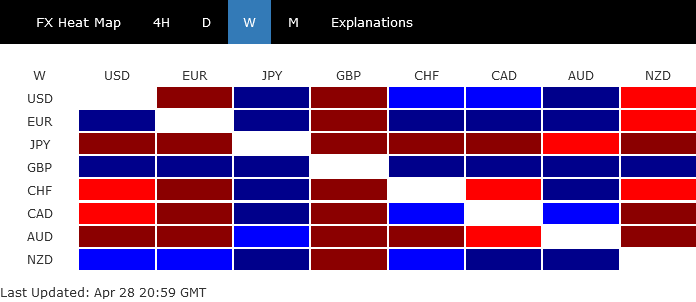

The markets experienced surprisingly high volatility in the last week of April, with central bank expectations as the primary driver. Japanese Yen emerged as the worst performer following BoJ’s dovish stance, leading bond traders to abandon hopes for any changes to yield curve control. Australian Dollar was the second-worst performer, as economists now lean towards another RBA hold at the next meeting. Swiss Franc and Canadian Dollar also closed lower. On the other hand, British Pound was the strongest performer, followed by the New Zealand Dollar. US Dollar and Euro were mixed, leaning more towards the firmer side.

Trading activity is expected to remain high this week, with Fed, ECB, and RBA rate decisions featuring prominently, along with several important economic data releases in the first week of May. Technically, stocks in the US and Europe appear set for an extended rally in the near term. Pound, and to a lesser the Euro, will likely maintain an advantage against commodity currencies. Meanwhile, last week’s Yen selloff could be just the beginning of a significant downward move.

Kazuo Ueda’s Inaugural BoJ Meeting Exceeds Dovish Expectations, Yen Bears and Stock Investors Rejoice

Kazuo Ueda’s first meeting as BoJ Governor proved more dovish than anticipated, delighting stock investors and Yen bears. Yield curve control parameters remained unaltered, and new economic projections indicated that the CPI core will decline again after reaching 2% target in 2024.

Forward guidance was modified, removing the statement, “it also expects short- and long-term policy interest rates to remain at their present or lower levels.” However, the pledge to “not hesitate to take additional easing measures if necessary” was retained.

BoJ will carry out a “broad-perspective review of monetary policy” over the next 12 to 18 months, disappointing those who anticipated immediate changes as early as at last week’s meeting.

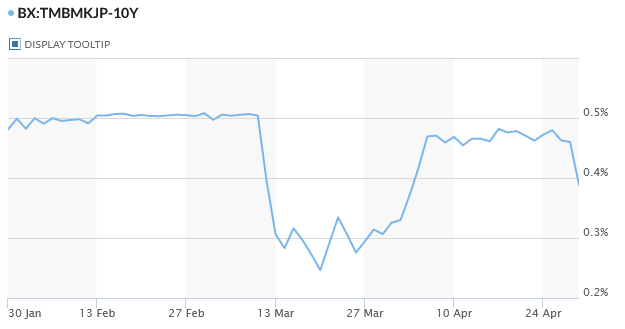

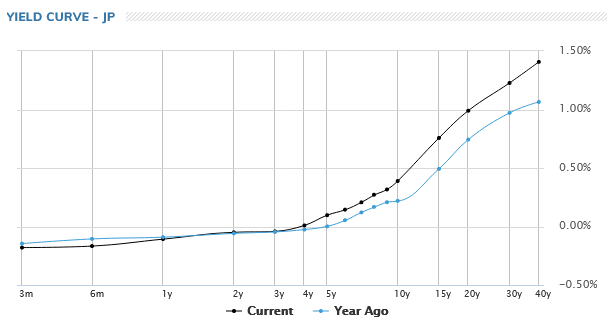

10-year JGB closed significantly lower at 0.389%, as traders abandoned hopes of a change in the 0.50% cap in the near future. Yield curve appears smooth, without any dips around the 10-year range.

