Dollar rises broadly in early US session as lifted by stronger than expected ADP private job data. Meanwhile, stock futures turn south, apparently triggered by affirmation of continuous tightening by Fed. Yet, traders would still hold the larger bets until tomorrow’s non-farm payrolls data. For now, Swiss Franc is following the greenback as the second strongest for the day, then Euro. Sterling, Yen and Aussie are the weakest ones.

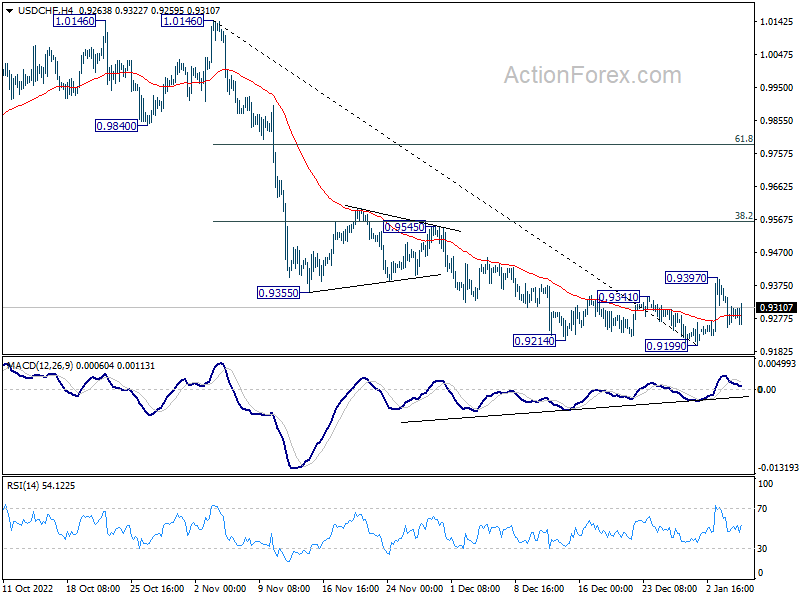

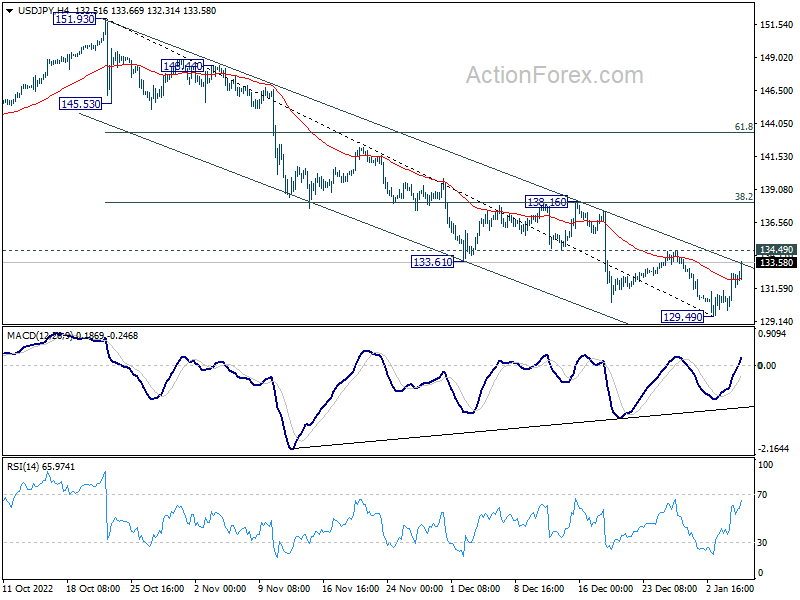

Technically, it should be emphasized again that many Dollar pairs are still range bound. EUR/USD is staying inside 1.0481/0733. AUD/USD is inside 0.6628/0.6892. USD/CHF is inside 0.9199/9397. Even USD/JPY is also inside 129.49/134.49. One-sided breakouts in these pairs are needed to confirm Dollar’s next move, which might happen tomorrow.

