Yen remains the biggest winner of the day, and maintains most gains in early US session. It remains to be seen how long the impact of BoJ’s tweak of the yield curve control would last. But any, Yen is enjoying the ride for now. Australian and New Zealand Dollar are the weaker ones so far, but others are mixed against each other. US and Canadian Dollars are having slight upper hands over Europeans. But respects pairs are generally range bound.

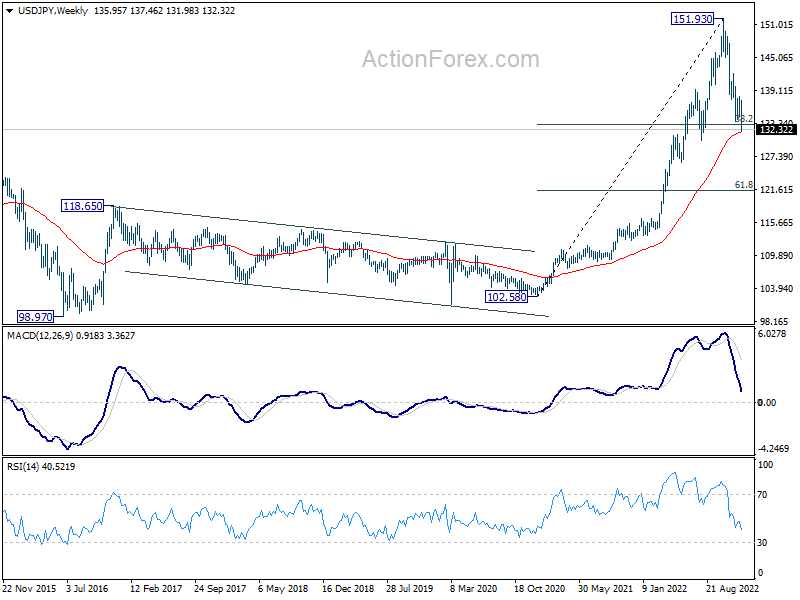

Technically, it should be noted that USD/JPY is now in proximity to 55 week EMA (now at 131.72) after today’s steep decline. The EMA could provide enough support for at least an interim rebound. If that happens, it would likely be accompanied by a strong bounce in Dollar elsewhere, including break of 1.0481 support in EUR/USD and 0.9378 resistance in USD/CHF. Let’s see.

In Europe, at the time of writing, FTSE is up 0.04%. DAX is down -0.33%. CAC is down -0.27%. Germany 10-year yield is up 0.075 at 2.279. Earlier in Asia, Nikkei dropped -2.46%. Hong Kong HSI dropped -1.33%. China Shanghai SSE dropped -1.07%. Singapore Strait Times dropped -0.08%. Japan 10-year JGB yield rose 0.1619 to 0.418.

Canada retail sales rose 1.4% mom in Oct, but volume was unchanged

Canada retail sales rose 1.4% mom to CAD 62.0B in October, below expectation of 1.5% mom, and the largest in crease in five month. Sales were up in 6 out of 11 subsectors, representing 84.4% of retail trade. Growth was led by higher sales at gasoline stations (+6.8%) and food and beverage stores (+2.2%). Excluding gasoline stations and motor vehicle and parts, sales rose 0.9%.

In volume terms, retail sales were unchanged for the month.

Based on advance estimate, sales decreased -0.5% mom in November.

BoJ tweaks YCC to allow 10-yr yield to rise to 0.50%

BoJ surprises the markets today by widening the band of 10-year JGB yield from 0.25% to 0.50% today. At the same time, short term policy rate is kept unchanged at -0.10% as expected.

Under the yield curve control framework, the central bank will still continue to purchases JGBs without an upper limit to keep 10-year yield at around 0%. But now, the bank will offer to purchase 10-year JGB yields at 0.50% every business day through fixed-rate operations, effectively allowing 10-year yield to rise towards 0.50% level.

