As the market holds its breath for today’s BoE rate decision and economic projections, Sterling is trading on a softer note, barring against Euro. Overnight attempts to resume the recent rally against Dollar were short-lived, with the Pound returning swiftly to its familiar range. The potential for hawkish and dovish surprises, or simultaneously both, at today’s meeting promises a volatile session for the British currency.

Elsewhere in the currency markets, Australian and New Zealand Dollars, along with Japanese Yen, stand as the week’s strongest performers. Risk sentiment is playing a minor role as stock markets continue to show lackluster performance. However, weakness in US and European yields seems to be providing some support for these currencies. Euro emerges as the current underperformer, followed by Canadian Dollar and US Dollar.

From a technical perspective, EUR/GBP appears to be losing some of its downside momentum, as reflected in 4H MACD. Yet, as long as 0.8745 resistance level holds, further decline is anticipated. Next target is 100% projection of 0.8977 to 0.8717 from 0.8874 at 0.8614. Decisive break of this level could trigger further downside acceleration. Conversely, in case of recovery, failure to regain 0.8745 could limit Euro’s strength elsewhere.

In Asia, at the time of writing, Nikkei is down -0.02%. Hong Kong HSI is down -0.34%. China Shanghai SSE is down -0.20%. Singapore Strait Times is down -0.41%. Overnight, DOW dropped -0.09%. S&P 500 rose 0.45%. NASDAQ rose 1.04%. 10-year yield dropped -0.082 to 3.439.

SNB Jordan signals readiness for further policy tightening amid inflation concerns

SNB Chairman, Thomas Jordan indicated yesterday that there might be a need to further tighten the monetary policy in Switzerland, signaling the bank’s unwavering commitment to keeping inflation in check.

“Monetary policy is still not restrictive enough to anchor inflation in the area of price stability,” Jordan said. “We cannot exclude that we have to further tighten monetary policy.”

Jordan pointedly noted, “If the inflation forecast is significantly above the area of price stability, then monetary policy is too loose.” This remark underscores the central bank’s resolve to use monetary policy levers to ensure that inflation doesn’t exceed the stability range.

The chairman’s comments come on the heels of recent data showing that annual inflation in Switzerland edged down to 2.6% in April from 2.9% in March. While these figures are modest compared to many countries grappling with double-digit inflation rates, they still exceed SNB’s traditional definition of price stability.

BoJ opinions: Current monetary easing should continue

In the Summary of Opinions at BoJ’s monetary policy meeting on April 27/28, new governor Kazuo Ueda’s debut, revealed the need to continue with current monetary easing despite improved view on inflation outlook.

One member said “attention is warranted for the time being on the possibility of continued high inflation” while another said “achievement of the price stability target of 2 percent is coming into sight”. Meanwhile, “price projections have been raised somewhat”.

Yet, it’s generally agreed that the central bank “should continue with the current monetary easing,” given that inflation is likely to decline ahead, in the background of heightened uncertainties in overseas economies.

Also it’s reiterated that to achieve the inflation target in “sustainable manner”, it needs to be “accompanied by wage increases”. And it’s “necessary” to continue to “firmly support the momentum for wage hikes through monetary easing “.

There was also cautions that “the risk of missing a chance to achieve the 2 percent target due to a hasty revision to monetary easing is much more significant than the risk of the inflation rate continuing to exceed 2 percent.”

One member noted that there is no need to revise the conduct of yield curve control as “distortions on the yield curve are currently dissipating”.

China’s CPI at 0.1% yoy in Apr, lowest since Feb 2021

China CPI slowed from 0.7% yoy to 0.1% yoy in April, below expectation of 0.3% yoy. That’s the lowest level since February 2021. Core CPI, excluding food and energy, was unchanged a 0.7% yoy.

Within the CPI, food prices in China rose by 0.4 per cent from a year earlier in April, compared with a rise of 2.4 per cent in March, while non-food prices rose by 0.1 per cent last month, year on year, down from an increase of 0.3 per cent in March.

“In April, the market supply was generally adequate, and consumer demand gradually recovered, with the CPI falling by 0.1 per cent from a month earlier and rising by 0.1 per cent, year on year,” said senior NBS statistician Dong Lijuan.”Core CPI, excluding food and energy prices, rose by 0.1 per cent from a month earlier to 0.7 per cent, year on year, up at the same rate as in the previous month.”

PPI dropped from -2.5% yoy to -3.6% yoy, below expectation of -3.2% yoy. PPI fell at the fastest rate since May 2020 and was down for a seventh consecutive month

“In April, PPI fell by 0.5 per cent from a month earlier and by 3.6 per cent, year on year, due to fluctuations in international commodity prices; the overall weakness of the domestic and international market demand; and the higher base of comparison from the same period last year,” Dong added.

BoE to hike 25bps, will there be hint on pause?

Today marks BoE’s much-anticipated “Super Thursday,” with markets bracing for a 25 bps increase that brings interest rate to 4.50%. While some speculate that BoE may hit the pause button post today’s rate hike, opinions are far from unanimous. Notably, Goldman Sachs anticipates interest rate to reach a terminal rate of 5.00% by August, implying two more rate hikes in the pipeline.

Attention will be focused on voting too. Known doves Silvana Tenreyro and Swati Dhingra are anticipated to vote against any change. However, given that inflation remained in double digits at 10.1% in March, any dissent from the remaining seven MPC members could be viewed as a dovish surprise. Conversely, hawkish surprises could arise if any members vote for a more aggressive 50bps hike today.