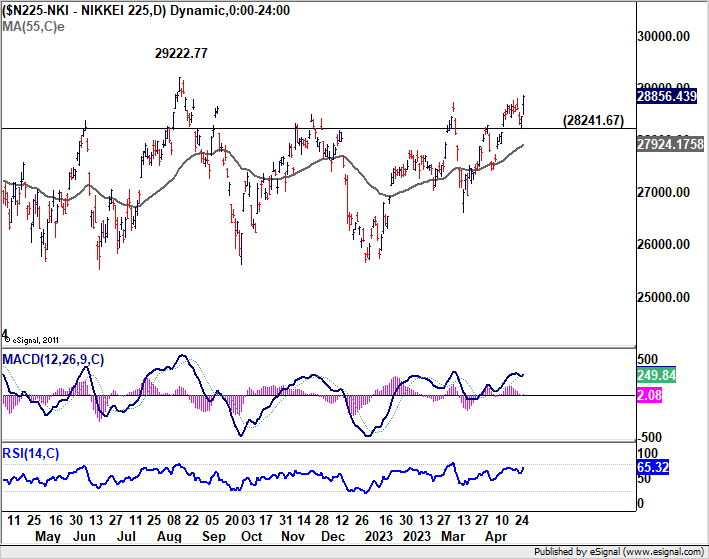

Nikkei made notable progress in resuming its near-term rally, closing at 28856.43. Outlook will remain bullish as long as 28241.67 support holds. Key near-term resistance of 29,222.77 should be tested soon. Firm break there will pave the way back to 30795.77 high and increase the likelihood of larger uptrend resumption.

