Investors are eagerly awaiting the release of February US CPI figures today, although the banking crisis has overshadowed the event. The possibility of a 50bps hike by Fed next week has been priced out by the market. While traders still anticipate a 25bps hike, with a likelihood of over 70% as indicated in the fed funds futures, the chances of no hike at all could rise once again depending on how events unfold in the stock and bond markets.

Major currency pairs and crosses are trading within yesterday’s range, waiting for the next round of market turbulence. Dollar has been the weakest performer so far this week, followed by Euro and Canadian Dollar. Australian and New Zealand Dollars are recuperating from recent losses, while Yen and Swiss Franc are consolidating their gains. There is a chance for Yen and Franc to surge further if risk aversion picks up momentum again.

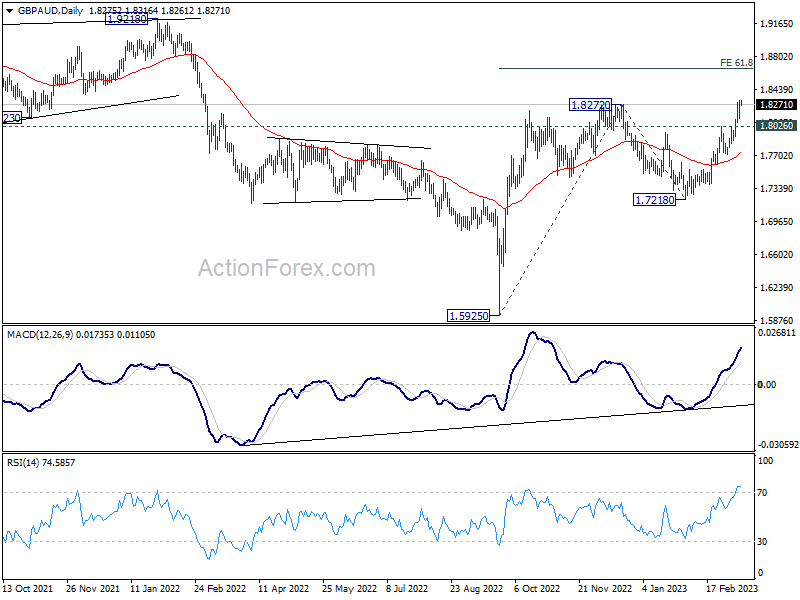

Technically, GBP/AUD is trying to resume the rally from 1.5925 since late last week, but couldn’t get rid of 1.8272 resistance clearly yet. The next move would very much depend on how risk sentiment evolves. For now, further rise is expected as long as 1.8026 support holds. Next target is 61.8% projection of 1.5925 to 1.8272 from 1.7218 at 1.8668.

In Asia, at the time of writing, Nikkei is down -2.37%. Hong Kong HSI is down -2.11%. China Shanghai SSE is down -0.87%. Singapore Strait Times is down -0.22%. Japan 10-year JGB yield is down -0.0489 at 0.257. Overnight,DOW dropped -0.28%. S&P 500 dropped -0.15%. NASDAQ rose 0.45%. 10-year yield dropped -0.18 to 3.515.

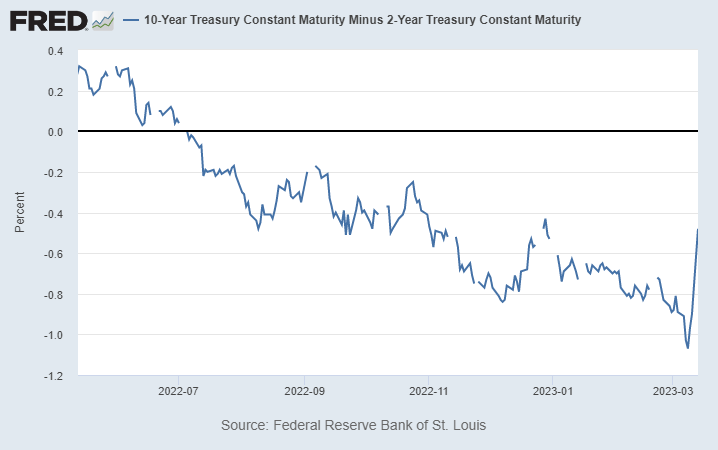

US yield curve inversion unwinding quickly, imminent recession concerns

US Treasury yield has experienced a significant decline as funds continue to pour into bonds due to the collapse of Silicon Valley Bank. Overnight, the 2-year yield dropped by -0.585 to 4.030, after breaching the 4% handle. This is the worst one-day drop since the 2008 global financial crisis. The yield fell by nearly 100 basis points from Wednesday’s 5.066, which was the most significant three-day decline since the 1987 market crash.

