Yen rises strongly in Asian session after BoJ’s surprise announcement of raising 10-year yield cap to 0.50%. Dollar is following closely as second, and then Swiss Franc, on risk aversion. For the same reason, Australian, and New Zealand Dollar are sold off as weakens, followed by Sterling. Canadian and Euro are mixed for now.

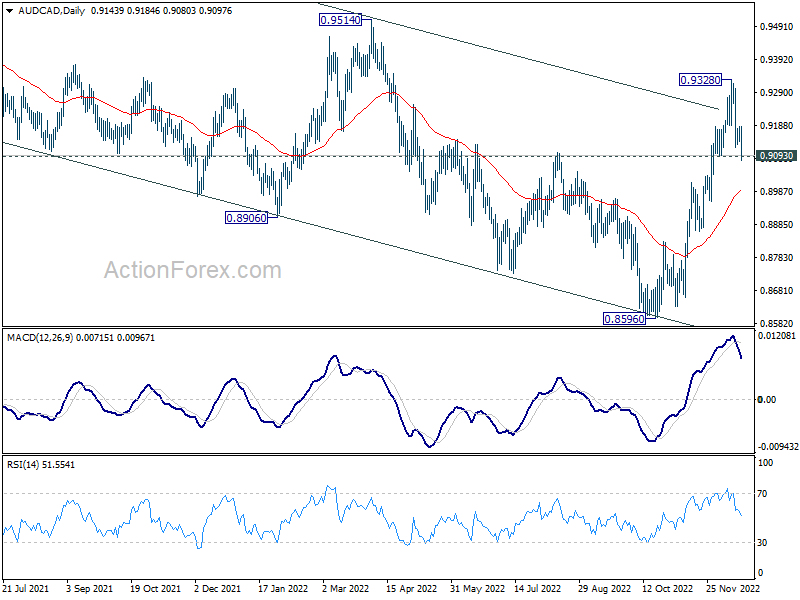

Technically, despite breaking near term falling channel resistance to 0.9328, AUD/CAD quickly retreated back inside the channel. As short term top was probably formed and deeper fall should be seen back to 4 hour 55 EMA (now at 0.8984), and possibly below. The development suggests that Aussie is going to underperform Canadian if rallies in Yen and, to a lesser extent, Dollar intensify.

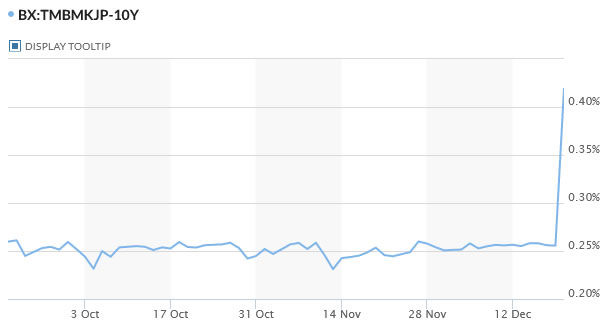

In Asia, at the time of writing, Nikkei is down -2.51%. Hong Kong HSI is down -1.92%. China Shanghai SSE is down -1.35%. Singapore Strait Times is down -0.21%. Japan 10-year JGB yield up sharply by -0.1635 to 0.419. Overnight, DOW dropped -0.49%. S&P 500 dropped -0.90%. NASDAQ dropped -1.49%. 10-year yield rose 0.099 to 3.581.

BoJ tweaks YCC to allow 10-yr yield to rise to 0.50%

BoJ surprises the markets today by widening the band of 10-year JGB yield from 0.25% to 0.50% today. At the same time, short term policy rate is kept unchanged at -0.10% as expected.

Under the yield curve control framework, the central bank will still continue to purchases JGBs without an upper limit to keep 10-year yield at around 0%. But now, the bank will offer to purchase 10-year JGB yields at 0.50% every business day through fixed-rate operations, effectively allowing 10-year yield to rise towards 0.50% level.