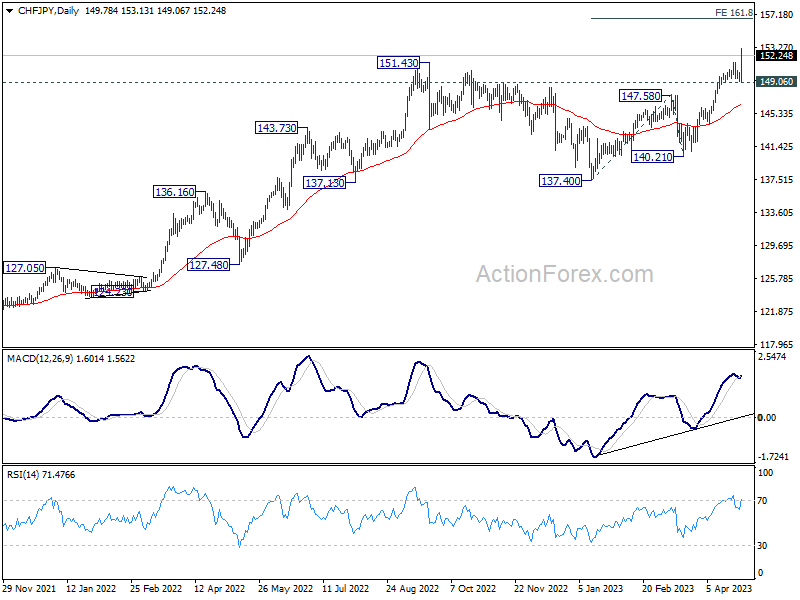

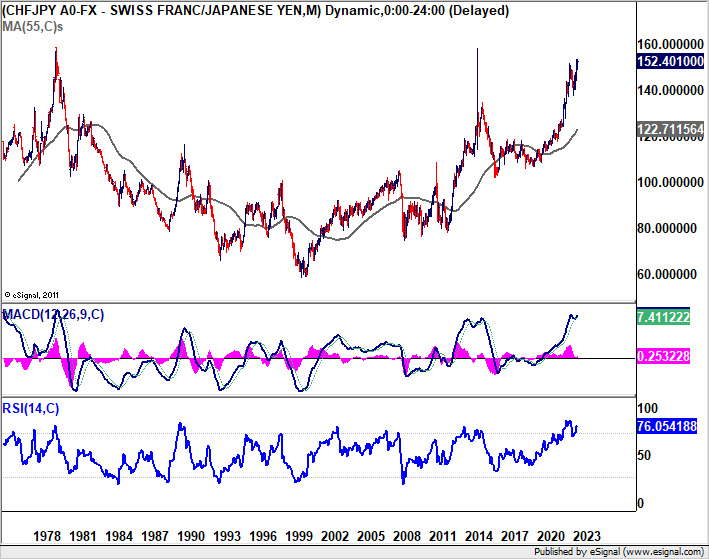

Following post-BoJ selloff, Yen finished as the week’s worst performer. CHF/JPY has finally surpassed 151.43 resistance to resume its long-term uptrend. Near-term outlook will remain bullish as long as 149.06 support holds. Next target the 161.8% projection of 137.40 to 147.58 from 140.21 at 156.68. There is now a realistic chance of breaking the 158.45 (made in 1979/80) to reach a new all-time high.

Aussie Struggles as RBA Pause Expectations Grow; GBP/AUD on the Move

Australian Dollar was the second worst performer last week, on growing expectation that RBA would pause for the second time at the upcoming meeting on May 2, Tuesday. The shift in expectation came after release of Q1 CPI report, which showed a lower path of headline inflation as RBA projected, and a path for trimmed mean CPI inline with the forecast. Thus, RBA would now have more room to continue to wait and assess the impact of prior hikes. Indeed, the current 3.60% cash rate target is now seen by some as the terminal one for the current cycle.

Additionally, commodity prices also weighed on the Aussie, with Copper falling to new 2023 low last week. Iron ore prices also had the worst month since October, on concern of weaker-than-expected peak construction season in China.

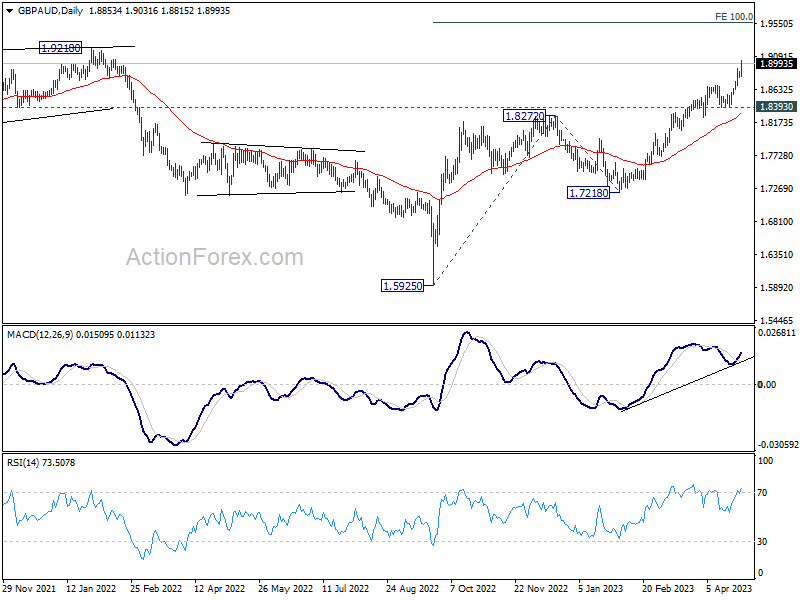

GBP/AUD was one the the top movers last week, gaining more than 2.1%. Near term outlook will now stay bullish as long as 1.8393 support holds. Current rally from 1.5925 should extend through 1.9218 resistance to 100% projection of 1.5925 to 1.8272 from 1.7218 at 1.9565.

It’s still too early to conclude for now. But current development raises the chance that long term consolidation pattern from 2.2382 (2015 high) has completed with three waves to 1.5925). Rise from 1.4378 (2013 low) might be ready to resume. A key hurdle to overcome is the resistance zone between trend line resistance (now at around 1.9923 level), and 2.0840. This is the level to watch in the second half of the year.

