Yen’s selloff continues today, so are the rallies in US and European benchmark treasury yields. While the cap on 10-year JGB yields was raised earlier this month, there is still a cap. On the other hand, market sentiments appeared to be boosted by relaxation of outbound travel in China. Additionally, BoJ’s Summary of Opinions indicated that the board is in no way ready to exit the ultra loose monetary policy yet. As for today, Euro and Dollar are the next weakest while Kiwi and Aussie are the strongest ones.

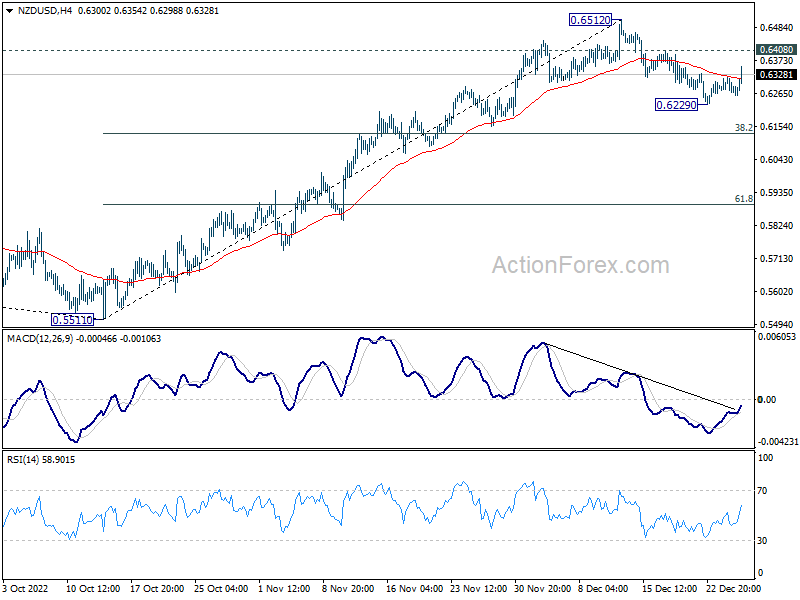

Technically, NZD/USD’s break of 4 hour 55 EMA suggests that correction from 0.6512 has completed earlier than expected at 0.6629. Further rise is mildly in favor to 0.6408 resistance. Break there will bring retest of 0.6512 high. However, rejection by 0.6408 will still extend the correction from 0.6512 to 38.2% retracement of 0.5511 to 0.6512 at 0.6130.

In Europe, at the time of writing, FTSE is up 0.79%. DAX is down -0.13%. CAC is flat. Germany 10-year yield is up 0.109 at 2.496. Earlier in Asia, Nikkei dropped -0.41%. Hong Kong HSI rose 1.56%. China Shanghai SSE dropped -0.26%. Singapore Strait Times rose 0.02%. Japan 10-year JGB yield dropped -0.011 to 0.457.

