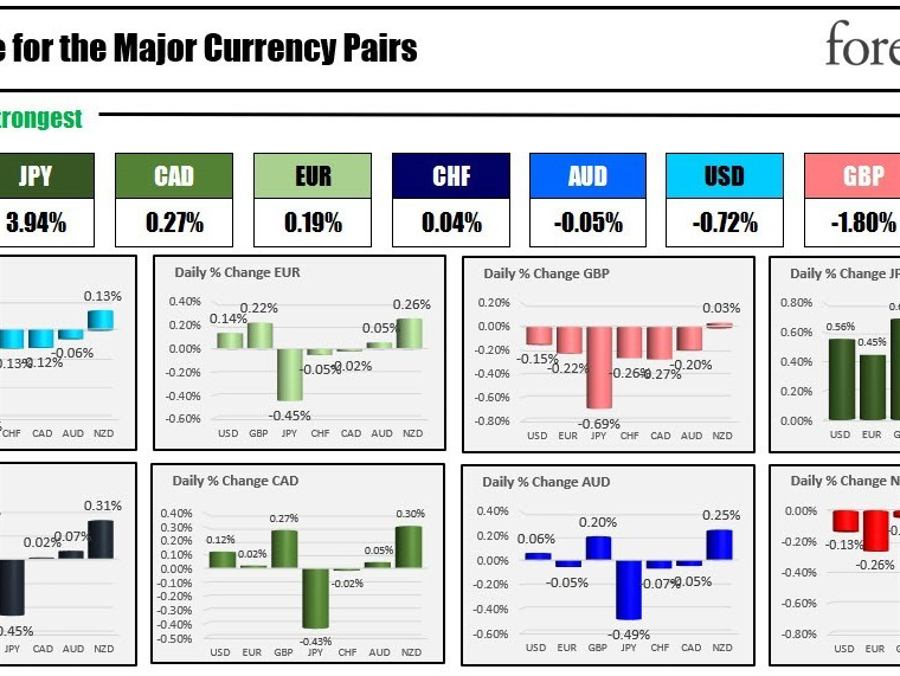

The JPY is the strongest and the NZD is the weakest as the NA session begins

Overnight, the Reserve Bank of New Zealand (RBNZ) decided to maintain its official cash rate (OCR) at 5.5%, a move that was broadly anticipated by the market. The decision was made to help control inflation and spending while ensuring the sustainability of employment levels. RBNZ officials noted in a statement that global economic growth is softening, and international inflation rates are decreasing, facilitated by factors like the normalization of global supply chains, reducing shipping costs, and falling energy prices. These factors have also led to lower export prices for New Zealand’s goods. Domestically, inflation is projected to continue falling from its peak, with core inflation also expected to decrease as capacity constraints are eased. Although employment is above the optimal sustainable level, the labor market is showing signs of easing pressure, with job vacancies in decline. RBNZ remains confident that keeping interest rates at a restrictive level for an extended period will steer consumer price inflation back to its target range of 1 to 3% per annum.

The NZDUSD moved higher ahead of the decision and in the process extended above the highs from last week and this week between 0.62186 to 0.62235. The price reached 0.62383 before rotating back lower. The lows have reached a cluster of moving averages defined by the 200-hour MA, 200-day MA, 100-day MA, and 100-hour MA between 0.6173 to 0.6190. The low just reached 0.6183 and trades at 0.6189. That area will be a key barometer going forward for the pair technically. If the dip buyers come in here, the ups and downs could continue back to the aforementioned swing area. Conversely, continuing to move lower, a break below the 200-hour MA would open the down for a retest of 38.2% and lows from Monday and Tuesday at 0.6166 (move below is even more bearish in the short term at least (see chart below).

NZDUSD falls to cluster of MAs

In Australia, Reserve Bank of Australia Governor Lowe offered insights on the economic situation and policy direction, highlighting potential further tightening to guide inflation back to its target. He acknowledged the complicated and uncertain outlook on inflation and indicated that the upcoming August meeting would consider updated economic forecasts and new data. Despite a “significant and rapid” tightening of monetary policy, Lowe asserted that the full effects are yet to be felt due to the inherent lags in the system. The Governor projected subdued economic growth over the next few years, and a consequent slow return of inflation to the target range. Lowe expressed a firm commitment to bringing inflation back to target within a reasonable timeframe, underscoring that he is “deadly serious” about achieving this goal. He expressed confidence that higher interest rates are having their intended impact and kept an open stance on potential further tightening of monetary policy.

IN the UK today, the BOE released its latest financial stability report and warned of significant uncertainty in the global economic outlook and an increasingly challenging risk environment. Higher interest rates on loans present potential difficulties for borrowers, posing increased risk to banks. However, the BOE maintains that UK banks are resilient and well-prepared to support customers who may struggle with repayments, due in part to their robust capital buffers and a maintained counter cyclical capital buffer at 2%. The stress test results suggest that UK banks would remain stable even under worse-than-expected economic conditions. Despite the challenges faced by UK households due to rising living costs and interest rates, the report underscores the strength of the UK banking system.

Staying on central banks, today the Bank of Canada will announce their rate decision at 10 AM ET, with expectations of a 25 basis point hike to 5.0%. It would be the 2nd consecutive meeting where the bank raised the rates by 25 basis points. The hikes come after 3 months when the bank had a “conditional pause”.

Focus will be on how the BOC sees rates going forward. Growth in Canada for the 1st quarter was at 3.1% and it is tracking close to 2% in the 2nd quarter (but expected to move lower in the 2H). Inflation declined to an annual rate of 3.4% as a result of base effects. The bank does not see inflation return it to 2% target until 2025. Like in the US core inflation remains sticky.