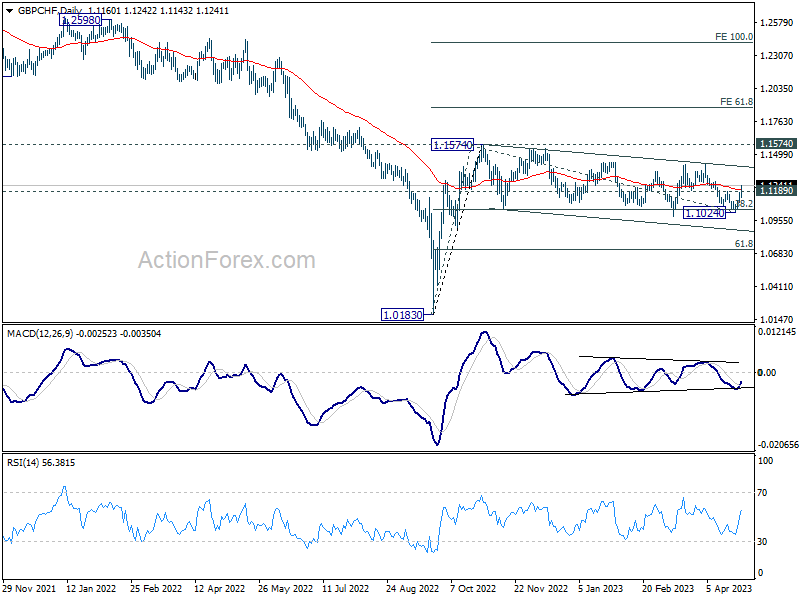

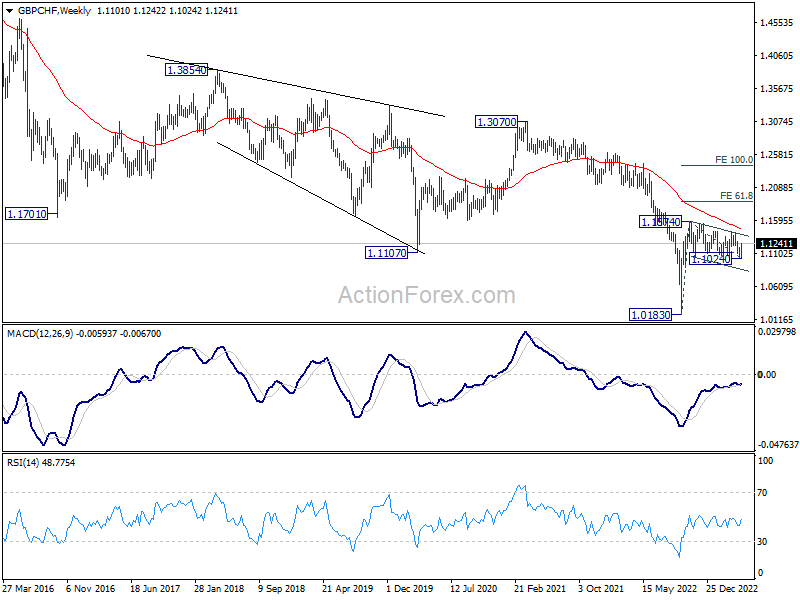

Sterling Outperforms on Rate Expectations; GBP/CHF in Focus

Taking about Sterling, it emerged as the best performer of the week, closing even above March highs against all but Euro and Swiss Franc. Interest rate expectations are driving Pound’s gains as UK remains the only major economy grappling with stubbornly high double-digit inflation. Without clear signs of increasing disinflation momentum, BoE will have little choice but to continue tightening.