In Europe, at the time of writing, FTSE is up 0.59%. DAX is down -0.30%. CAC is down -0.11%. Germany 10-year yield is up 0.0544 at 2.325. Earlier in Asia, Nikkei rose 0.40%. Hong Kong HSI rose 1.25%. China Shanghai SSE rose 1.01%. Singapore Strait Times rose 1.55%. Japan 10-year JGB yield dropped -0.0431 to 0.421.

US ADP jobs rose 245k, strong labor market but fragmented

US ADP private employment grew 245k in December, well above expectation of 145k. By sector, goods-producing jobs rose 22k while service-providing jobs rose 213k. By establishment size, small companies added 195k jobs and medium companies added 191k. But large companies cut -151k jobs. Annual pay for job-stays were up 7.3% yoy,

Nela Richardson Chief Economist, ADP, said: “The labor market is strong but fragmented, with hiring varying sharply by industry and establishment size. Business segments that hired aggressively in the first half of 2022 have slowed hiring and in some cases cut jobs in the last month of the year.”

US initial jobless claims fell to 204k, better than expectations

US initial jobless claims fell -19k to 204k in the week ending December 31, better than expectation of 230k. Four-week moving average of initial claims dropped -7k to 214k. Continuing claims dropped -24k to 1694k in the week ending December 24. Four-week moving average of continuing claims rose 6k to 1688k.

Also released, US trade deficit narrowed to USD -61.5B in November, versus expectation of USD -74.6B. Canada trade surplus narrowed to CAD 0.0B, below expectation of CAD 1.2B.

Eurozone PPI at -0.9% mom, 27.1% yoy in Nov

Eurozone PPI came in at -0.9% mom, 27.1% yoy in November, versus expectation of -0.8% mom, 28.2% yoy. For the month, industrial producer prices decreased by -2.2% mom in the energy sector and by -0.4% mom for intermediate goods, while prices increased by 0.2% mom for durable consumer goods, by 0.3% mom for capital goods and by 0.6% mom for non-durable consumer goods. Prices in total industry excluding energy increased by 0.1% mom.

EU PPI was at -0.9% mom, 27.4% yoy. The largest monthly decreases in industrial producer prices were recorded in Bulgaria (-12.6%), Slovakia (-11.6%) and Greece (-6.0%), while the highest increases were observed in Italy (+3.3%), Sweden (+2.7%) and Ireland (+2.4%).

UK PMI services finalized at 49.9 in Dec, fractional fall in activity

UK PMI Services was finalized at 49.9 in December, up from November’s 48.8. S&P Global said fractional fall in activity was recorded at the end of 2022. Inflation rates were down but still high. Employment was unchanged, ending long period of jobs growth. PMI Composite was finalized at 49.0, up from prior month’s 48.2.

Tim Moore, Economics Director at S&P Global Market Intelligence:

“Around 40% of the survey panel expect a rise in business activity over the next 12 months, while 16% forecast a decline. Survey respondents commented on squeezed disposable incomes, elevated recession risks and a housing market downturn as key factors likely to constrain demand in the year ahead.

“Although service providers widely noted concerns about global economic headwinds and stubbornly high inflation, there were also many reports citing positivity about factors within their control, including forthcoming product launches, expansion into new markets and planned business investment.”

China Caixin PMI composite improved to 48.3, continuing contraction

China Caixin PMI Services rose from 46.7 to 48.0 in December, above expectation of 47.5. PMI Composite rose from 47.0 to 48.3, pointing to contraction in business activity for the fourth straight month.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Both manufacturing and services sectors’ supply and demand contracted due to the pandemic, with manufacturing demand taking a harder hit than in November. Overseas demand was weak, employment remained sluggish, but inflationary pressure was modest, and optimism among businesses significantly improved.

“Covid outbreaks rapidly spread across China in November, causing a number of macroeconomic indicators to fall sharply. On Dec. 7, China announced 10 new measures to further optimize Covid containment. In the short term, infections are expected to explode, which will disrupt production and everyday life. How to effectively coordinate Covid controls with economic and social development has once again become a crucial question.”

