Clear direction is yet to be established in the forex markets this week, with the exception of Yen’s continued depreciation, albeit at a slow pace. Canadian Dollar’s rally, spurred by CPI data, was abruptly halted due to worsening risk sentiment, marked by DOW’s over -330pts drop. US Treasury Secretary Janet Yellen amplified her warning about the urgent need to increase the debt limit, cautioning that failure to do so could result in “a number of financial markets break – with worldwide panic triggering margin calls, runs and fire sales.”

Currently, most major pairs and crosses remain within last week’s range, with the exceptions of USD/JPY, GBP/CAD, and AUD/CAD. Yen, Dollar, and Euro are showing weakness, while New Zealand Dollar, Canadian Dollar, and Swiss Franc are demonstrating strength. Aussie and Sterling are mixed. Considering the sparse economic calendar for today and tomorrow, trading may continue to be subdued. However, Australian Dollar could see some action tomorrow with the release of Australian job data.

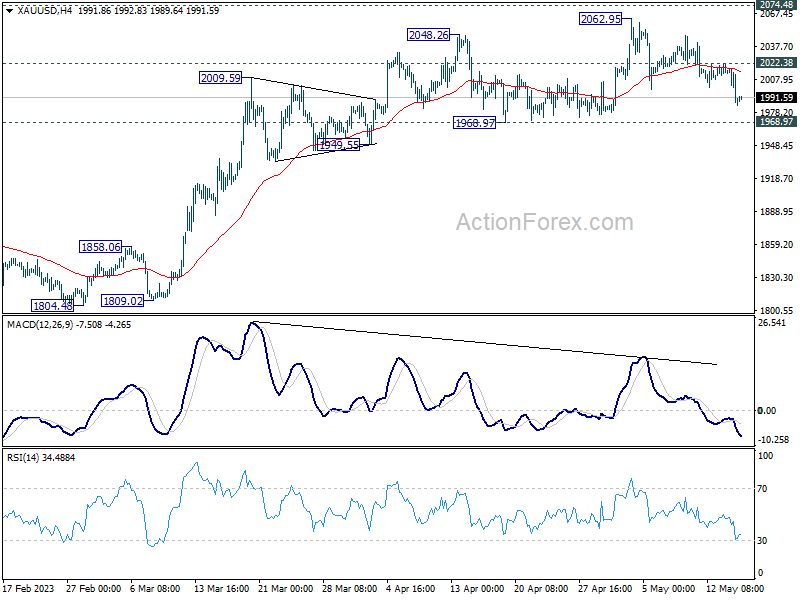

On the technical side, Gold is continuing its pullback from 2062.92 and has dipped below the 2000 mark. Near-term outlook remains bullish as long as 1968.97 support level holds. break of 2022.38 minor resistance could indicate readiness a rally resumption, potentially testing record high of 2074.48. However, firm break below 1968.97 could signal that near-term bearish reversal is already underway.

In Asia, at the time of writing, Nikkei is up 0.85%, back above 30k handle. Hong Kong HSI is down -0.55%. China Shanghai SSE is down -0.23%. Singapore Strait Times is down -0.83%. Japan 10-year JGB yield is down -0.0231 at 0.373. Overnight, DOW dropped -1.01%. S&P 500 dropped -0.64%. NASDAQ dropped -0.18%. 10-year yield rose 0.041 to 3.549.

Fed Logan: Slower tightening shouldn’t signal any less commitment

Dallas Fed President Lorie Logan semphasized the importance of a cautious approach to tightening monetary policy amidst uncertainty, suggesting that a slower pace doesn’t diminish commitment to achieving inflation goals.

Logan stated in a conference, “when conditions are uncertain, you may need to travel more slowly. But a slower pace of tightening shouldn’t signal any less commitment to achieving the inflation goal.” She further noted the potential for nonlinear deterioration of financial conditions, advocating for smaller, less frequent rate hikes to mitigate this risk.

Logan also underscored the multifaceted nature of monetary policy’s impact. She said, “The restrictiveness of monetary policy comes from the entire policy strategy – how fast rates rise, the level they reach, the time spent at that level and the factors that determine further increases or decreases.”

Seaprately, New York Fed President John Williams highlighted the time lag between policy decisions and their full impact on the economy, underlining the importance of monitoring the economy’s behavior post-decision. “We’ve got to make our decisions and then watch what happens, get that feedback, see how the economy’s behaving,” Williams explained.

In another occasion, Chicago’s Austan Goolsbee, however, indicated it may be too soon to discuss rate cuts or changes to monetary policy. He said, “I think it’s far too premature to be talking about rate cuts and premature to be saying — even for the next meeting — are we going to pause? Are we going to raise? Are we going to cut.”

Japan’s economy bounced back in Q1, up 1.6% annualized, 0.4% qoq

Japan’s economy delivered a robust performance in Q1, expanding at annualized rate of 1.6%, which significantly surpassed expectation of 0.7%. This marks the first expansion in three quarters, thanks to a potent combination of strong private consumption and a rebound in inbound tourism.

In terms of real GDP, adjusted for inflation, there was an increase of 0.4% qoq, beating the forecast growth of 0.1% qoq. The positive data signals a welcome resurgence in Japan’s economy, signaling a potential turn-around after short period of technical recession.