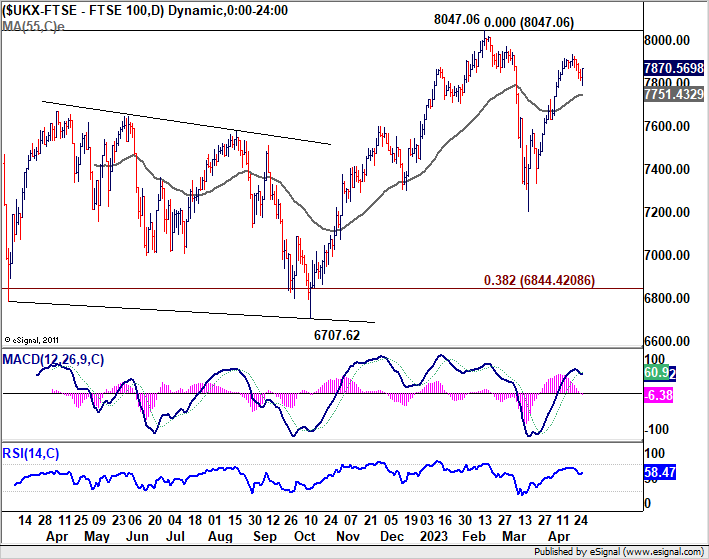

Meanwhile, the overall economy appears to have weathered inflation pressures, led by robust growth in the services sector. As reflected in FTSE developments, investors do not seem too nervous at the moment. The near-term pullback may have completed well ahead of 55 Day EMA, and another rise to retest the record high of 8047.06 could occur within the quarter.

Developments in GBP/CHF leading up to BoE meeting on May 11 and its aftermath are worth watching. Price actions from 1.1574 (2022 high) are clearly corrective in nature. 38.2% retracement of 1.0183 to 1.1574 at 1.1043 was defended well despite breakthrough attempts. A short-term bottom may have formed at 1.1024 with last week’s rebound, and further rise back to 1.1412 resistance is now favored.

It may also be time for an upside breakout. Break of 1.1024 would be the first sign a resumption of the rally from 1.0183 (2022 spike low). Further break of 1.1574 would also decisively surpass 55 W EMA (now at 1.1469). Subsequent medium-term rise should then be seen to 61.8% projection of 1.0183 to 1.1574 from 1.1024 at 1.1884.

We’ll see if BoE provides the needed push for GBP/CHF later in the month.

Fed Likely to Continue Tightening but May Pause After Next Hike

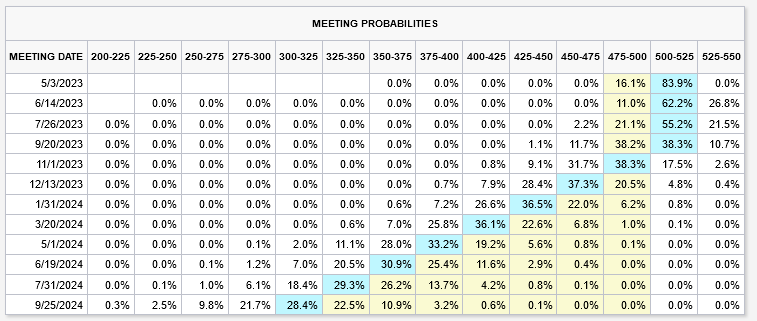

Turning over to the US, with core PCE price index remaining high at 4.6% yoy in March, Fed is expected to maintain its tightening stance by implementing another 25 bps hike on May 3rd, the coming Wednesday. However, as headline PCE slowed more quickly than expected to 4.2%, Fed should have more confidence in pausing the cycle after this hike. This expectation is further supported by weaker-than-anticipated Q1 GDP growth, registering a modest 1.1% annualized rate.

Fed fund futures are now pricing in 83.9% probability of a 25 bps hike to 5.00-5.25% on Wednesday, with a near 50% chance that the rate will remain unchanged after September, and a 79.9% chance of a cut in November. The pricings are now more “rational”. Naturally, future developments will influence these projections, including Fed’s new economic projections to be published in June.

US stocks rebounded significantly late in the week, with DOW closing on a strong note at 34098.16, above the near-term resistance at 34082.94. The strong support from the 55 D EMA also affirms near-term bullishness. Further rallies are anticipated to 34712.28 resistance and beyond. A key hurdle will be 61.8% projection of 28660.94 to 34712.28 from 31429.82 at 35169.54, which could be tested later in the quarter.