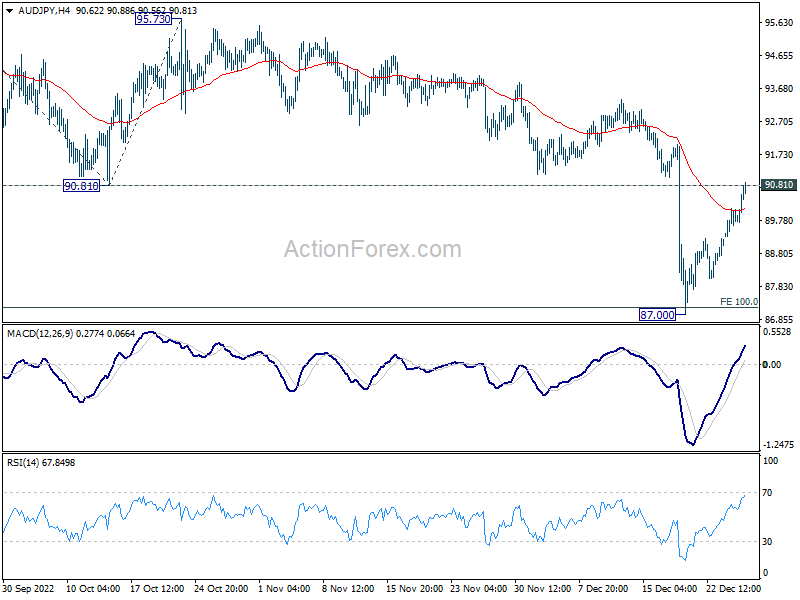

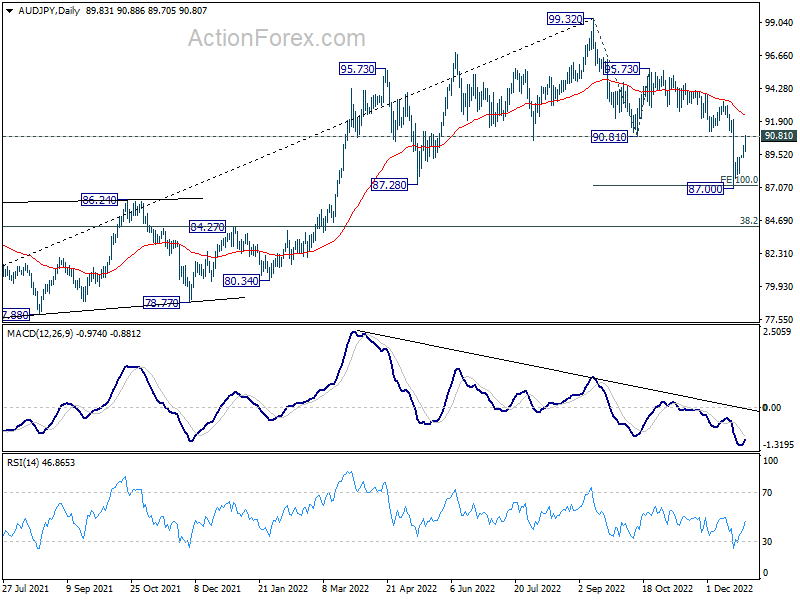

AUD/JPY extends rebound, hopeful for bounce in Chinese tourists

Australian Dollar is among the strongest ones for today, and appeared to be give a lift by China’s resumption of issuing outbound visas from January 8. Australia is among the top 10 destinations with fastest-growing search volume in China after the news, indicating its popularity in Chinese tourists. Tourism operators are hopeful that visitations will rebound strongly, which is 95 below the pre-pandemic levels.

Japan, India, Italy and South Korea all said they would be imposing tighter COVID-testing requirements on tourists from China, with concerns on the lack of transparency on infections and variants in the country. But there is nothing heard from the Australian government yet.

AUD/JPY is extending the rebound from 87.00, and it’s now pressing 90.81 key near term support turned resistance. Sustained break there will argue that corrective fall from 99.32 has completed at 87.00, after hitting 100% projection of 99.32 to 90.81 from 95.73 at 87.22. In such case, stronger rise should be seen back to 95.73/99.32 range, as the second leg of the corrective pattern from 99.32.

BoJ Opinions: Expansion of 10-yr yield fluctuations enhances sustainability of YCC

In the Summary of Opinions at BoJ’s December 19-20 meeting, several members noted that Japan is currently in a “critical phase” in achieving 2% inflation target. One noted that “signs of a virtuous cycle have started to be seen” between wages and prices”. This is “evidenced by the overall high levels of corporate profits and moves to increase wages amid tight labor market conditions.”

But “price stability is not considered to have been achieved”. Thus, it’s appropriate for BoJ to continue with the Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control for as long as necessary, to “firmly support the economy and realize a favorable environment for firms to raise wages.

Many members noted the “deterioration in the functioning of bond markets”, and “distortion in the price formation of 10-year bonds”. Expansion of the range of 10-year JGB yield fluctuation will address the deterioration and distortion. But it’s “not intended to change the direction of monetary easing”. The expansion will “contribute to enhancing the sustainability of yield curve control”.

Japan industrial production down -0.1% mom in Nov, output weakening

Japan industrial production declined -0.1% mom in November, better than expectation of -0.2% mom. But that’s still the third straight month of contraction, followed -3.2% mom in October and -1.7% mom in September.

Looking at some details, general machinery output was down -7.9%, production machinery was down -5.7% while auto products was down -0.8%.

The Ministry of Economy, Trade and Industry downgraded the assessment of industrial production to “weakening”. It expects output to rebound by 2.8% in December, then decrease -0.6% in January.