Further intrigue lies in the new economic projections, which will be closely examined for hints of the future rate path. Outlook for inflation remains shrouded in uncertainty. A report released today by NIESR suggests that inflation will remain “persistently elevated,” decreasing only to 5.4% by the end of 2023. This forecast markedly exceeds prediction by the Office for Budget Responsibility, which anticipated inflation to drop to 2.9%.

Here are some previews on BoE:

Elsewhere

US PPI and jobless claims will also be featured today.

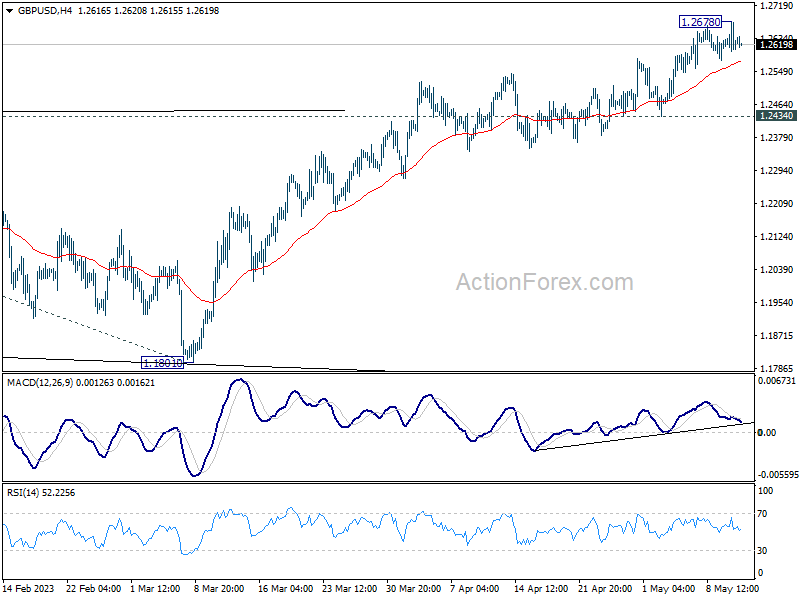

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2592; (P) 1.2636; (R1) 1.2669; More…

GBP/USD retreated quickly after rising to 1.2678 and intraday bias is turned neutral again. for now, further rally is expected as long as 1.2434 support holds. Break of 1.2678 will resume larger up trend to 1.2759 fibonacci level first. Firm break there will target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. However, decisive break of 1.2434 will confirm short term topping, and turn bias back to the downside for deeper fall.

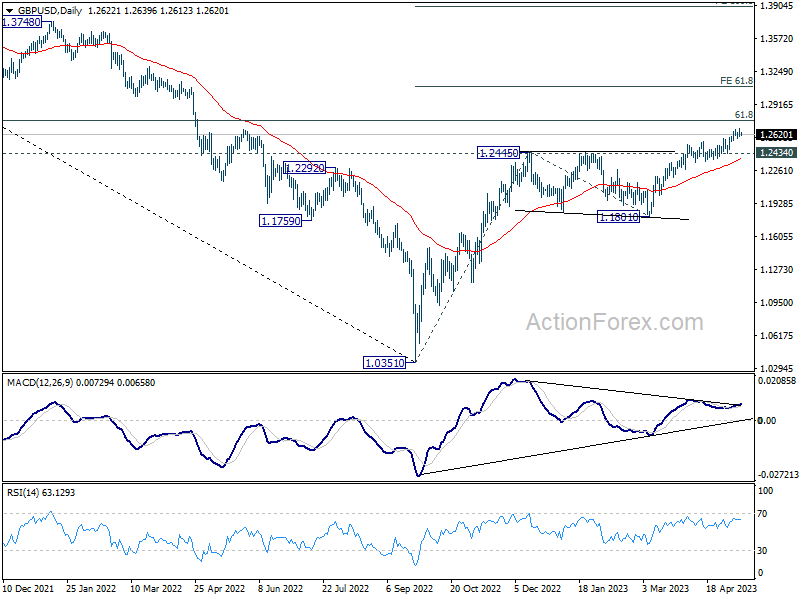

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS Housing Price Balance Apr | -39% | -38% | -43% | |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 23:50 | JPY | Bank Lending Y/Y Apr | 3.20% | 2.90% | 3.00% | |

| 23:50 | JPY | Current Account (JPY) Mar | 1.01T | 1.32T | 1.09T | 1.23T |

| 01:00 | AUD | Consumer Inflation Expectations May | 5.00% | 4.60% | ||

| 01:30 | CNY | CPI Y/Y Apr | 0.10% | 0.30% | 0.70% | |

| 01:30 | CNY | PPI Y/Y Apr | -3.60% | -3.20% | -2.50% | |

| 05:00 | JPY | Eco Watchers Survey: Current Apr | 54.6 | 54.1 | 53.3 | |

| 11:00 | GBP | BoE Interest Rate Decision | 4.50% | 4.25% | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | 7–0–2 | 7–0–2 | ||

| 12:30 | USD | PPI M/M Apr | 0.30% | -0.50% | ||

| 12:30 | USD | PPI Y/Y Apr | 1.40% | 2.70% | ||

| 12:30 | USD | PPI Core M/M Apr | 0.30% | -0.10% | ||

| 12:30 | USD | PPI Core Y/Y Apr | 2.70% | 3.40% | ||

| 12:30 | USD | Initial Jobless Claims (May 5) | 245K | 242K | ||

| 14:30 | USD | Natural Gas Storage | 78B | 54B |