Dollar Index remained within tight range last week, showing no significant progress. The favored view is that fall from 105.88 is the second leg of the corrective pattern from 100.82, completed at 100.78. Break of 102.80 resistance would support this view, and bring stronger rally back to 105.88 resistance as the third leg of the pattern. However, a decisive break below 100.82 would dampen this outlook, resuming the overall downtrend from 114.77.

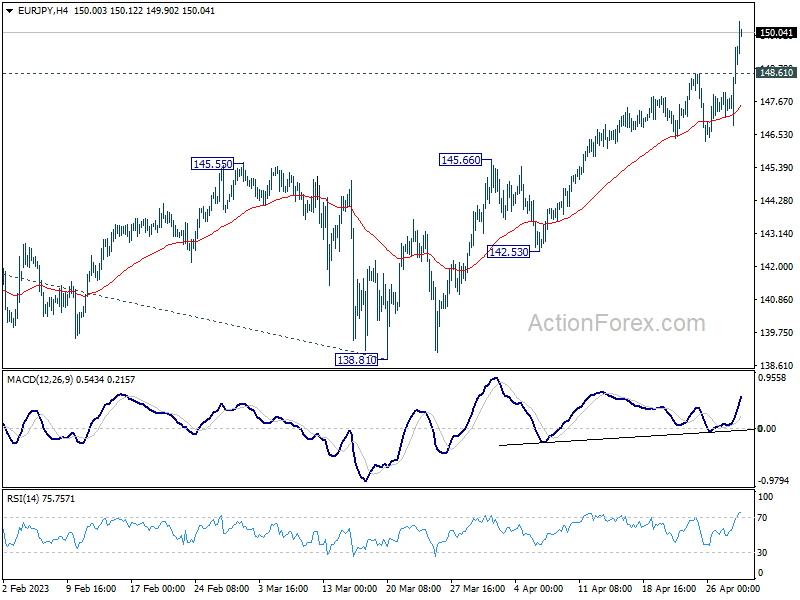

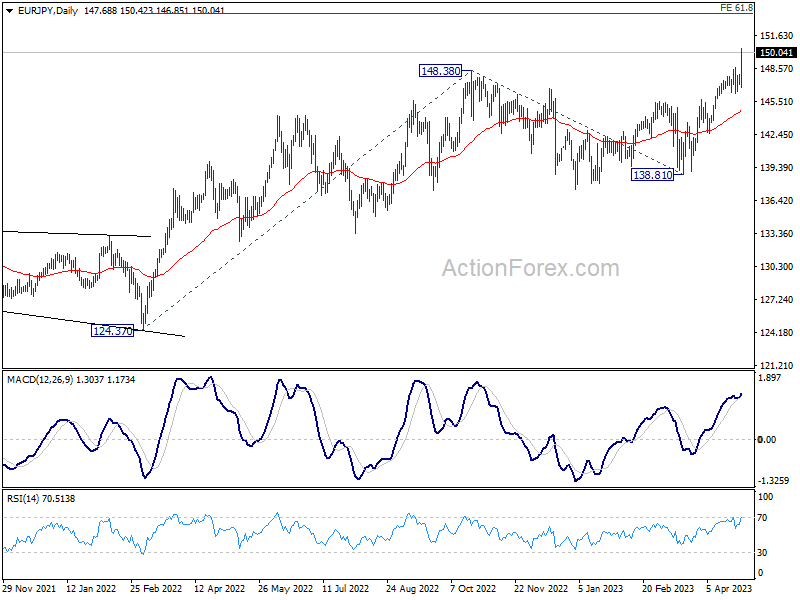

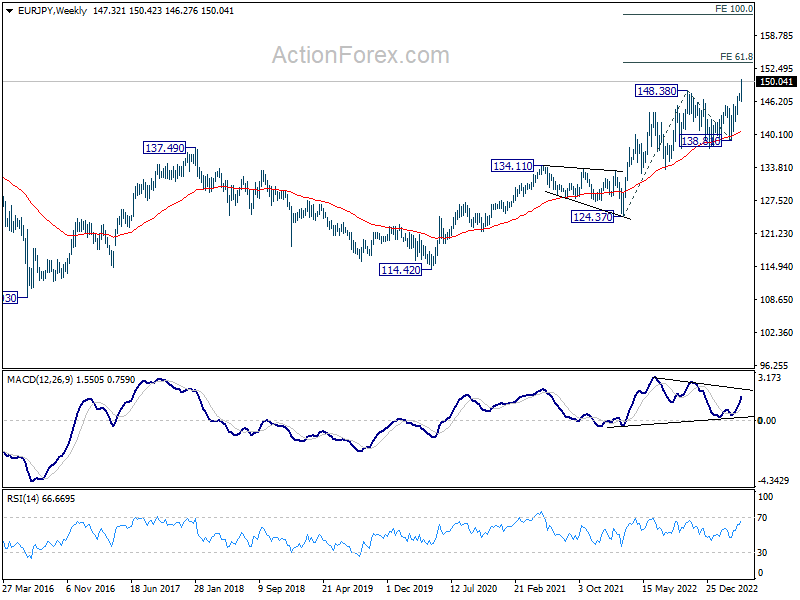

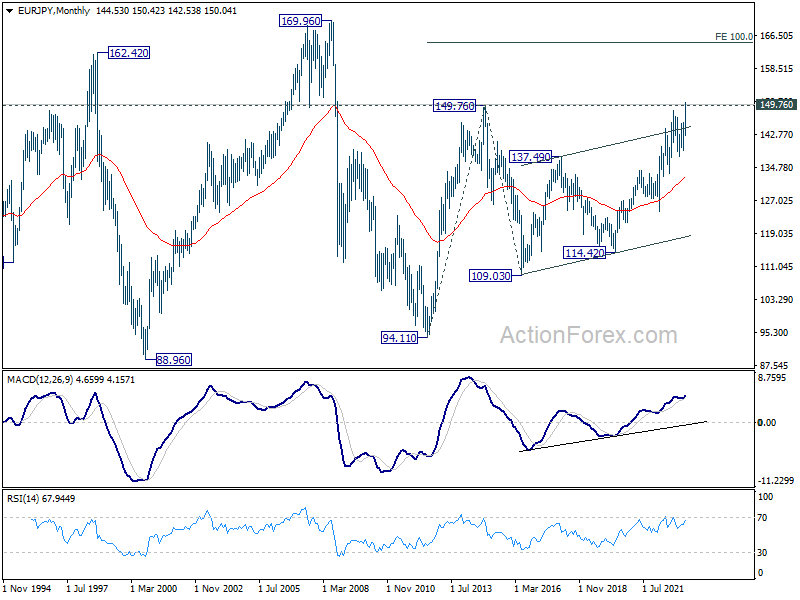

EUR/JPY Weekly Outlook

EUR/JPY’s up trend continued last week, surged through 148.38, and closed above 149.76 long term resistance. Initial bias stays on the upside this week. Next target is 153.64 projection level. On the downside, below 148.61 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, current development indicates that rise from 114.42 (2020 low) is in progress. Next target is 61.8% projection of 124.37 to 148.38 from 138.81 at 153.64. Sustained break there will pave the way to 100% projection at 162.82. For now, medium term outlook will remain bullish as long as 138.81 support holds, even in case of deep pull back.

In the long term picture, break of 149.76 (2014 high) argues that whole up trend form 94.11 (2012 low) is resuming. Sustained trading above 149.76 will pave the way to 100% projection of 94.11 to 149.76 from 109.03 at 164.68, which is close to 169.96 (2008 high).

This “NEW CONCEPT” Trading Strategy Prints Money!… (INSANE Results!)

This “NEW CONCEPT” Trading Strategy Prints Money!… (INSANE Results!)