Financial markets in today’s Asian session exhibit a risk-averse sentiment, despite attempts on the weekend to stabilize the situation from the recent banking crisis. While UBS’s acquisition of Credit Suisse may have provided slight support to Euro and Swiss Franc, stocks are trading in red, and commodity currencies are weaker. Yen, on the other hand, is showing strength, reflecting overall caution in the markets. However, most major currency pairs and crosses remain within Friday’s range, exhibiting low volatility.

Central bank decisions this week will be in the spotlight, particularly FOMC rate decision. Current expectations lean towards a 25bps hike, but this could change based on new developments. Fed’s future trajectory is uncertain, and investors are looking for clarity from the latest economic projections and dot plots. In addition, BoE is anticipated to implement a 25bps rate hike before pausing, and SNB is likely to increase rates by 50bps due to resurgence of inflation.

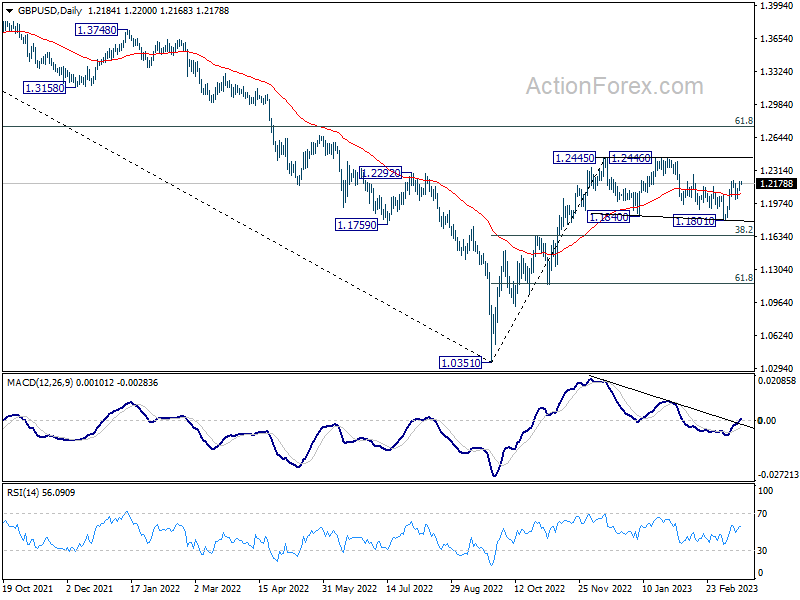

GBP/USD will be a focus this week with Fed and BoE rate decisions featured. Technically, current outlook is that consolidation pattern from 1.2445 has completed with three waves down to 1.1801. Break of last week high at 1.2203 will bring retest of 1.2445/6 resistance zone. Decisive break there will resume larger up trend from 1.0351. Let’s see how it goes.

In Asia, Nikkei closed down -1.42%. Hong Kong HSI is down -3.17%. China Shanghai SSE is down -0.46%. Singapore Strait Times is down -1.22%. Japan 10-year JGB yield is down -0.035 at 0.238.

Market sentiment remains fragile despite CS takeover and coordinated central bank actions

Over the weekend, two significant actions were announced in an attempt to stabilize the markets amidst the ongoing banking crisis. These actions included the government-supported takeover of troubled Credit Suisse by UBS and a coordinated move by six major central banks to enhance the provision of US dollar liquidity. Despite these measures, market sentiment remains fragile, with stocks in Japan, Hong Kong, and Singapore extending declines.

UBS’s takeover of Credit Suisse was made possible with the support of the Swiss federal government, FINMA, and SNB. SNB noted that this move aims to secure financial stability and protect the Swiss economy during these exceptional circumstances. Based on the Federal Council’s Emergency Ordinance, Credit Suisse and UBS can obtain a liquidity assistance loan with privileged creditor status in bankruptcy for a total amount of up to CHF 100B. Additionally, SNB can grant Credit Suisse a liquidity assistance loan of up to CHF 100B backed by a federal default guarantee.

In a separate announcement, Fed, alongside BoC, BoE, BoJ, ECB, and SNB, revealed a coordinated action to increase the availability of liquidity via the standing US dollar liquidity swap line arrangements. To enhance the swap lines’ effectiveness, the central banks will increase the frequency of 7-day maturity operations from weekly to daily, starting on March 20, 2023, and continuing at least until the end of April.

