Yen firms up against Dollar in Asian session today, after PPI report adds more bullets for BoJ to start tweaking monetary policy. Investors in Japan are also feeling the risk of stimulus exit, and push Nikkei down more than -1%. Nevertheless, Yen is overall mixed for now. Aussie and Kiwi are so far the firmer ones. Dollar is the weakest, extending last week’s decline while European majors are slightly on the soft side too.

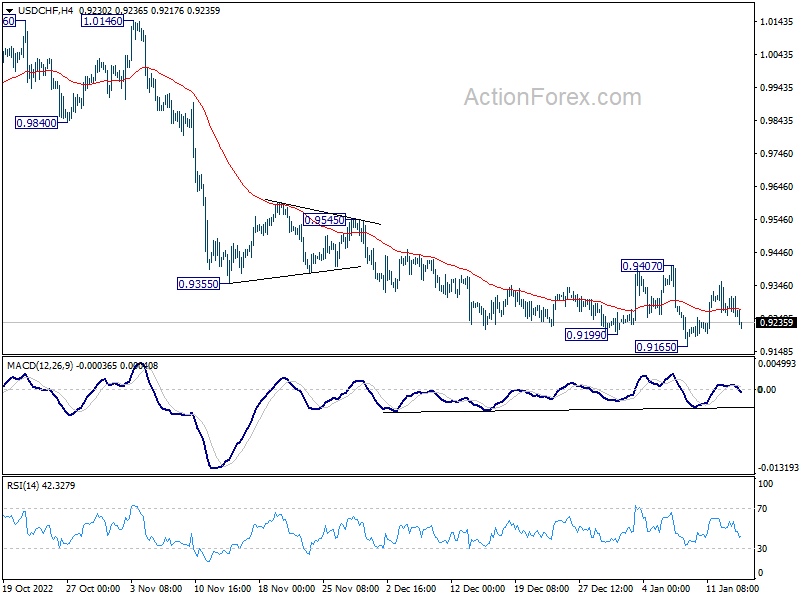

Technically, Swiss Franc is clearly lagging behind others in the rally again the greenback. USD/CHF has indeed failed to break out from range last week. A focus for this week would indeed be on whether USD/CHF would break through 0.9407 resistance to signal short term bottoming. If Dollar is going to rebound, Swissy is currently an easier target.

In Asia, at the time of writing, Nikkei is down -1.16%. Hong Kong HSI is up 0.73%. China Shanghai SSE is up 1.44%. Singapore Strait Times is down -0.19%. Japan 10-year JGB yield is up 0.0005 at 0.512.

Bitcoin pressing resistance after regaining 20k

Bitcoin started the year strongly and regained 20k handle last week. Total market cap also surged past USD 400B level. The move followed overall risk-on sentiment, on expectations that Fed is ready to further slow down the tightening pace. While it’s still early to call for a sustainable trend reversal, the worst looks increasingly likely behind.

Technically, considering bullish convergence condition in daily and week MACD, 15452 should be a medium term bottom at least. Immediate focus is now on 21460 resistance. Firm break there will confirm this case and bring further rise back to 25198 resistance.

Nevertheless, to secure a trend reversal, Bitcoin will need to break through 55 week EMA (now at 25677) in rather decisive manner. Otherwise, it’s probably just setting up the range for some medium term sideway trading instead. So, 25k would be the next level to pay attention to.