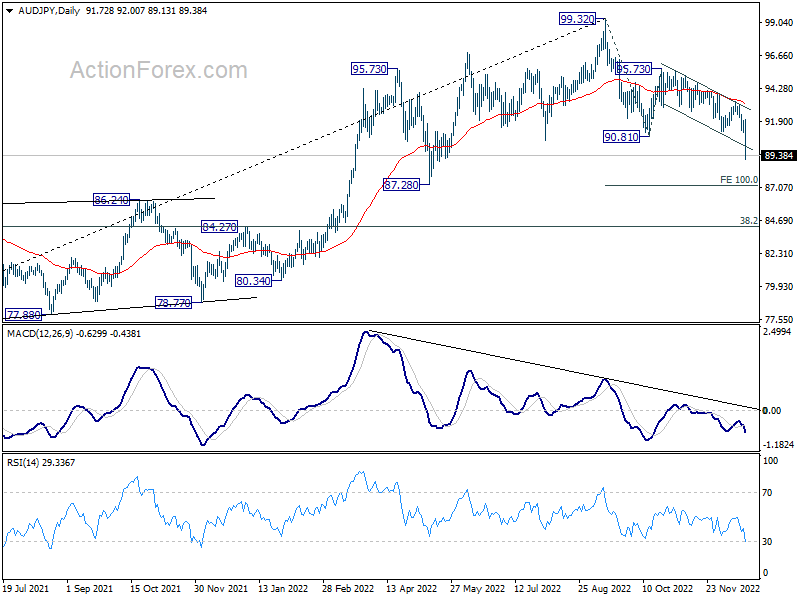

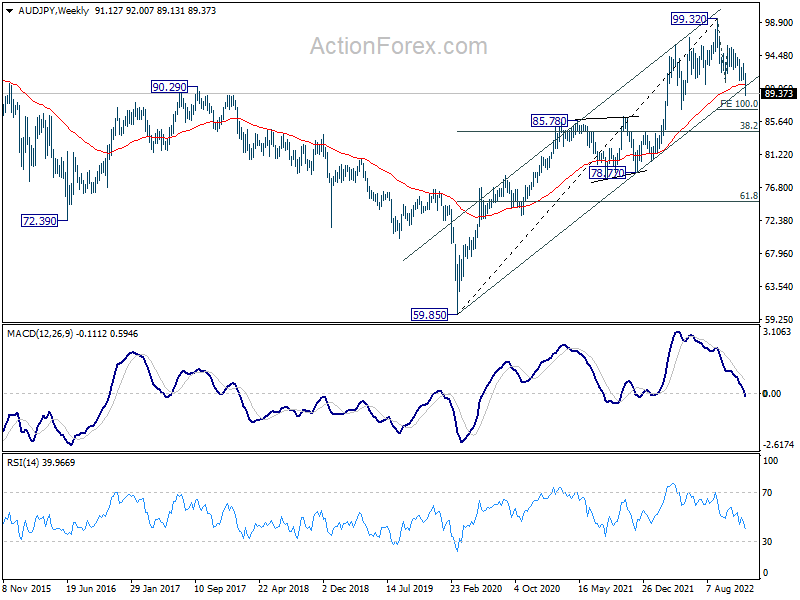

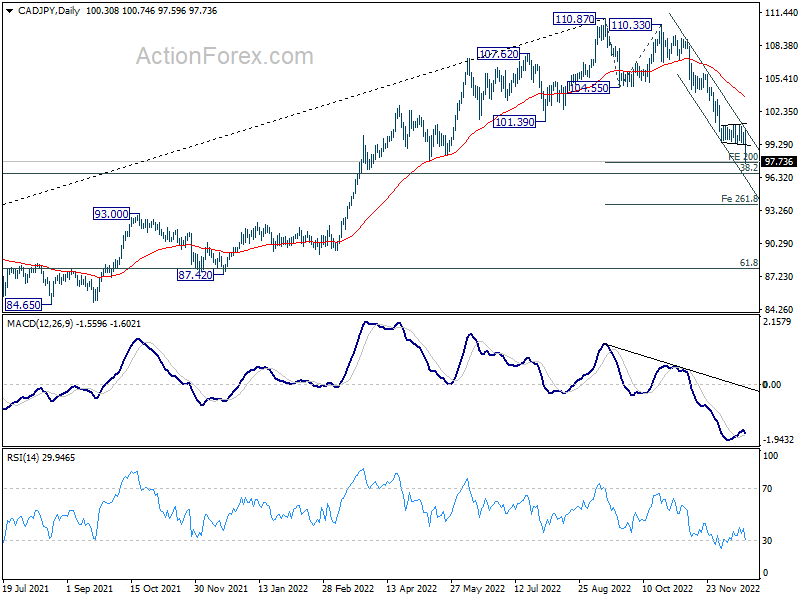

AUD/JPY and CAD/JPY downside breakout after BoJ surprise

Yen surges broadly today after BoJ surprisingly raise 10-year yield cap from 0.25% to 0.50%. AUD/JPY finally breaks through 90.81 support decisively to resume the decline from 99.32. The strong break of a near term channel also indicates downside acceleration. Next near term target is 100% projection of 99.32 to 90.81 from 95.73 at 87.22

From a longer term point of view, the break of 55 week EMA and the channel support also affirms the case that AUD/JPY is corrective whole up trend from 2020 low at 59.85. Such decline from 99.32 would target 38.2% retracement of 59.85 to 99.32 at 84.24 before forming a bottom.

CAD/JPY also broke out of a near term expanding triangle to resume the whole fall from 110.87. Near term target of 200% projection of 110.87 to 104.55 from 110.33 at 97.69 is already met. Such decline is seen the correcting the up trend from 2020 low at 73.80. The question now is whether support from 38.2% retracement of 73.80 to 110.87 at 96.70 is strong enough to contain downside. If now, CAD/JPY accelerate further to 261.8% projection at 93.78.

RBA considered 50bps, 25bps, and no change at Dec meeting

Minutes of RBA’s December 6 meeting indicates that the board has considered three interest rate options of a 50bps hike, a 25bps hike, and no change.