BoJ Kuroda: Yield cap raised to correction distortions in yield curve

BoJ Governor Haruhiko Kuroda said in the post meeting press conference, “Overseas market volatility has heightened from around spring … While we have kept the 10-year bond yield from exceeding the 0.25% cap, this has caused some distortions in the shape of the yield curve. We, therefore, decided that now was the appropriate timing to correct such distortions and enhance market functions.” That’s led to the decision today to raise the cap from 0.25% to 0.50%.

“Consumer inflation has hit 3.6% mainly through rising import costs from a weak yen. Furthermore, inflation expectations are heightening. This is pushing down real interest rates and enhancing the stimulus effect on the economy. As such, while we’ve (widened the band) to correct distortions in the yield curve, the move won’t diminish the effect of YCC,” he added.

But Kuroda also indicated, “I don’t think we need to review YCC or quantitative easing for the time being.” “It’s premature to debate specifics on changing the monetary policy framework or an exit from easy policy. When achievement of our target comes into sight, the BOJ’s policy board will hold discussions on an exit strategy and offer communication to markets,” he said.

RBA considered 50bps, 25bps, and no change at Dec meeting

Minutes of RBA’s December 6 meeting indicates that the board has considered three interest rate options of a 50bps hike, a 25bps hike, and no change.

The argument for a 50bps increase stemmed from inflation remains “too high”, and there were factors support a “more pre-emptive action”. For a 25bps increase, the board acknowledged there had bee already a “significant cumulative increase” in interest rates and they would “begin to have more of an effect through the course of 2023″. The arguments for now chance placed”further emphasis of the lagged effect” of prior rate increases.

Board members eventually decided that the case for 25bps increase was the”strongest one”, as further hike was “likely to be necessary”. Members also noted the “importance of acting consistently”.

The minutes also reiterated that “the Board expects to increase interest rates further over the period ahead, but it is not on a pre-set path. Members noted that the size and timing of future interest rate increases would continue to be determined by the incoming data and the Board’s assessment of the outlook for inflation and the labour market.”

NZ ANZ business confidence fell to fresh record low

New Zealand ANZ business confidence declined from -57.1 to -70.2 in December, a new record low. Looking at some details, own activity outlook fell from -13.7 to -25.6. Export intentions dropped form -5.4 to -10.0. Investment intentions dropped form -8.1 to -20.5. Employment intentions dropped from -4.0 to -16.3. Pricing intentions rose from 58.5 to 59.1. Cost expectations declined form 88.7 to 84.4. Inflation expectations dropped from 6.39 to 6.23.

ANZ said: “The fall in business confidence is certainly dramatic, but while it’s at a fresh record low, it would be incorrect to read this as an indication that any recession is likely to be unusually severe. Rather, it’s unusually widely anticipated. It’s a situation unprecedented in recent decades for a central bank to admit it is deliberately engineering a recession.”

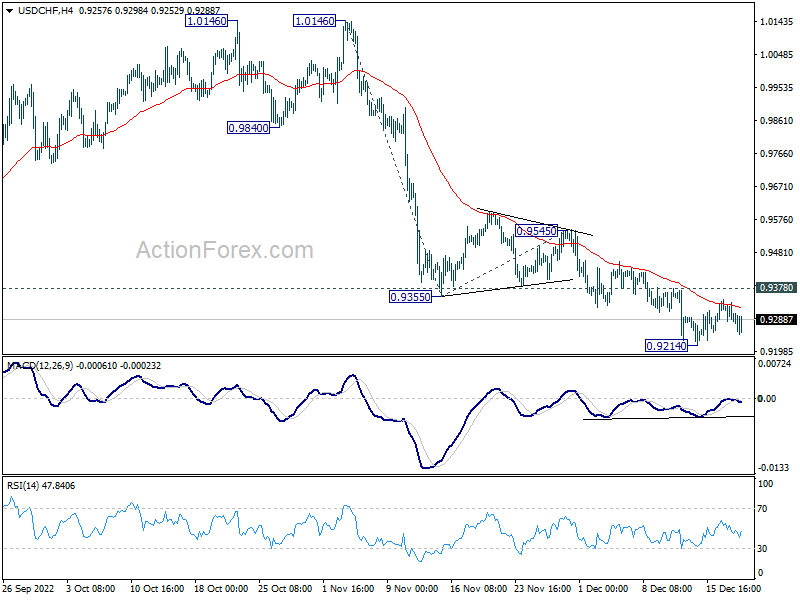

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9265; (P) 0.9307; (R1) 0.9328; More…

