Aussie rises broadly today on news that China is considering to lift the ban on its coal partially. The move also takes Kiwi higher. On the other hand, Dollar is turning softer together with loonie. Despite yesterday’s rally attempt, the greenback is clearly hesitating ahead of today’s ISM manufacturing and FOMC minutes, as well as Friday’s non-farm payrolls. Yen is still the strongest for the week but it’s now consolidating some gains. European majors are mixed, with Euro on the softer side.

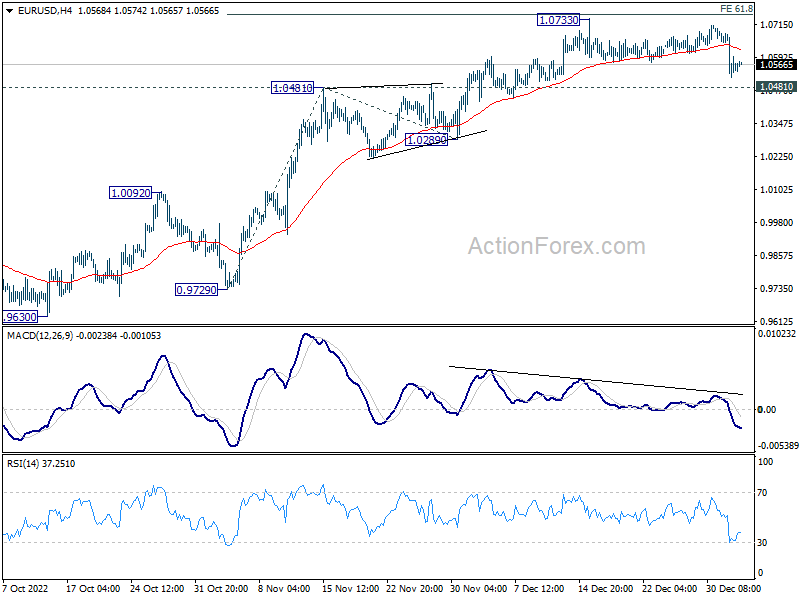

Technically, development in EUR/USD will be a key focus of the week. Conditions are there for the pair to at least correct the whole rally from 0.9534 low. But it needs to break through 1.0481 resistance turned support first. In that case, deeper fall would be seen to 1.0289 support and possibly below. However, strong rebound from 1.0481 will maintain near term bullishness for another rise through 1.0733, sooner rather than later.

In Asia, Nikkei closed down -1.45%. Hong Kong HSI is up 2.48%. China Shanghai SSE is up 0.11%. Singapore Strait Times is down -0.05%. Japan 10-year JGB yield is up 0.0427 at 0.458. Overnight, DOW dropped -0.03%. S&P 500 dropped -0.40%. NASDAQ dropped -0.76%. 10-year yield dropped -0.086 to 3.793.

ECB Kazaks see significant rate increases at Feb and Mar meetings

ECB Governing Council member Martins Kazaks said yesterday, “in the next two meetings I think we can still do quite large steps” on interest rates.

“Of course the steps may become smaller as necessary as we find the level appropriate to bring the inflation down to 2%,” he added.

“Currently I would see that at the February and March meetings we will have significant rate increases,” he said.

BoJ Kuroda expects economy to grow firmly and stably this year

BoJ Governor Haruhiko Kuroda told the bankers’ association that Japan is facing uncertainties “such as inflation and pandemic. Yet, he expects the economy to “firmly and stably this year backed by accommodative monetary conditions.”

Kuroda reiterated that the central bank would keep monetary easing to achieve the 2% inflation target accompanied by wage growth.

Separately, Prime Minister Fumio Kishida said on a radio program that aired Tuesday, “raising interest rates has an impact on people’s day-to-day lives and small and midsize businesses It’s not the case that all that needs to be done is to raise rates. The government and the Bank of Japan each have a role to play.”

Japan PMI manufacturing finalized at 48.9, slipped further into contraction

Japan PMI Manufacturing was finalized at 48.9 in December, down from November’s 49.0. That’s the lowest level since October 2020. S&P Global noted there were strong reductions in output volumes and order books. Input buying was cut at strongest rate since September 2020. Supply pressures were the least widespread since February 2021.

Laura Den man, Economist at S&P Global Market Intelligence, said: “December PMI data saw the Japanese manufacturing sector slip further into contraction territory in the final month of 2022. The downturn was largely centred around the current demand environment which is weak both internationally and domestically….

“At the same time, forward looking indicators are increasingly painting a gloomier picture for Japan’s manufacturing sector in the future. Companies have cut back input buying sharply, and business sentiment waned to a seven-month low.”