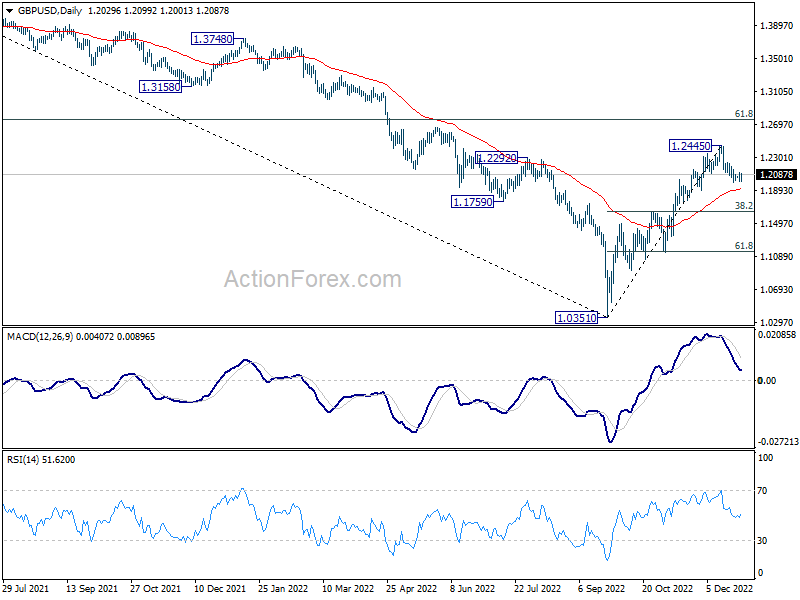

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1985; (P) 1.2049; (R1) 1.2094; More…

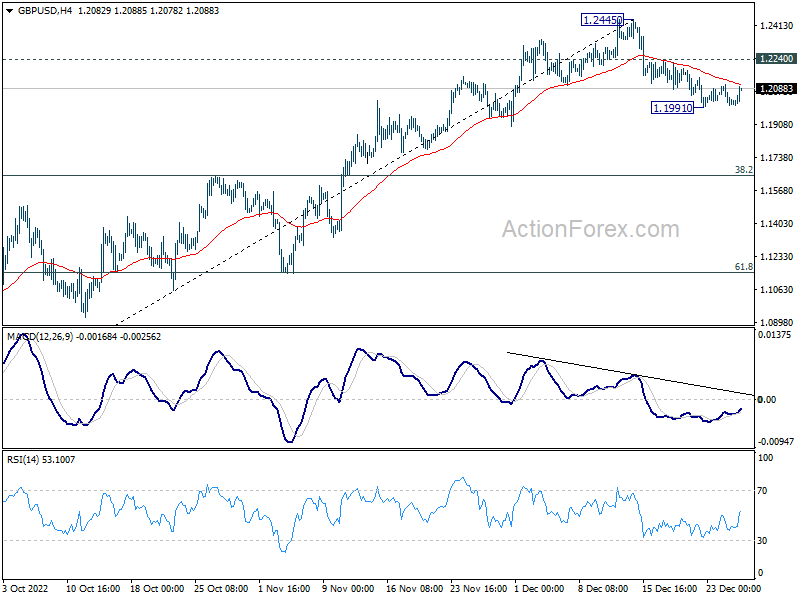

GBP/USD recovers mildly today but stays in tight range. Intraday bias remains neutral for the moment. On the downside, break of 1.1991 will resume the fall from 1.2445 to 55 day EMA (now at 1.1916). Firm break there will target 38.2% retracement of 1.0351 to 1.2445 at 1.1645. On the upside, break of 1.2240 minor resistance will turn bias back to the upside for retesting 1.2445 instead.

In the bigger picture, rise from 1.0351 medium term bottom is at least correcting whole down trend from 1.4248 (2021 high). Further rise is expected as long as 1.1644 resistance turned support holds. Next target is 61.8% retracement of 1.4248 to 1.0351 at 1.2759. Sustained break there will pave the way back to 1.4248. This will remain the favored case as long as 55 day EMA (now at 1.1916) holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 23:50 | JPY | Industrial Production M/M Nov P | -0.10% | -0.20% | -3.20% | |

| 09:00 | CHF | Credit Suisse Economic Expectations Dec | -42.8 | -57.5 | ||

| 15:00 | USD | Pending Home Sales M/M Nov | -1.20% | -4.60% |

breakout perfect entry #forex #crypto #trading #trending

breakout perfect entry #forex #crypto #trading #trending This “NEW CONCEPT” Trading Strategy Prints Money!… (INSANE Results!)

This “NEW CONCEPT” Trading Strategy Prints Money!… (INSANE Results!)