These swap lines between central banks serve as crucial liquidity backstops to ease strains in global funding markets. By mitigating these strains, central banks aim to maintain the supply of credit to households and businesses. However, the ongoing decline in stock markets across Asia signals that further actions may be needed to restore confidence and stability in the global financial markets.

Hong Kong HSI is trading down -2.5% at the time of writing. The decline from 22700.85 (Jan high) is still in progress with the index bounded well inside the falling channel, and capped below 55 hour EMA. Outlook will stay bearish as long as 19804.56 support turned resistance holds. Next target is 100% projection of 22700.85 to 19804.56 from 21005.66 at 18109.37.

BoJ members support persistent monetary easing, discussed side effects

In the Summary of Opinions from BoJ’s March meeting, many members expressed support for continuing with the current monetary easing and yield curve control. However, there were also discussions on potential side effects and concerns related to the policy.

One member acknowledged the side effects of the current monetary easing, such as distortions in the yield curve. They stressed the need for BoJ to examine market functioning without preconceptions while assessing the balance between positive effects and side effects. Nonetheless, this member believed that the bank should “persistently continue with large-scale monetary easing” in the current phase.

Another member commented that it would take time to examine the effects of modifications in yield curve control on market functioning. They expect that when observed CPI inflation declines and market projections of interest rates calm down, “distortions on the yield curve are expected to be corrected”.

A member warned against hasty policy changes, stating that the risk of missing the chance to achieve the price stability target should be considered more significant than the risk of delaying policy changes, given the current improvements in the price environment.

Another member emphasized the importance of BoJ maintaining its commitment to the 2% price stability target. They argued that starting a discussion on the target could lead to “unnecessary speculation” on monetary policy conduct, despite the growing possibility of achieving the target. Similarly, this member saw no need to revise the joint statement of the government and BoJ.

Fed, SNB and BoE Decisions Loom: Uncertainty Remains Over Rate Hike Paths and Market Impacts”

This week, the highly anticipated FOMC rate decision will finally take place. Market expectations have been on a roller-coaster ride, shifting from a 50bps hike following Fed Chair Jerome Powell’s semi-annual testimony to a potential hold during the peak of last week’s banking crisis. As of Friday’s close, fed fund futures were pricing in a 62% chance of a 25bps hike to 4.75-5.00%. However, these odds may change based on upcoming developments.

More uncertainty lies in Fed’s path beyond March, with markets pricing in an 80% chance of both a pause in May and a cut in June. There’s also a 65% probability that rates will fall back to 3.75-4.00% by the end of the year. The new economic projections and dot plots from the Fed should help clarify some of these uncertainties.

Meanwhile, BoE is expected to hike by a final 25bps to 4.25% and then pause. Some economists predict that rates could remain at that level for at least a year. However, with market pricing suggesting a 25bps hike is far from certain, BoE could surprise investors. Voting patterns during the meeting will also be closely monitored.

SNB is widely anticipated to hike by 50bps to 1.50% after February’s CPI re-acceleration to 3.4%. Chair Thomas Jordan has stated that monetary policy is still too loose and further tightening cannot be ruled out.

Other central bank activities include the BoJ Summary of Opinions from its February meeting, RBA minutes from its March meeting, and BoC meeting minutes release.

In terms of data, CPI reports from Canada, the UK, and Japan will be significant, while PMIs from Australia, Japan, Eurozone, UK, and US will be closely watched.

Here are some highlights for the week:

- Monday: BoJ summary of opinions; Germany PPI; Eurozone trade balance.

- Tuesday: New Zealand trade balance; RBA minutes; Swiss trade balance; Germany ZEW; Canada CPI, US existing home sales.

- Wednesday: UK CPI, PPI; Eurozone current account; Canada new housing price index, BoC minutes; FOMC rate decision.

- Thursday: SNB rate decision; BoE rate decision; US jobless claims, current account, new home sales; Eurozone consumer confidence.

- Friday: Australia PMIs; Japan CPI, PMI manufacturing; UK Gfk consumer confidence, retail sales, PMIs; Eurozone PMIs; Canada retail sales; US durable goods orders, PMIs.