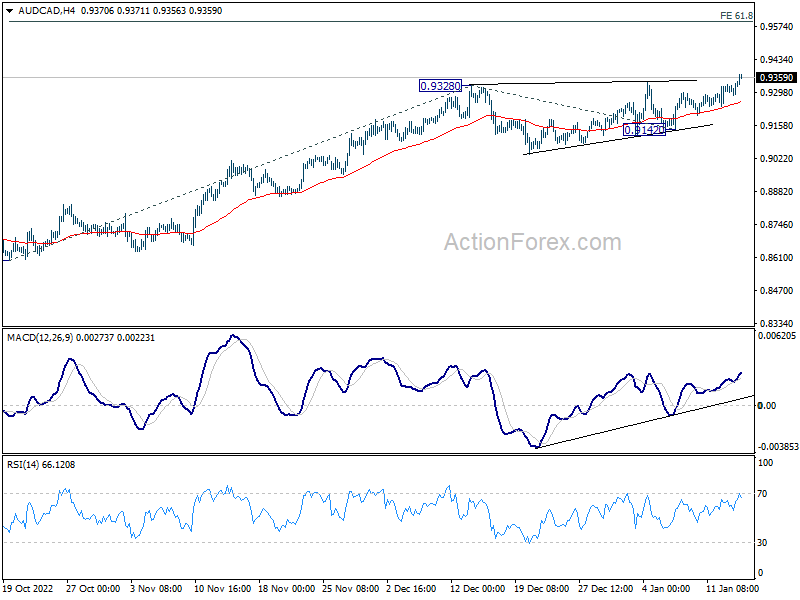

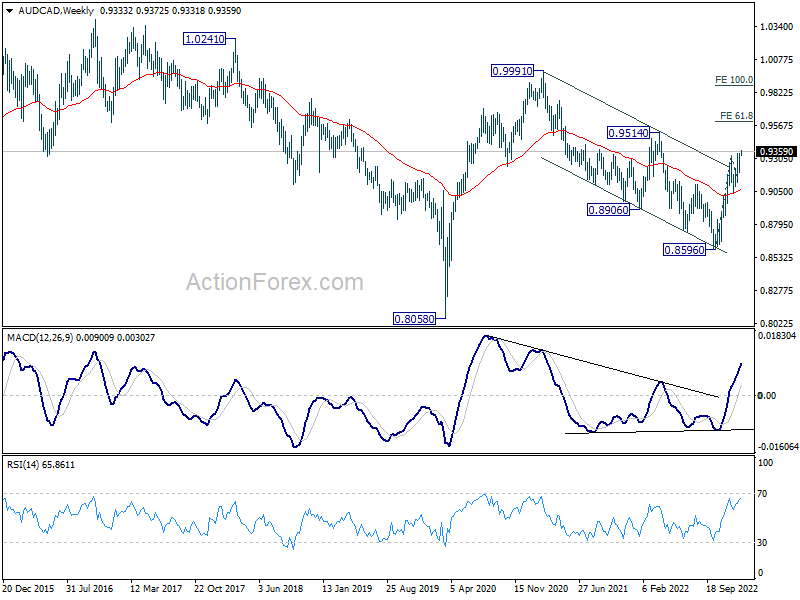

AUD/CAD extending near term rally, to target 0.96 next

While risk on-sentiment is supporting commodity currencies in general, Aussie has been outperforming others recently. Reacceleration in Australian consumer inflation as shown in last week’s November monthly CPI data suggests little room for RBA to pause for now. Additionally, there is optimism over China’s reopening, as well as resumption of coal purchases.

AUD/CAD opened the week with solid buying. the development should confirm resumption of whole rise from 0.8596 low. Near term outlook will stay bullish as long as 0.9142 support holds, even in case of retreat. Next target is 61.8% projection of 0.8596 to 0.9328 from 0.9142 at 0.9594.

During the move, AUD/CAD should also take out 0.9514 resistance to confirm completion of the three-wave corrective decline from 0.9991 (2021 high). That would set the stage for further rally through 0.9991 to resume the rise from 0.8058 (2020 low) in the medium term.

Japan PPI up 10.2% yoy in Dec, second highest on record

Japan PPI rose 10.2% yoy in December, accelerated from 9.7% yoy, above expectation of 9.5% yoy. The reading topped 10% handle for the second time in 2022, marking the second-largest gains on record, following the 10.3% yoy jump in September.

For 2022, wholesale prices rose 9.7% on average, hitting a new record high since comparable data became available in 1981. It’s also twice as fast as in 2021 when a 4.6% increase was reported.

BoJ to highlight the week of more inflation and retail sales data

BoJ meeting will be the main focus of the week. The majority of economists are still expecting no change in monetary policy. Yet, there are some speculations of further tweak in yield curve control, such as lifting the 10-year JGB yield cap to 0.75%. Eventually, BoJ is getting more and more likely to abandon YCC soon and set the stage for rate hike later in the year. So, even if the central bank does nothing, eyes will be on any message regarding the path forward.

Accounts of ECB’s December meeting will also be watched to confirm the message that more 50bps rate hikes lie ahead in at least February and March meeting. Regarding central bank activities, Fed will also publish Beige Book economic report.

On the data front, US retail sales and PPI; Germany ZEW;Japan CPI; UK employment, CPI and retail sales; Canada CPI and retail sales, Australia employment will be closely watched. China will also release Q4 GDP and December data.

Here are some highlights for the week:

- Monday: Australia MI inflation gauge; Japan PPI, machine tools orders;Canada manufacturing sales.

- Tuesday: Australia Westpac consumer sentiment; China GDP, industrial production, retail sales, fixed asset investment; Japan tertiary industry index; Germany CPI final, ZEW economic sentiment; UK employment; Canada CPI, housing starts; US empire state manufacturing.

- Wednesday: BoJ rate decision, Japan machine orders; UK CPI; Eurozone CPI final; Canada IPPI and RMPI; US retail sales, PPI, industrial production, business inventories, NAHB housing index, Fed Beige Book.

- Thursday: Japan trade balance; Australia employment; Swiss PPI; ECB meeting accounts; Canada wholesale sales; US Philly Fed survey, jobless claims, building permits and housing starts.