The argument for a 50bps increase stemmed from inflation remains “too high”, and there were factors support a “more pre-emptive action”. For a 25bps increase, the board acknowledged there had bee already a “significant cumulative increase” in interest rates and they would “begin to have more of an effect through the course of 2023″. The arguments for now chance placed”further emphasis of the lagged effect” of prior rate increases.

Board members eventually decided that the case for 25bps increase was the”strongest one”, as further hike was “likely to be necessary”. Members also noted the “importance of acting consistently”.

The minutes also reiterated that “the Board expects to increase interest rates further over the period ahead, but it is not on a pre-set path. Members noted that the size and timing of future interest rate increases would continue to be determined by the incoming data and the Board’s assessment of the outlook for inflation and the labour market.”

NZ ANZ business confidence fell to fresh record low

New Zealand ANZ business confidence declined from -57.1 to -70.2 in December, a new record low. Looking at some details, own activity outlook fell from -13.7 to -25.6. Export intentions dropped form -5.4 to -10.0. Investment intentions dropped form -8.1 to -20.5. Employment intentions dropped from -4.0 to -16.3. Pricing intentions rose from 58.5 to 59.1. Cost expectations declined form 88.7 to 84.4. Inflation expectations dropped from 6.39 to 6.23.

ANZ said: “The fall in business confidence is certainly dramatic, but while it’s at a fresh record low, it would be incorrect to read this as an indication that any recession is likely to be unusually severe. Rather, it’s unusually widely anticipated. It’s a situation unprecedented in recent decades for a central bank to admit it is deliberately engineering a recession.”

Looking ahead

Swiss trade balance, Germany PPI and Eurozone current account will be released in European session. later in the day, Canada will publish retail sales while US building permits and housing starts will be featured.

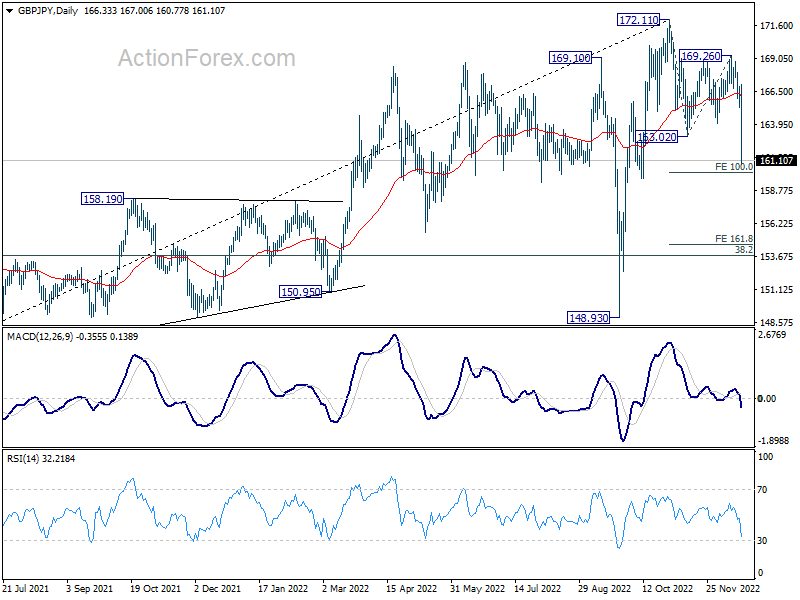

GBP/JPY Daily Outlook

Daily Pivots: (S1) 165.40; (P) 166.15; (R1) 167.09; More…

GBP/JPY’s decline from 172.11 resumed by breaking through 163.02 support decisively. Intraday bias stays on the downside for 100% projection of 172.11 to 163.02 from 169.26 at 160.17. Firm break there will target 161.8% projection at 154.55 next. For now, outlook will stay bearish as long as 164.02 support turned resistance holds, in case of recovery.

In the bigger picture, sustained break of 55 week EMA (now at 161.26) will confirm medium term topping at 172.11, on bearish divergence condition in weekly MACD. Fall from 172.11 should be correcting whole up trend from 123.94 (2020 low). Deeper decline should be seen to 38.2% retracement of 123.94 to 172.11 at 153.70 and possibly below. This will now remain the favored case as long as 55 day EMA (now at 166.11) holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Dec | -70.2 | -57.1 | ||

| 00:30 | AUD | RBA Minutes | ||||

| 03:00 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 07:00 | CHF | Trade Balance (CHF) Nov | 3.27B | 4.14B | ||

| 07:00 | EUR | Germany PPI M/M Nov | -2.60% | -4.20% | ||

| 07:00 | EUR | Germany PPI Y/Y Nov | 30.00% | 34.50% | ||

| 09:00 | EUR | Eurozone Current Account (EUR) Oct | -10.3B | -8.1B | ||

| 13:30 | CAD | Retail Sales M/M Oct | 1.50% | -0.50% | ||

| 13:30 | CAD | Retail Sales ex Autos M/M Oct | 1.30% | -0.70% | ||

| 13:30 | USD | Building Permits Nov | 1.50M | 1.51M | ||

| 13:30 | USD | Housing Starts Nov | 1.40M | 1.43M | ||

| 15:00 | EUR | Eurozone Consumer Confidence Dec P | -23 | -24 |