Retail sales in the US were weaker than expectations but it was Fed’s Wallers comments which surprised the markets more. Waller said that recent data show Fed hasn’t made much progress on inflation , and followed that up with more hikes are needed. That was hikes…not another hike. So although the market has been tolerating the playbook that the Fed was to have one more hike, they were not thinking there would be multiple hikes left from the Fed.

Say it ain’t so.

Now Waller is typically more hawkish and perhaps he was sent out to take one for Chair Powell, and slow the S&P from heading to 4200. I am not sure the Fed wants to see stocks racing too far ahead as they try to ease the economic ship in for a soft landing. After all if the economy falls off the cliff as some see ahead, the implications for stocks could get uglier from loftier levels. Moreover, the debt market is also at odds with Feds thinking with 2 year yield trading above and below 4% today when the Fed is targeting 5.25% or more (according to Waller) and intent on not looking to ease until 2024 at the earliest. The disconnect is evident in the January Fed funds contract as well which is pricing in a fed funds rate of 4.47% (it was at 4.36% earlier in the day). Again the Fed is looking for a minimum of a high range for the Fed target at 5.0% -5.25%.

Waller at least slowed the stock and bond ships down a bit.

Later the Univ. of Michigan consumer sentiment (preliminary) came out and although sentiment remained high at 63.5 vs 62.0 last month, it was the inflation reading that caught most of the markets attention. That measure saw the 1 year inflation expectations rising sharply to 4.6% from 3.6%.

So in addition to Waller, the consumer is not buying the “happy days are just ahead” for inflation. Having said that, this week the CPI and the PPI data were encouraging and the math of the next few months at least, imply that with a little luck – and some cooperation from shelter costs – a big chunk from the CPI headline at 5%, can be further eroded from headline and core inflation readings (see post here). The not so great part of that idea, is gas and oil prices are on the rise again and that can raise costs across many sectors of the economy (not just at the gas pump).

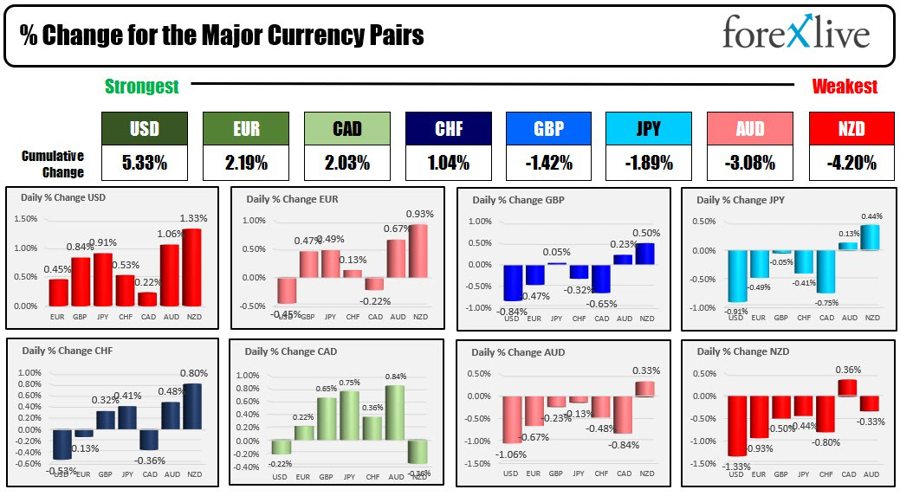

The implications of the news today in the currency market, was the USD was king and is ending the day as the strongest of the major currencies (see ranking below). The NZD was the weakest followed by the AUD as risk-off sent those currencies lower vs most currencies (the USD was up 1% vs both those currencies).

The strongest to the weakest of the major currencies

Although the USD was higher across all the major currencies today, it is ending the trading week mixed vs the major currencies. The USD was weaker vs the following currencies

- EUR, -0.86%

- CHF, -1.26%

- CAD, -1.17%

- AUD, -0.71%

The USD was stronger or unchanged vs the following:

- JPY, +1.21%

- GBP, unchanged

- NZD, +0.68%

The US stocks today are ending the day down despite a good start to the earnings season from some banks. JPMorgan shares rose 7.55%, CItibank rose 4.78% PNC rose 0.36%, but Wells Fargo fell -0.05% after largely better than expected earnings.

For the major indices, although they closed off lows, they still ended the day lower:.

- Dow fell -0.42%

- S&P fell -0.21%

- Nasdaq fell -0.35%

For the trading week, all three indices did close with gains:

- Dow Industrial Average average rose 1.20%

- S&P index rose 0.79%

- NASDAQ index rose was the laggard with a modest gain of 0.29%

In the US at that market, yields reacted to the upside on the data/news with the two year yield back above the 4% level at 4.103%. A snapshot of levels at the end of the week shows:

- 2 year yield 4.103%, up 13.1 basis points

- 5 year yield 3.61% up 10.5 basis points

- 10 year yield 3.517% up 6.8 basis points

- 30 year yield 3.738% +4.9 basis points

For the trading week:

- 2 year yield rose 11 basis points

- 5 year yield rose 9.3 basis points

- 10 year yield rose 10.4 basis points

- 30 year yield rose 11.5 basis points

The price of gold/silver fell sharply today reacting to higher yields and stronger dollar:

- Spot gold fell $36.84 or -1.81% to $2003.43. For the trading week, gold prices fell $-3.62 or -0.18%

- Spot silver fell $-0.50 or -1.94% to $25.31. For the trading week the price still rose by $0.36 or 1.43%

- Crude oil rose $0.36 to $82.52 today. The high for the week reached $83.53. That is precisely where the 200 day moving average is currently located. Next week the 200 day moving average will be a key barometer for both buyers and sellers – move above is more bullish. Stay below is more bearish. The low for the week reached the $79.37 this week. Overall, crude oil is ending the week up $1.82 or 2.26%.

Next week, CPI data from Canada, Japan, New Zealand, UK will all be released. The Reserve Bank of Australia meeting minutes (they kept rates unchanged) will be released. The ECB will also release meeting minutes (raised by by 50 bps to 3.5%).

In the US, the Philly Fed and the Empire manufacturing indices will be released along with existing home sales and flash manufacturing/services PMI data.

On the earnings calendar, big names are still a week or two away from release. More financial institutions will dominate the calendar in the upcoming week:

Monday April 17

- State Street Bank

Tuesday, April 18

- Goldman Sachs

- BNY Mellon

- Bank of America

Wednesday, April 19

- Morgan Stanley

- bancorp

- Zions Bancorporation

- Citizens

Thursday, April 20

- Huntington

- Comerica

- KeyBank

- Truist

Starting the week of April 24, the earning shifts into high gear (subject to change) Below is a preview of what’s to come. Traders will be watching the projections going forward. If earnings estimates start coming down, the S&P and major indices could be in trouble:

Monday, April 24

- Coca-Cola

- Kimberly-Clark

Tuesday, April 25

- Alphabet

- PepsiCo

- Verizon

- UPS

- Raytheon

- Lockheed Martin

- GE

- 3M

- GM

- Chipotle

- Dow

- Snap

- Whirlpool

Wednesday, April 26

- Meta Platforms

- Visa

- AT&T

- Qualcomm

- Boeing

- ServiceNow

- General Dynamics

- Hilton Worldwide

Thursday, April 27

- Apple

- Microsoft

- Amazon

- Merck

- Bristol-Myers Squibb

- Intel

- Caterpillar

Thanks for your support. Have a great and safe weekend to all.