Intraday bias in USD/CHF remains neutral for the moment, but further decline is in favor with 0.9378 resistance intact. On the downside, break of 0.9214 will resume the fall and target 61.8% projection of 1.0146 to 0.9355 from 0.9545 at 0.9056. However, break of 0.9378 resistance will indicate short term bottoming and turn bias back to the upside for 0.9545 resistance instead.

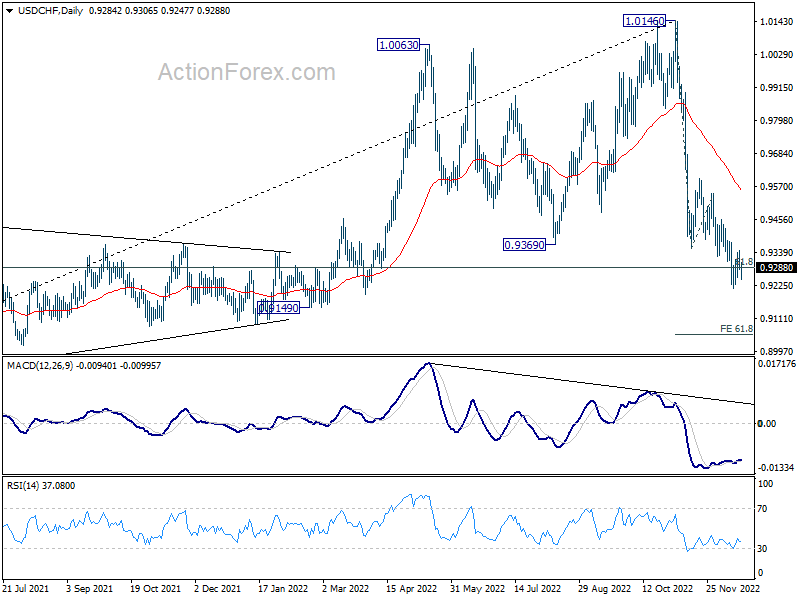

In the bigger picture, rise from 0.8756 (2021 low) has completed at 1.0146, well ahead of 1.0342 long term resistance (2016 high). Based on current downside momentum, fall from 1.0146 might be a medium term down trend itself. Sustained break of 61.8% retracement of 0.8756 to 1.0146 at 0.9287 will pave the way to 0.8756. In any case, risk will stay on the downside as long as 0.9545 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Dec | -70.2 | -57.1 | ||

| 00:30 | AUD | RBA Minutes | ||||

| 03:00 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 07:00 | CHF | Trade Balance (CHF) Nov | 2.31B | 3.27B | 4.14B | 4.27B |

| 07:00 | EUR | Germany PPI M/M Nov | -3.90% | -2.60% | -4.20% | |

| 07:00 | EUR | Germany PPI Y/Y Nov | 28.20% | 30.00% | 34.50% | |

| 09:00 | EUR | Eurozone Current Account (EUR) Oct | -0.4B | -10.3B | -8.1B | |

| 13:30 | CAD | Retail Sales M/M Oct | 1.40% | 1.50% | -0.50% | |

| 13:30 | CAD | Retail Sales ex Autos M/M Oct | 1.70% | 1.30% | -0.70% | |

| 13:30 | USD | Building Permits Nov | 1.34M | 1.50M | 1.51M | |

| 13:30 | USD | Housing Starts Nov | 1.43M | 1.40M | 1.43M | |

| 15:00 | EUR | Eurozone Consumer Confidence Dec P | -23 | -24 |