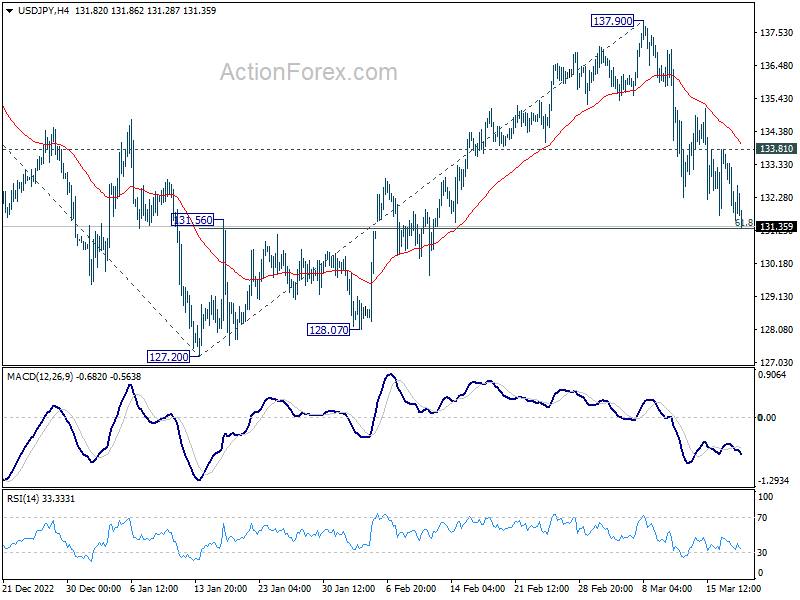

USD/JPY Daily Outlook

Daily Pivots: (S1) 131.04; (P) 132.41; (R1) 133.26; More…

USD/JPY’s fall from 137.90 is still in progress and it’s now touching 61.8% retracement of 127.20 to 137.90 at 131.28. Intraday bias remains on the downside for the moment. Sustained break of 131.28 will pave the way to retest 127.20 low next. On the upside, above 133.81 minor resistance will turn intraday bias neutral and bring some consolidations first.

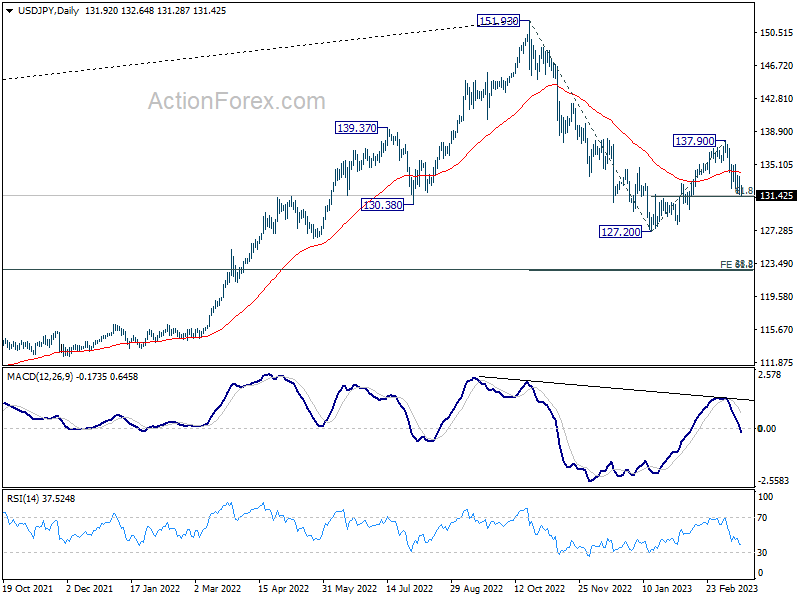

In the bigger picture, rebound from 127.20 should have completed at 137.90 as a corrective move, with strong break of 55 day EMA. The down trend from 151.93 (2022 high) is not over yet. Break of 127.20 will resume this down trend and target 61.8% projection of 151.93 to 127.20 from 137.90 at 122.61. This will now be the favored case as long as 137.90 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 00:01 | GBP | Rightmove House Price Index M/M Mar | 0.80% | 0.00% | ||

| 07:00 | EUR | Germany PPI M/M Feb | -1.20% | -1.00% | ||

| 07:00 | EUR | Germany PPI Y/Y Feb | 12.40% | 17.80% | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Jan | -17.3B | -18.1B | ||

| 11:00 | EUR | German Buba Monthly Report |