The financial markets are trading more on the risk-on side as the year-end is approaching. But reactions in the forex markets are relatively mild. Yen continues to be the worst performer for the week but selloff is somewhat slowing. Euro and Sterling are soft with Dollar. Commodity currencies are the relatively stronger ones but have already pared much of the earlier gains. With most traders away, the committed moves might only come next week.

In Asia, at the time of writing, Nikkei is down -1.05%. Hong Kong HSI is down -0.92%. China Shanghai SSE is down -0.29%. Singapore Strait Times is down -0.84%. Japan 10-year JGB yield is down -0.007 at 0.450. Overnight, DOW dropped -1.10%. S&P 500 dropped -1.20%. NASDAQ dropped -1.35%. 10-year yield rose 0.027 to 3.887.

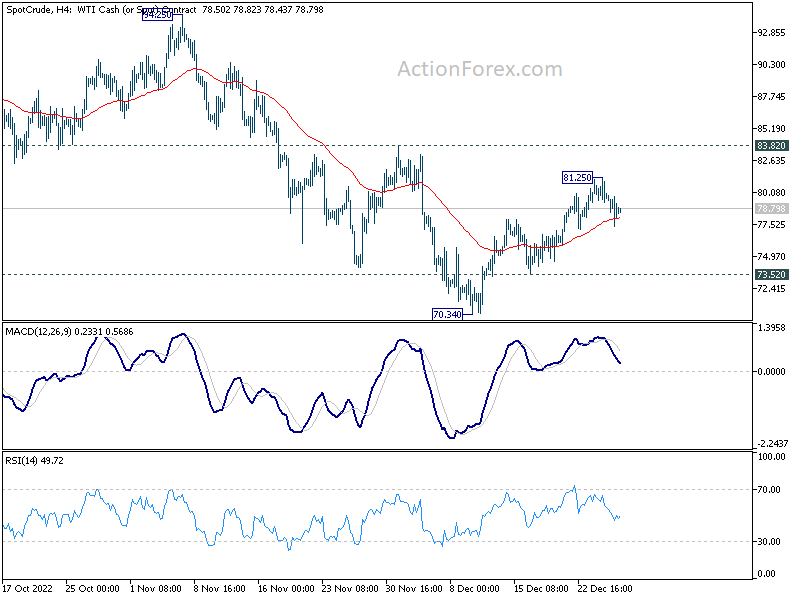

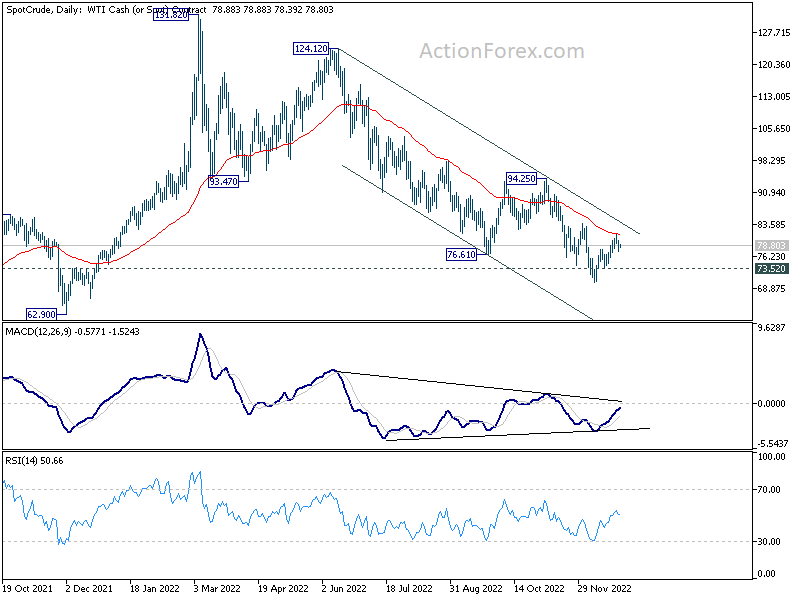

WTI oil down as China boost fades

Oil prices closed lower overnight as the near term rebound appeared to be fading. The optimism over a surge in demand in China was replaced by concerns over infections in the country, as well as its outbound tourists. A regional councillor in Italy confirmed that half of passengers on China flight to Lombardy were tested COVID positive. US also announced to require travelers from China, including Hong Kong, to show negative Covid-19 test result before flights.

WTI crude oil’s rebound from 70.34 stalled after hitting 55 day EMA. It’s also kept well inside the medium term falling channel from 124.12. While bullish convergence condition is seen in daily MACD, bearishness is maintained with recent development. Further decline from current level, followed by break of 73.52 support should confirm that the corrective rebound has completed in a three wave structure. Larger down trend should then be ready to resume through 70.34 low, towards next support level at 62.90.

NASDAQ closed at new 2022 low, but a turnaround soon?

NASDAQ closed at new 2022 low at 10213.28 overnight as investor sentiment turned sour in thin holiday trading. Technically, it’s still staying above intraday low at 10088.82, but a break of that level should be seen soon, probably 10000 handle too.

