Despite regaining some ground in the Asian session, Euro continues to trade as the week’s weakest performer alongside Swiss Franc. Today’s ECB rate announcement is the primary focus for investors, as uncertainty looms over the extent of the anticipated rate hike. The SNB’s efforts to stabilize the markets in response to Credit Suisse’s problems may have temporarily curbed negative sentiment, but the potential trigger for a crisis remains unknown.

In its February statement, ECB unambiguously signaled its intention to increase rates by 50bps at today’s meeting, a message reiterated repeatedly by officials, including President Christine Lagarde. However, following recent market turmoil, investors are now pricing in only a 30% chance of the 50bps hike, with a more modest 25bps increase seeming increasingly plausible. In addition to the rate decision, market participants will be closely monitoring ECB’s updated economic projections, adding further complexity to the day’s proceedings.

Elsewhere in the currency markets, Yen has emerged as the week’s strongest performer so far, due to rally resumption yesterday. Surprisingly, commodity currencies such as Australian Dollar, New Zealand Dollar, and Canadian Dollar have also demonstrated resilience, albeit with limited gains. As these currencies are not at the epicenter of the market selloff, their performance has been relatively stable. Meanwhile, Dollar remains mixed as traders grapple with ongoing volatility in both treasury yields and stocks, leaving them hesitant to fully commit to a particular direction.

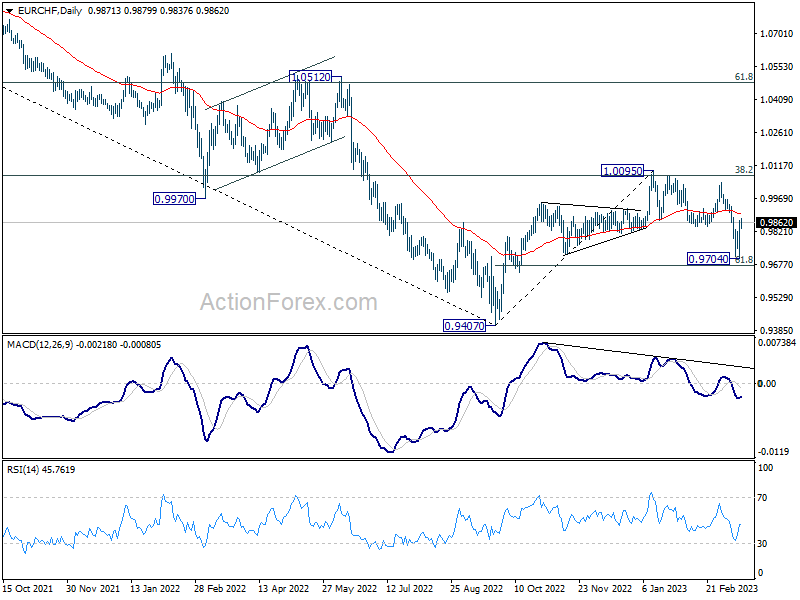

Technically, EUR/CHF has exhibited a robust rebound from 0.9704 (yesterday’s low), but that could be attributed more to Swiss Franc’s own problems. Despite this recovery, downside risk remains as long as it trades below 55 day EMA (now at 0.9901). The prevailing decline from 1.0095 peak is expected to persist, potentially extending towards the 61.8% retracement level of 0.9407 to 1.0095 at 0.9670. A further decline may even prompt a retest of the 0.9407 low. However, sustained break above the 55-day EMA would invalidate near-term bearishness and could trigger a more substantial rally towards the 1.0095 resistance level.

In Asia, at the time of writing, Nikkei is down -0.97%. Hong Kong HSI is down -1.25%. China Shanghai SSE is down -0.49%. Singapore Strait Times is down -0.78%. Japan 10-year JGB yield is down -0.0161 at 0.300. Overnight, DOW dropped -0.87%. S&P 500 dropped -0.70%. NASDAQ rose 0.05%. 10-year yield dropped -0.146 to 3.492, after hitting as low as 3.388.

Credit Suisse to borrow from SNB to calm markets

Credit Suisse’s measures to ease investor concerns over potential contagion and a banking crisis have failed to lift market pressures, with the Asian markets remaining under pressure.

The bank announced it would borrow up to CHF50B from the SNB, calling it a “decisive action to pre-emptively strengthen its liquidity.” The loan and a repurchase of billions of dollars of Credit Suisse debt aim to manage its liabilities and interest payment expenses.