The Bank of Canada will update its growth/inflation projections. Analysts expect:

- 2023 CPI to rise to 3.7% from 3.5%

- 2024 CPI is expected to remain unchanged at 2.3%

For GDP:

- 2023 GDP expected at 1.3% versus 1.4% last

- 2024 CPI expected at 1.0% versus 1.3% last

On the economic calendar, the US CPI data will be released at 8:30 AM. Although the numbers are not likely to impact the July Fed decision (a 25 bp hike is pretty much all baked in the cake), it COULD be a difference between one more hike and no more hikes in 2023. Expectations for the numbers show:

- CPI MoM 0.3% versus 0.1% last month

- CPI ex-food and energy is expected to rise by 0.3% versus 0.4% last month

- CPI YoY is expected to fall sharply to 3.1% from 4.0%. This is as a result of base effects. More specifically a year ago, the CPI increased by 1.3%. That number will drop out of the equation and be replaced by a much lower number. If the MoM number increases by 0.1% or less, the YoY could see a sub-3.0% level

- CPI ex-food and energy is expected to dip to 5.0% from 5.3%. The MoM from a year ago was 0.7%. Like the headline number, a MoM gain of 0.2% or 0.1% (or lower) could see a YoY fall to less than 5%.

Services less energy rose by 6.6% YoY last month. That component of CPI accounts for 58% of the total CPI. The biggest component of that calculation is the Shelter component (34.56% of total CPI). The shelter component is up 8.0% on the year and rose by 0.6% last month. Analysts and traders keep on looking for an easing of that component. Will it happen this month or will the trend continue that helps to keep service/core prices sticky?

Later today, the US treasury will auction off 10 year notes at 1 PM ET. And at 2 PM, the US Federal Reserve will release their beige book which outlines the anecdotal trends in the US economy ahead of the next FOMC rate decision later this month.

Earlier today, the weekly Mortgage data was released in the US. The Mortgage Bankers Association (MBA) report showed that mortgage applications increased by 0.9% despite higher rates. The Refinance Index also saw a slight increase, from 206.5 to 208.4. The 30-year mortgage rate climbed from 6.85% to 7.07%, reflecting the rise in US treasury yields.

Crude oil is trading up $0.32 or 0.43% at $75.15. The 100-day moving average comes in at $73.71 today. Yesterday the price moved above – and closed above – that moving average. The swing high from June 5 comes in a $75.06 That target has now been reached and breached with a high of $75.25. The 200-day moving average is $77.33. A move back below the 100-day moving average would reverse the technical bias more in favor of the sellers. The 200-day MA target above has not been breached since August 2022.

In late NY session news yesterday, the private API inventory data showed:

- Crude build of 3.026 million. The expectations for EIA data today are for a build of 0.483M

- Gasoline build of 1.004 million. The expectations for EIA data today are for a drawdown of -0.727M

- Distillates build of 2.908 million. The expectations for EIA data today are for a drawdown of -0.262M

In other markets:

- Spot gold is trading up $2.33 or 0.12% at $1934.54

- Silver is trading up $0.04 or 0.19% at $23.16

- Bitcoin is trading at $30,759 after ending near $30,609 near 5 PM yesterday

In the premarket for US stocks, the major indices are trading higher. Yesterday, the indices closed higher for the 2nd consecutive day, led by the Dow 30 stocks.

- Dow Industrial Average is trading up 81 points. It rose 317.02 points yesterday

- S&P index is trading up 11.5 points. It rose 29.71 points yesterday

- NASDAQ index is trading up 56.7 points. It rose 75.21 points yesterday

Yesterday, Microsoft’s $69 billion megamerger with Activision Blizzard was granted a significant advantage, as a federal court judge dismissed U.S. antitrust concerns on Tuesday. The Federal Trade Commission had sought an injunction to prevent the merger, but U.S. District Judge Jacqueline Scott Corley ruled that the deal would not “substantially lessen competition” in video game subscription or cloud gaming markets. The decision caused Activision shares to rise by over 10%. Although concerns have been raised that Microsoft could exploit the purchase to dominate competition from companies like Nintendo and Sony’s PlayStation, the FTC only has until Friday to contest the decision. Meanwhile, attention has shifted to the UK’s antitrust watchdog, the Competition and Markets Authority (CMA), which initially blocked the merger but recently hinted at a potential softening of its stance if Microsoft adjusts the terms of the Activision deal.

Shares of Microsoft are trading at $333.91 after settling at $332.47 yesterday. Activision shares our trading at $89.80. That is down from the close price of $90.99 yesterday.

In the European equity markets, the major indices are trading higher. Yesterday the major indices all rose led by France’s CAC:

- German DAX is up 0.96%. Yesterday the index rose 0.75%

- France’s CAC is up 0.80%. Yesterday the index rose 1.07%

- UK’s FTSE 100 is up 1.4%. Yesterday the index rose 0.12%%

- Spain’s Ibex is up 0.47%. Yesterday the index rose 0.85%

- Italy’s FTSE MIB is 1.0% (delayed). Yesterday the index rose 0.68%

In the Asian Pacific market today, markets closed mixed:

-

Japan’s Nikkei 225 -0.81%

-

China’s Shanghai Composite -0.78%

-

Hong Kong’s Hang Seng +1.08%

-

Australia’s S&P/ASX 200 +0.38%

In the US debt market, yields are lower in early US trading

- 2-year yield 4.843%, -5.3 basis points

- 5-year yield 4.187%, -5.0 basis points

- 10-year yield 3.942%, -4.0 basis points

- 30-year yield 4.006%, -1.5 basis points basis points

In the European debt market, benchmark 10-year yields are lower.

European 10 year yields