Dollar rebounds broadly following risk-off sentiment as delayed reaction to Fed’s hawkish projections overnight. SNB, BoE and ECB met expectations with 50bps rate hike. Euro is strong as ECB maintains hawkish bias, with upward revision in inflation projections. Swiss Franc is the third strongest after SNB indicates the possibility of more tightening. Meanwhile, Sterling is notably weaker after somewhat dovish MPC voting. But Aussie and Kiwi are even worse on overall sentiment.

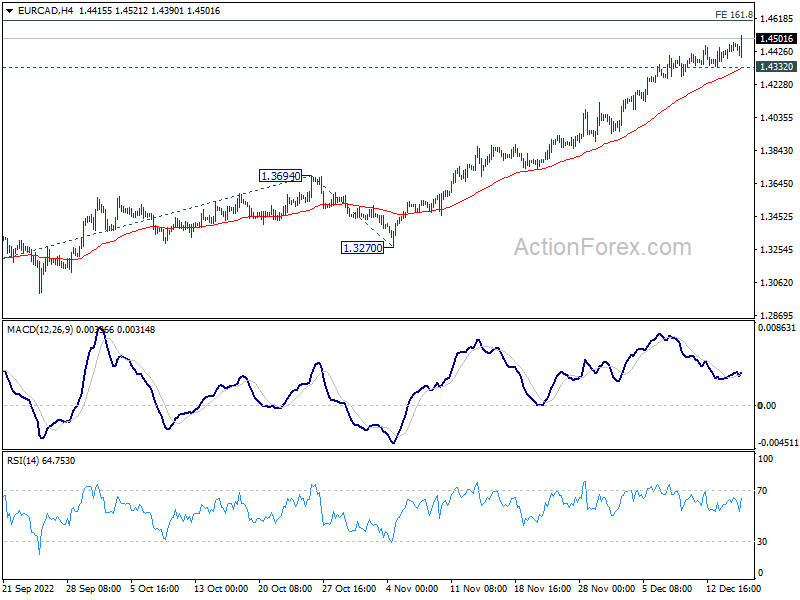

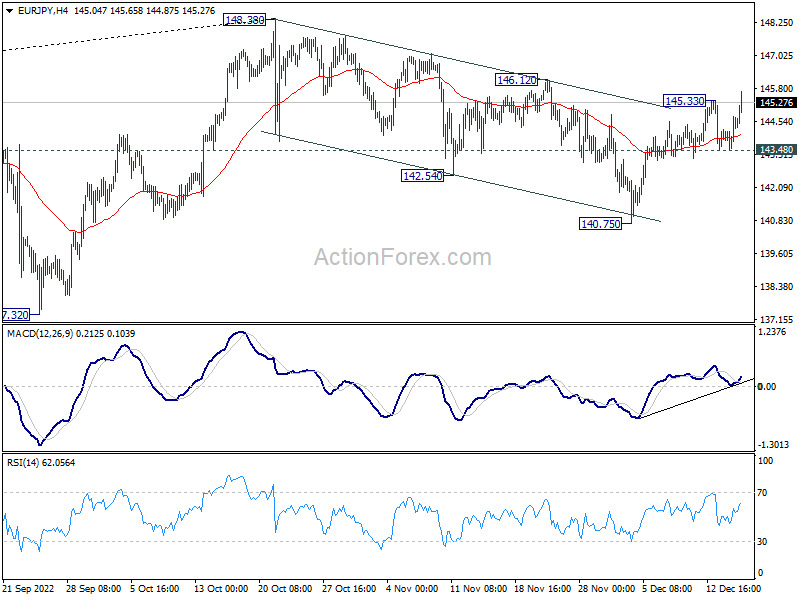

Technically, Euro is making progresses in some crosses with EUR/JPY breaking through 145.33 temporary top. EUR/AUD is on the verge of breaking 1.5747 resistance. EUR/CAD is also extending near term rally. A question now is when EUR/GBP would break through 0.8674 minor resistance to confirm short term bottoming at 0.8545. Euro’s strength in crosses will keep EUR/USD in range.

In Europe, at the time of writing, FTSE is down -0.66%. DAX is down -1.98%. CAC is down -1.87%. Germany 10-year yield is up 0.970 at 2.038. Earlier in Asia, Nikkei dropped -0.37%. Hong Kong HSI dropped -1.55%. China Shanghai SSE dropped -0.25%. Singapore Strait Times dropped -0.15%. Japan 10-year JGB yield dropped -0.0002 at 0.258.

US retail sales down -0.6% mom in Nov, ex-auto sales down -0.2% mom

US retail sales dropped -0.6% mom to USD 689.4B in November, worse than expectation of -0.1% mom. Ex-auto sales dropped -0.2% mom to USD 562.9B, worse than expectation of 0.2% mom rise. Ex-gasoline sales dropped -0.6% mom to USD 625.1B. Ex-auto, ex-gasoline sales dropped -0.2% to USD 498.6B. Total sales for September through November were up 7.7% yoy from the same period a year ago.

Initial jobless claims dropped -20k to 211k in the week ending December 10, smaller than expectation of 230k. Four-week moving average of initial claims dropped -3k to 227k. Continuing claims rose 1k to 1671k in the week ending December 3. Four-week moving average of continuing claims rose 43k to 1625k.