Earlier, in a joint statement with the Swiss financial market regulator FINMA, the SNB assured the markets that the Credit Suisse had met “strict capital and liquidity requirements” and said, “there are no indications of a direct risk of contagion for Swiss institutions due to the current turmoil in the US banking market.”

“If necessary, the SNB will provide CS with liquidity,” FINMA and SNB said.

Japan posted record February trade deficit

In February, Japan exports rose 6.5% yoy to JPY 7655B, below expectation of 7.1% yoy. Imports rose 8.3% yoy to JPY 8552B, below expectation of 12.2% yoy. Consequently, the country experienced its largest February trade deficit to date at JPY -897.7B.

The breakdown of trade relations painted an interesting picture, with the US and China displaying contrasting trends. Exports to the US surged by 14.9% yoy, while imports increased by 6.6%, resulting in a favorable surplus of JPY 530.5B. However, trade with China proved more challenging, as exports dipped by -10.9% yoy and imports saw a marginal decrease of 0.6% yoy, culminating in a deficit of JPY -209.8B.

On a more positive note, seasonally adjusted figures highlighted a 4.4%mom rise in exports to JPY 8146B, accompanied by a 3.0% mom drop in imports to JPY 9336B. As a result, trade deficit narrowed to JPY -1191B, outperforming the expected JPY -1460B.

Australia employment grew 64.6k in Feb, unemployment rate dropped to 3.5%

Australia employment grew 64.6k in February, well above expectation of 48.5k. Full-time employment rose 74.9k. Part-time employment decreased -10.3k.

Unemployment rate dropped from 3.7% to 3.5%, below expectation of 3.6%. Participation rate rose 0.1% to 66.6%. Monthly hours worked rose 3.9% mom.

Bjorn Jarvis, ABS head of labour statistics said: “with employment increasing by around 65,000 people, and the number of unemployed decreasing by 17,000 people, the unemployment rate fell to 3.5 per cent. This was back to the level we saw in December.

“The February increase in employment follows consecutive falls in December and January. In January, this reflected a larger than usual number of people waiting to start a new job, the majority of whom returned to or commenced their jobs in February.

NZ GDP contracted -0.6% qoq in Q4, RBNZ may slow tightening

New Zealand’s Q4 GDP contracted by -0.6% qoq, missing the expected contraction of 0.2% qoq. The primary industries fell by 1.3%, service industries were down by 0.1%, and goods-producing industries were down by 0.3%.

Although the Finance Minister Grant Robertson acknowledged that the GDP could fluctuate as the country continues to recover from COVID, he also highlighted that the economy is nearly 6.7% larger than pre-pandemic levels, outpacing other countries.

Despite this, the GDP figure is significantly below RBNZ’s forecast of 0.7% growth, suggesting that the central bank may not need to be as aggressive with its tightening in the future. As a result, economists are now predicting that the RBNZ will opt for a more modest 25bps rate hike in April instead of the previously expected 50bps.

Looking ahead

The main event is ECB’s rate decision and press conference. Elsewhere, Swiss SECO will release economic forecasts. Canada will publish wholesale sales. US jobless claims, Philly Fed survey, housing starts and building permits, and import prices will be featured.

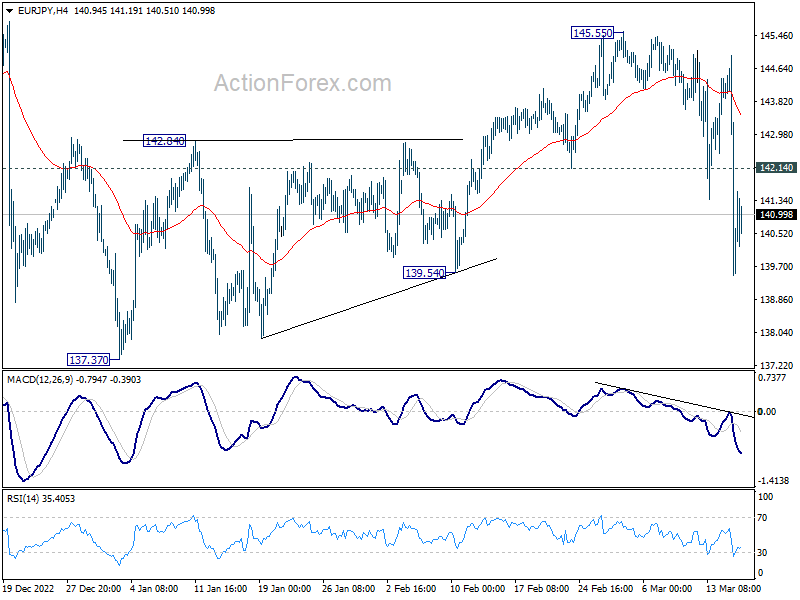

EUR/JPY Daily Outlook

Daily Pivots: (S1) 138.74; (P) 141.86; (R1) 144.23; More….