Looking into the details, private consumption for the quarter rose by 0.6%, driven by robust demand for cars and durable goods. Concurrently, consumers boosted spending on services such as dining out, culminating in the fourth consecutive quarterly gain. Meanwhile, capital spending rose by 0.9%, aided by increased car-related investments and marking the first increase in two quarters.

However, not all sectors exhibited positive trends. Exports took a hit, declining by -4.2% due to a slump in shipments of cars and machinery used for chip production. Imports also fell by 2-.3%. Public investment remained largely flat.

Australia wage growth accelerated to 0.8% in Q1, highest in over a decade

Australia wage price index posted 0.8% qoq increase in Q1 2023, slightly short of expected 0.9% rise. Despite this, annual wage growth accelerated to 3.7%, marking the highest level since Q3 2012. This uptick is attributable to a combination of factors, including low unemployment, tight labour market, and high inflation.

Private sector emerged as the primary engine of growth, with wages climbing 0.8% over Q1 and experiencing an annual rise of 3.8%. According to Leigh Merrington, ABS’s acting head of prices statistics, several private sector industries witnessed an annual wage growth exceeding 4%, with the remaining industries all recording an annual growth above 3%.

In the public sector, the highest quarterly (0.9%) and annual (3.0%) wage growth in a decade was reported. Increase in public sector wages is attributed to outcomes from enterprise agreement bargaining, regular scheduled rises, and higher wage caps.

Merrington further highlighted wage outcomes for Q1 2023, stating, “There was a continued lift in the share of jobs receiving wage rises of between 4 and 6 per cent, which is the highest share since 2009. The share of jobs with a wage rise of 2 per cent or less has fallen from over 50 per cent in mid-2021 to less than 20 per cent.”

Looking ahead

Eurozone CPI final will be the main focus in European session while Italy trade balance will be featured too. US will release housing starts and building permits later in the day.

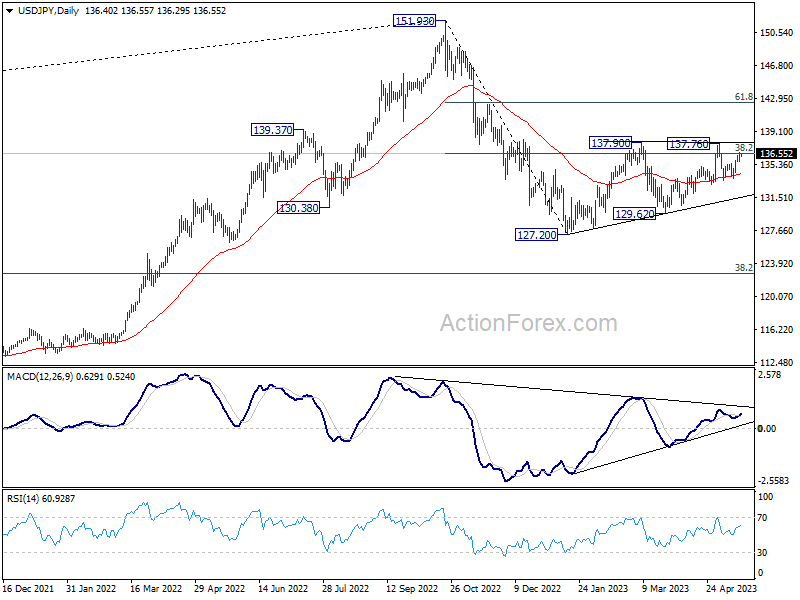

USD/JPY Daily Outlook

Daily Pivots: (S1) 135.82; (P) 136.26; (R1) 136.82More…

USD/JPY’s rally from 133.73 is still in progress and intraday bias remains on the upside for 137.76/90 resistance zone. Decisive break there will resume whole rebound from 127.20. On the downside, though, below 135.46 minor support will turn bias back to the downside for 133.73. Firm break there will resume the fall from 137.76 through 133.00.

In the bigger picture, price actions from 151.93 high are currently seen as a corrective pattern to the long term up trend. The first leg should have completed at 127.20. Rebound from there is seen as the second leg. Sustained break of 38.2% retracement of 151.93 to 127.20 at 136.34 will bring stronger rise to 61.8% retracement at 142.48. Meanwhile, break of 129.62 will argue that the third leg is starting through 127.20 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Annualized Q1 P | 0.40% | 0.20% | 0.10% | |

| 23:50 | JPY | GDP Deflator Y/Y Q1 P | 2.00% | 2.00% | 1.20% | |

| 01:30 | AUD | Wage Price Index Q/Q Q1 | 0.80% | 0.90% | 0.80% | |

| 04:30 | JPY | Industrial Production M/M Mar F | 1.10% | 0.80% | 0.80% | |

| 08:00 | EUR | Italy Trade Balance (EUR) Mar | 2.50B | 2.11B | ||

| 09:00 | EUR | Eurozone CPI Y/Y Apr F | 7.00% | 7.00% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Apr F | 5.60% | 5.60% | ||

| 12:30 | USD | Housing Starts Apr | 1.40M | 1.42M | ||

| 12:30 | USD | Building Permits Apr | 1.44M | 1.43M | ||

| 14:30 | USD | Crude Oil Inventories | -1.5M | 3.0M |