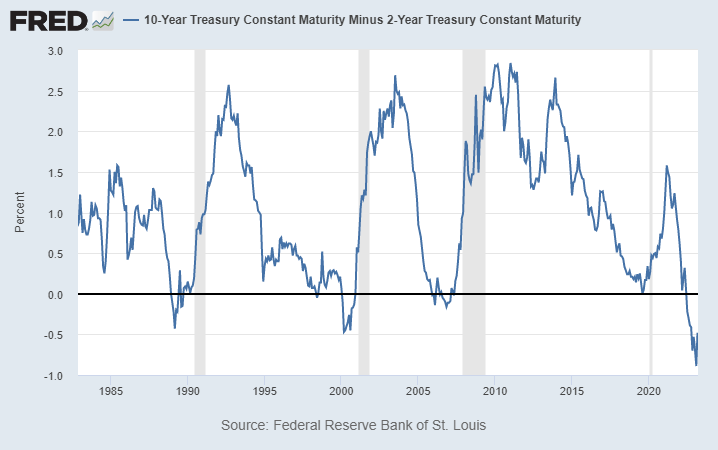

However, an even more critical development is the rapid unwinding of the yield curve inversion. Last week, the 10-year yield was more than 100 basis points below the 2-year yield. But now, it’s around 50 basis points below. It’s still too early to tell if the yield curve is normalizing, but recent history suggests that a recession in the US is imminent if that is the case.

In the first example, for the 1988/90 inversion period, yield curve can be considered fully normalized in April 1990. Recession officially began in July 1990, three months later.

In the second example, for the 2000 inversion period, yield curve can be considered fully normalized in January 2001, and recession started in March 2001, three months later.

In the third example, for the 2006/2007 inversion period, yield curve can be considered fully normalized in June 2007. Recession officially started in December, six months later.

Australia Westpac consumer sentiment unchanged at 78.5, second sub-80 read in a row

Australia Westpac Consumer Sentiment Index was unchanged at 78.5 in March, a second month of extremely weak reading, near historical lows. Areas of most concern remain inflation, interest rates, and the economy.

Westpac noted that there were only one month of sub-80 reading during the COVID pandemic and the global financial crisis period. Runs of sub-80 have only been seen during the recession during the 1980s and 1990s.

Regarding RBA policy, Westpac will wait after release of data on employment, inflation, spending, and confidence, before deciding to change the expectation of a 25bps hike in April. But Westpac maintained the forecast of another 25bps hike in May.

Australia NAB business confidence fell to -4, conditions down to 17

Australia NAB Business Confidence dropped sharply from 6 to -4 in February. Business Conditions dropped from 18 to 17. Looking at some details, trading conditions were unchanged at 27. Profitability conditions dropped from 18 to 14. Employment conditions rose from 11 to 12.

“Overall, the survey confirms the ongoing resilience of the economy through the first months of 2023, though we continue to expect a more material slowdown in demand later in the year when the full effect of rate rises has passed through,” said NAB.

Looking ahead

UK employment data will be the main focus in European session while Swiss will release PPI and Italy will release industrial output.

Later in the day, US CPI will take center stage. Canada will publish manufacturing sales.