Intraday bias in EUR/JPY remains on the downside for the moment. Fall from 145.55 is seen as the third leg of the whole correction from 148.38 high. Deeper decline would be seen to for retesting 137.37 low, and then 135.40 fibonacci level. On the upside, above 142.14 minor resistance will turn intraday bias neutral first, and could bring recovery. But near term risk will remain on the downside as long as 4 hour 55 EMA (now at 143.47) holds.

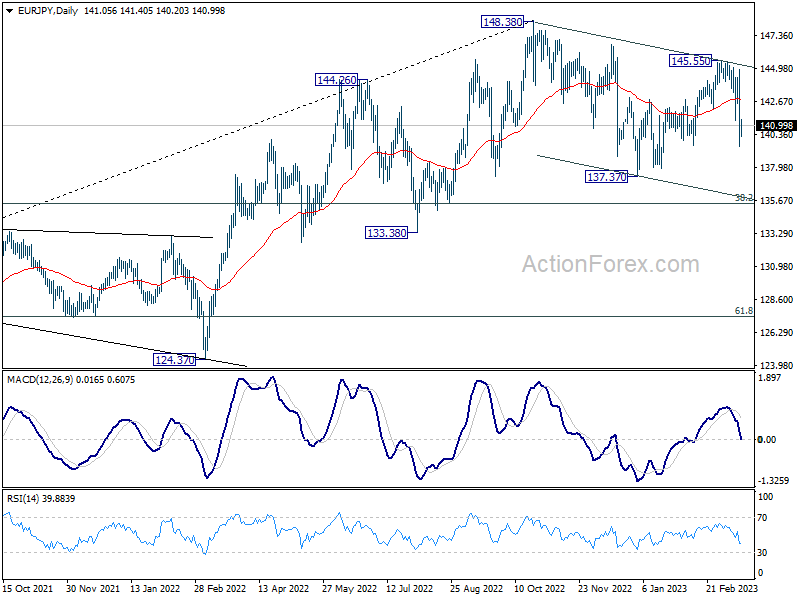

In the bigger picture, as long as 55 week EMA (now at 139.54) holds, larger up trend from 114.42 (2020 low) is still in progress for 149.76 long term resistance. However, firm break of 55 week EMA will bring deeper fall to 38.2% retracement of 114.42 to 148.38 at 135.40. Sustained break there will raise the chance of trend reversal, and target 61.8% retracement at 127.39.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | GDP Q/Q Q4 | -0.60% | -0.20% | 2.00% | 1.70% |

| 23:50 | JPY | Trade Balance (JPY) Feb | -1.19T | -1.46T | -1.82T | |

| 23:50 | JPY | Machinery Orders M/M Jan | 9.50% | 1.80% | 1.60% | |

| 00:00 | AUD | Consumer Inflation Expectations Mar | 5.00% | 5.10% | ||

| 00:30 | AUD | Employment Change Feb | 64.6K | 48.5K | -11.5K | -10.9K |

| 00:30 | AUD | Unemployment Rate Feb | 3.50% | 3.60% | 3.70% | |

| 04:30 | JPY | Industrial Production M/M Jan F | -5.30% | -4.60% | -4.60% | |

| 08:00 | CHF | SECO Economic Forecasts | ||||

| 12:30 | CAD | Wholesale Sales M/M Jan | 0.10% | -0.80% | ||

| 12:30 | USD | Initial Jobless Claims (Mar 10) | 205K | 211K | ||

| 12:30 | USD | Housing Starts Feb | 1.32M | 1.31M | ||

| 12:30 | USD | Building Permits Feb | 1.35M | 1.34M | ||

| 12:30 | USD | Import Price Index M/M Feb | -0.20% | -0.20% | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Mar | -16 | -24.3 | ||

| 13:15 | EUR | ECB Main Refinancing Rate | 3.50% | 3.00% | ||

| 13:45 | EUR | ECB Press Conference | ||||

| 14:30 | USD | Natural Gas Storage | -62B | -84B |