- Friday: New Zealand BusinessNZ manufacturing; Japan CPI; UK Gfk consumer sentiment, retail sales; Germany PPI; Canada retail sales; US existing home sales.

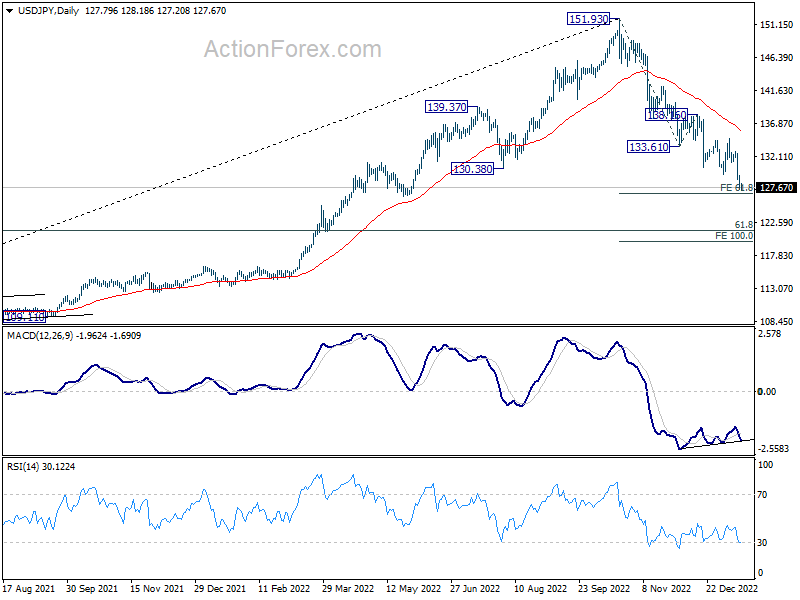

USD/JPY Daily Outlook

Daily Pivots: (S1) 127.07; (P) 128.25; (R1) 129.04; More…

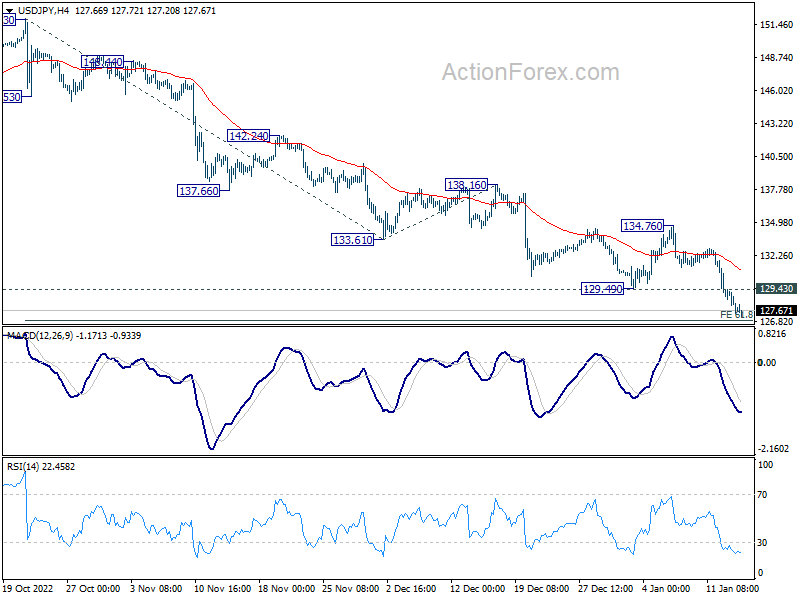

Intraday bias in USD/JPY remains on the downside at this point. Current fall from 1.151.93 in progress for 61.8% projection of 151.93 to 133.61 from 138.16 at 126.83. Break there will target 121.43 fibonacci level next. On the upside, above 129.3 minor resistance will turn intraday bias neutral first. But outlook will remain bearish as long as 134.76 resistance holds.

In the bigger picture, the firm break of 55 week EMA (now at 131.59) raises the chance of medium term bearish reversal, but that’s not confirmed yet. Strong support could be seen around 61.8% retracement of 102.58 to 151.93 at 121.43 and 38.2% retracement of 38.2% retracement of 75.56 to 151.93 at 122.75 to bring rebound. But break of 134.76 resistance is needed to indicate bottoming first. Otherwise further fall will remain in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Dec | 10.20% | 9.50% | 9.30% | 9.70% |

| 00:00 | AUD | TD Securities Inflation M/M Dec | 0.20% | 1.00% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Dec P | -7.70% | |||

| 13:30 | CAD | Manufacturing Sales M/M Nov | 2.30% | 2.80% | ||

| 15:30 | CAD | BoC Business Outlook Survey |