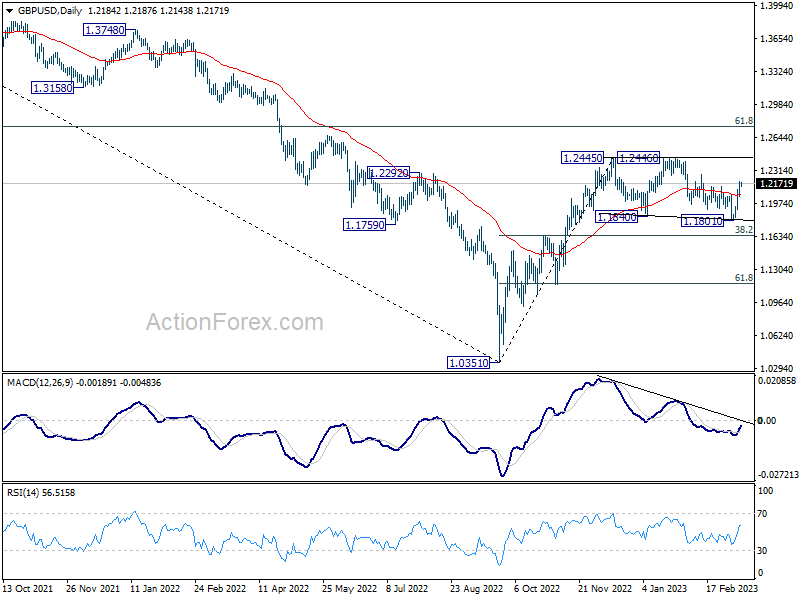

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2087; (P) 1.2143; (R1) 1.2240; More…

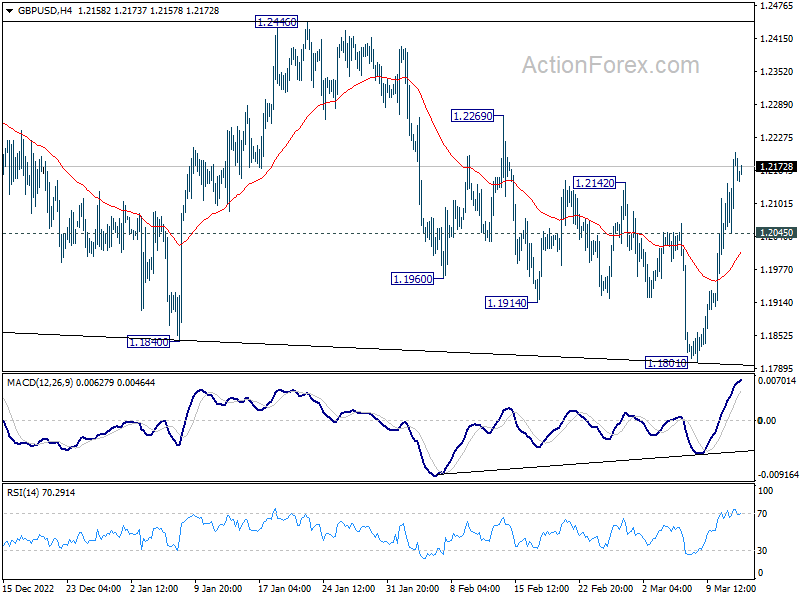

Intraday bias in GBP/USD remains on the upside as rise from 1.1801 is extending. As noted before, the corrective pattern from 1.2445 should have completed with three waves to 1.1801. Further rally should be seen to retest 1.2445/6 resistance zone next. On the downside, below 1.2045 minor support will delay the bullish case and turn intraday bias neutral first.

In the bigger picture, price action from 1.2445 are seen as a corrective pattern to rise from 1.0351 medium term bottom (2022 low). Resumption is expected as a later stage and firm break of 1.2446 will target 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. This will remain the favored case as long as 38.2% retracement of 1.0351 to 1.2445 at 1.1645 holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Mar | 0.00% | -6.90% | ||

| 00:30 | AUD | NAB Business Conditions Feb | 17 | 18 | ||

| 00:30 | AUD | NAB Business Confidence Feb | -4 | 6 | ||

| 07:00 | GBP | Claimant Count Change Feb | -12.4K | -12.9K | ||

| 07:00 | GBP | ILO Unemployment Rate (3M) Jan | 3.80% | 3.70% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jan | 6.60% | 6.70% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Jan | 5.70% | 5.90% | ||

| 07:30 | CHF | Producer and Import Prices M/M Feb | 0.50% | 0.70% | ||

| 07:30 | CHF | Producer and Import Prices Y/Y Feb | 3.40% | 3.30% | ||

| 09:00 | EUR | Italy Industrial Output M/M Jan | -0.40% | 1.60% | ||

| 11:00 | USD | NFIB Business Optimism Index Feb | 91.2 | 90.3 | ||

| 12:30 | CAD | Manufacturing Sales M/M Jan | -0.40% | -1.50% | ||

| 12:30 | USD | CPI M/M Feb | 0.40% | 0.50% | ||

| 12:30 | USD | CPI Y/Y Feb | 6.00% | 6.40% | ||

| 12:30 | USD | CPI Core M/M Feb | 0.40% | 0.40% | ||

| 12:30 | USD | CPI Core Y/Y Feb | 5.50% | 5.60% |