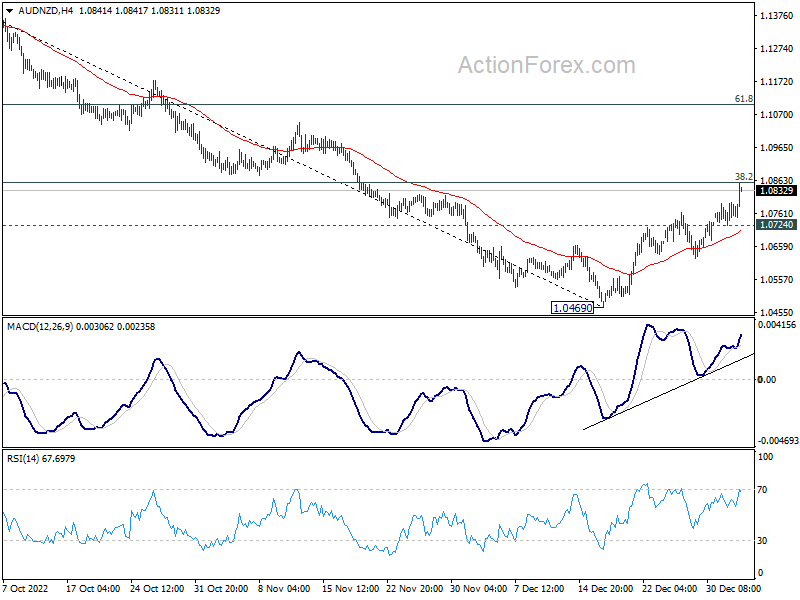

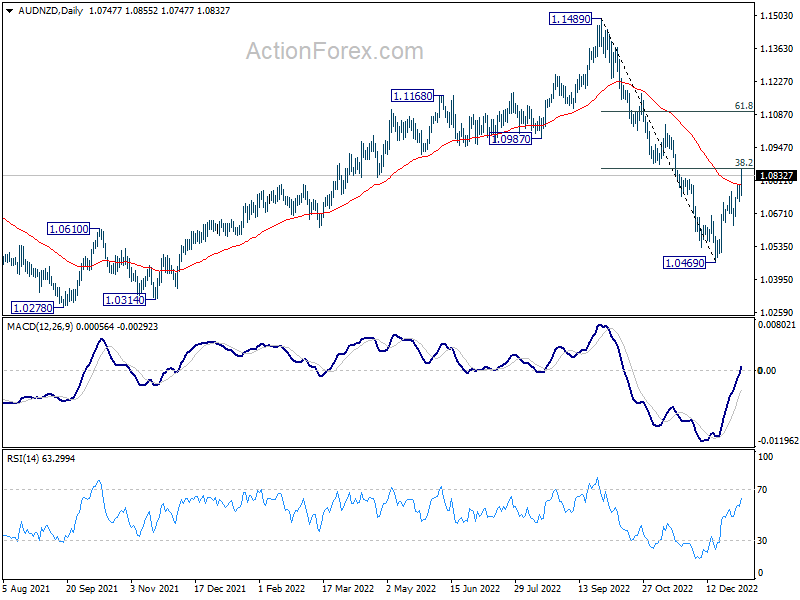

China considering to ease Australian coal ban, AUD/NZD jumps

Australian Dollar rises broadly on news that China is considering to partially ease the ban on its coals. Bloomberg reported that China’s National Development and Reform Commission held talks yesterday on proposals to allow four major coal importers to make new purchases on Australian coal this year, effective as soon as April 1.

AUD/NZD extends the rebound from 1.0469 and hits as high as 1.0855 so far. For now, further rally is expected in the cross as long as 1.0724 support holds. Sustained trading above 38.2% retracement of 1.1489 to 1.0469 at 1.0859 will pave the way to 61.8% retracement at 1.1099, even as a corrective move.

Looking ahead

Swiss CPI, Eurozone PMI services final, and UK mortgage approvals will be released in European session. US ISM manufacturing and FOMC minutes will be the main features later in the day.