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 130.82; (P) 131.77; (R1) 133.61; More…

USD/JPY’s rebound from 129.49 extends higher today but stays below 134.49 resistance. Intraday bias remains neutral first. Considering bullish convergence condition in 4 hour MACD, firm break of 134.49 should confirm short term bottoming. Bias will be turned back to the upside for 138.16 cluster resistance (38.2% retracement of 151.93 to 129.49 at 138.06. On the downside, break of 129.49 will resume the whole decline from 151.93 instead.

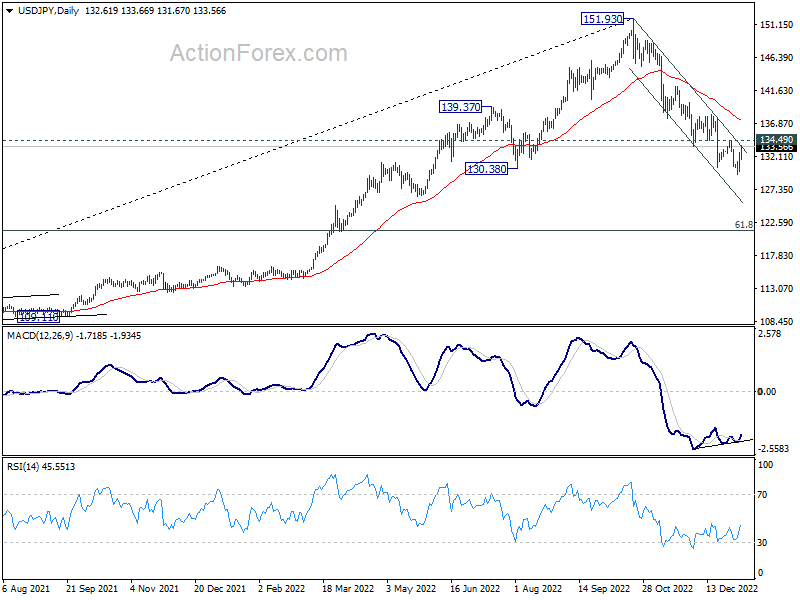

In the bigger picture, a medium term top was in place at 151.93. Sustained trading below 55 week EMA (now at 131.65) would raise the chance of bearish trend reversal. Deeper fall would be seen to 61.8% retracement of 102.58 to 151.93 at 121.43. This will now remain the favored case as long as 55 day EMA (now at 137.26) holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Dec | -6.10% | -3.20% | -6.40% | |

| 01:45 | CNY | Caixin Services PMI Dec | 48 | 47.5 | 46.7 | |

| 05:00 | JPY | Consumer Confidence Index Dec | 30.3 | 29.1 | 28.6 | |

| 07:00 | EUR | Germany Trade Balance (EUR) Nov | 10.8B | 7.5B | 6.9B | |

| 09:30 | GBP | Services PMI Dec F | 49.9 | 50 | 50 | |

| 10:00 | EUR | Eurozone PPI M/M Nov | -0.90% | -0.80% | -2.90% | |

| 10:00 | EUR | Eurozone PPI Y/Y Nov | 27.10% | 28.20% | 30.80% | |

| 12:30 | USD | Challenger Job Cuts Y/Y Dec | 129.10% | 416.50% | ||

| 13:15 | USD | ADP Employment Change Dec | 235K | 145K | 127K | |

| 13:30 | USD | Initial Jobless Claims (Dec 30) | 204K | 230K | 225K | 223K |

| 13:30 | USD | Trade Balance (USD) Nov | -61.5B | -74.6B | -78.2B | -77.9B |

| 13:30 | CAD | Trade Balance (CAD) Nov | 0.0B | 1.2B | 1.2B | |

| 14:45 | USD | Services PMI Dec F | 44.4 | 44.4 | ||

| 15:30 | USD | Natural Gas Storage | -230B | -213B | 0.13B | |

| 16:00 | USD | Crude Oil Inventories | 1.5M | 0.7M |