Technically, the key level lies in 9660/89 cluster projection level (61.8% projection of 16212.22 to 10565.13 from 13181.08 at 9689.96, 61.8% projection of 13181.08 to 10088.82 from 11571.64 at 9660.62). Strong support from this cluster level in January could set up the markets for a trend reversal attempt in the first half of 2023. But sustained break there would set up down trend extension for the upcoming period.

We’ll soon find out whether a turn in the market is around the corner.

Looking ahead

Eurozone M3 money supply and US jobless claims will be released today.

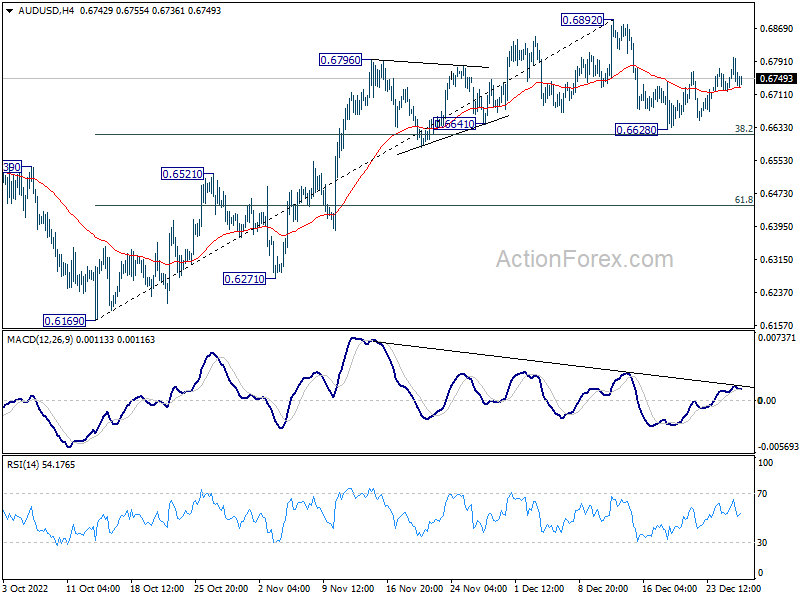

AUD/USD Daily Report

Daily Pivots: (S1) 0.6706; (P) 0.6753; (R1) 0.6788; More…

AUD/USD is staying in range of 0.6628/6892 and intraday bias remains neutral first. On the downside, sustained break of 38.2% retracement of 0.6169 to 0.6892 at 0.6616 will indicate rejection by 0.66871 fibonacci level. Deeper fall should then be seen to 61.8% retracement at 0.6445. On the upside, break of 0.6892 will resume the rally from 0.6169.

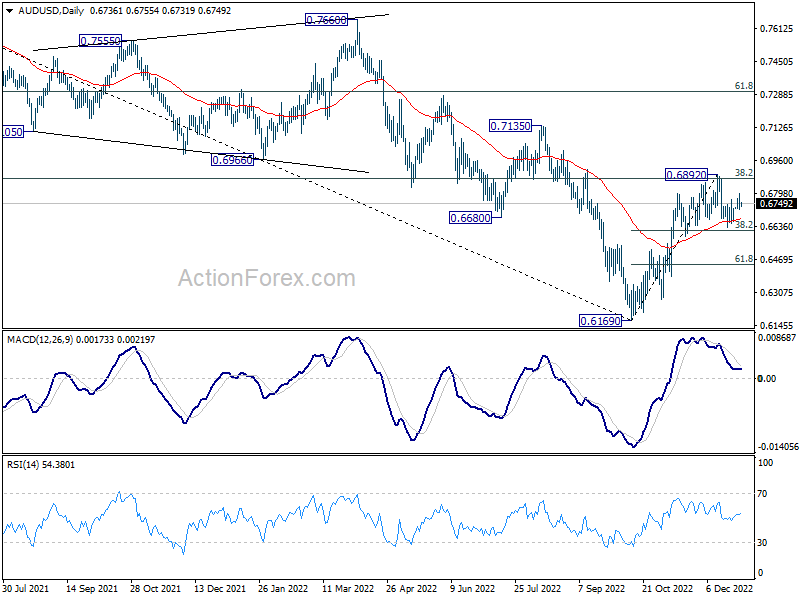

In the bigger picture, it’s still unsure if price actions from 0.6169 medium term bottom are developing into a corrective pattern or trend reversal. Rejection by 38.2% retracement of 0.8006 to 0.6169 at 0.6871 will maintain medium term bearishness for another fall through 0.6169 at a later stage. However, firm break of 0.6871, and sustained trading above 55 week EMA (now at 0.6896) will raise the chance of the start of a bullish up trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Nov | 5.00% | 5.10% | ||

| 13:30 | USD | Initial Jobless Claims (Dec 23) | 225K | 216K | ||

| 15:30 | USD | Natural Gas Storage | -198B | -87B | ||

| 16:00 | USD | Crude Oil Inventories | -1.2M | -5.9M |

breakout perfect entry #forex #crypto #trading #trending

breakout perfect entry #forex #crypto #trading #trending