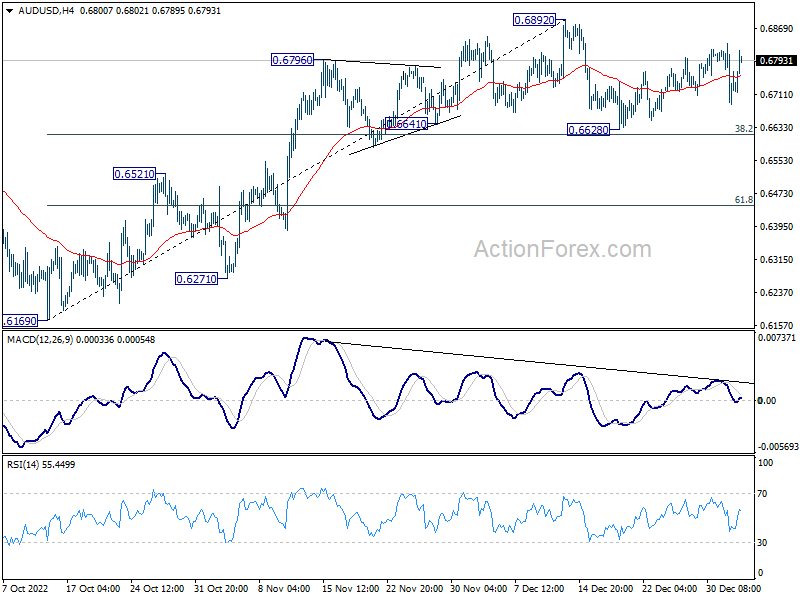

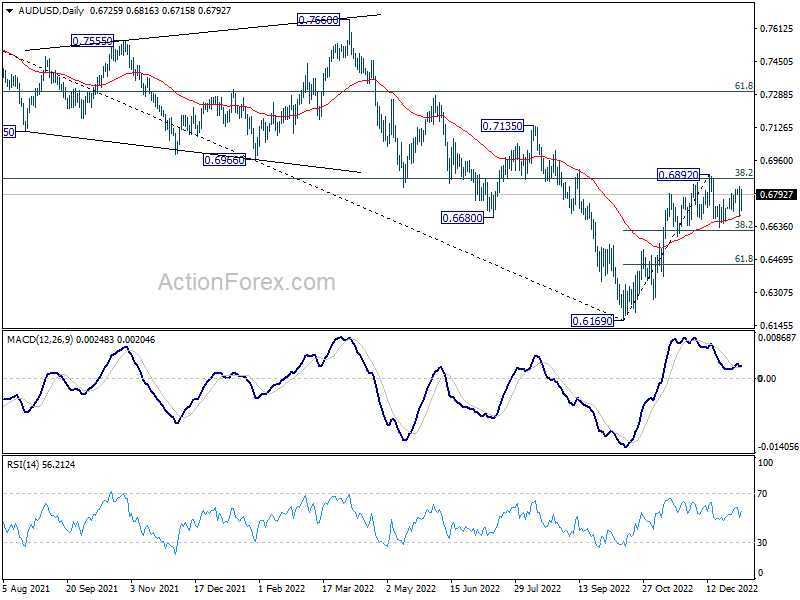

AUD/USD Daily Report

Daily Pivots: (S1) 0.6665; (P) 0.6750; (R1) 0.6812; More…

AUD/USD rebounds notably today but stays in range of 0.6628/6892. Intraday bias remains neutral for the moment. On the downside, sustained break of 38.2% retracement of 0.6169 to 0.6892 at 0.6616 will indicate rejection by 0.66871 fibonacci level. Deeper fall should then be seen to 61.8% retracement at 0.6445. On the upside, break of 0.6892 will resume the rally from 0.6169.

In the bigger picture, it’s still unsure if price actions from 0.6169 medium term bottom are developing into a corrective pattern or trend reversal. Rejection by 38.2% retracement of 0.8006 to 0.6169 at 0.6871 will maintain medium term bearishness for another fall through 0.6169 at a later stage. However, firm break of 0.6871, and sustained trading above 55 week EMA (now at 0.6894) will raise the chance of the start of a bullish up trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:01 | GBP | BRC Shop Price Index Y/Y Nov | 7.30% | 7.40% | ||

| 00:30 | JPY | Manufacturing PMI Dec F | 48.9 | 48.8 | 48.8 | |

| 07:00 | EUR | Germany Import Price Index M/M Nov | -1.70% | -1.20% | ||

| 07:30 | CHF | CPI M/M Dec | 0.00% | 0.00% | ||

| 07:30 | CHF | CPI Y/Y Dec | 3.40% | 3.00% | ||

| 08:45 | EUR | Italy Services PMI Dec | 47.6 | 49.5 | ||

| 08:50 | EUR | France Services PMI Dec F | 48.1 | 48.1 | ||

| 08:55 | EUR | Germany Services PMI Dec F | 49 | 49 | ||

| 09:00 | EUR | Eurozone Services PMI Dec F | 49.1 | 49.1 | ||

| 09:30 | GBP | Mortgage Approvals Nov | 54K | 59K | ||

| 09:30 | GBP | M4 Money Supply M/M Nov | 0.20% | 0.00% | ||

| 15:00 | USD | ISM Manufacturing PMI Dec | 48.6 | 49 | ||

| 15:00 | USD | ISM Manufacturing Prices Paid Dec | 42.3 | 43 | ||

| 15:00 | USD | ISM Manufacturing Employment Index Dec | 48.4 | |||

| 19:00 | USD | FOMC Minutes |