ECB hikes 50bps, expects to raise rates further

ECB raises the three key interest rates by 50bps today as expected. The main refinancing, marginal lending, and deposit rates are 2.50%, 2.75% and 2.00% respectively. The Governing Council expects to “raise them further” based on “substantial upward revision to the inflation outlook”.

Also ECB noted that “keeping interest rates at restrictive levels will over time reduce inflation by dampening demand and will also guard against the risk of a persistent upward shift in inflation expectations.” Future policy decisions will continue to be “data-dependent”, following a “meeting-by-meeting approach”.

Reinvestment under the APP purchases will continue until the end of February 2023. The portfolio will then decline at a “measured and predictable pace” subsequently, amount to EUR 15B per month on average until Q2 2023. Reinvestment under PEPP will continue at least until the end of 2024.

Based on new economic projections, inflation is expected to reach 8.4% in 2022, then fall to 6.3% in 2023, and then 3.4% in 2024, and 2.3% in 2025. Core inflation, excluding energy and food, is projected to be at 3.9% in 2022, 4.2% in 2023, 2.8% in 2024, and then 2.4% in 2025. The economy is projected to grow 3.4% in 2022, 0.5% in 2023, 1.9% in 2024, and then 1.8% in 2025.

BoE hikes 50bps, majority expects further increases

BoE raises Bank Rate by 50bps to 3.50% as expected, by 6-3 vote. Two members, Swati Dhingra and Silvana Tenreyro voted for no change. On the other hand, Catherine Mann voted for 75bps hike.

The “majority” of the MPC judged that “should the economy evolve broadly in line with the November Monetary Policy Report projections, further increases in Bank Rate may be required”.

It’s also reiterated that “The Committee continues to judge that, if the outlook suggests more persistent inflationary pressures, it will respond forcefully, as necessary.”

SNB hikes 50bps to 100%, cannot rule out more

SNB raises the policy rate by 50bps to 1.00% as widely expected, to “countering increased inflation pressure and a further spread of inflation”. The central added that additional rate hikes “cannot be ruled out”. It also maintained the willingness to be “active in the foreign exchange markets as necessary”.

In the new conditional inflation forecast based on 1.0% policy rate, inflation forecasts was lowered from 3.0% to 2.9% in 2022, left unchanged at 2.4% in 2023, and raised from 1.7% to 1.8% in 2024. Inflation forecast was indeed raised from Q3 2023 through Q4 2024.

The highest inflation forecasts was “attributable to stronger inflationary pressure from abroad and the fact that price increases are spreading across the various categories of goods and services in the consumer price index.”

Regarding GDP growth, SNB expects its to be at around 2.0% this year. But weaker overseas demand and higher energy prices are likely to “curb economic activity marked in the coming year”. SNB expects GDP growth to slow to 0.5% in 2023.

SNB Jordan: We will continue to sell foreign currency if appropriate

In the post meeting press conference, SNB Chairman Thomas Jordan said that this year’s 4% appreciation in Swiss Franc exchange rate “has helped ensure that less inflation has been imported from abroad, thus curbing the rise in inflation.”

He said that the central bank sold “foreign currency in recent months” to ensure appropriate monetary conditions. He added, “We will also sell foreign currency in the future if this is appropriate from the monetary policy perspective. Conversely, we remain willing to buy foreign currency again if necessary, i.e. if there were to be excessive appreciation pressure.”

Australia employment grew 64k in Nov, participation rate back at record high

Australia employment grew 64.0k in November, much better than expectation of 19.4k. Unemployment rate was unchanged at 3.4%, matched expectations. Participation rate rose 0.2% to 66.8%. Monthly hours worked dropped -0.4% mom.

Bjorn Jarvis, head of labour statistics at the ABS, said: “The participation rate increased by 0.2 percentage points to 66.8 per cent in November, returning to the record high we saw in June 2022. It was 1.0 percentage point higher than before the pandemic.”

“The record high participation rate continues to show that it is a tight labour market, especially when coupled with very low unemployment.”

Japan continues trade deficit streak for the 16th month

Japan export rose 20.0% yoy to JPY 8838B in November, a record high, led by cars autos and mining machinery shipment to the US. Imports rose 30.3% yoy to JPY 10865B, also a record high, as led by imports of crude oil, coal and LNG.

Trade deficit came in at JPY -2.03T. That the 16th straight month of trade deficit, and the fourth month in a row at the JPY 2T level.

In seasonally adjusted term, exports dropped -1.4% mom to JPY 8787B. Imports dropped -5.3%mom to JPY 10520B. Trade deficit narrowed to JPY -1.73T, versus expectation of JPY -1.24T.

China retail sales down -5.9% yoy in Nov, industrial production up 2.2% yoy

China retail sales contracted -5.9% yoy in November, much worse than expectation of -3.9% mom. Industrial production grew 2.2% yoy, below expectation of 3.4% yoy. Fixed asset investment rose 5.3% ytd yoy, below expectation of 5.6%.

“The consumption market was under pressure in November due to the impact of Covid and other factors, and the decline in market sales widened,” said NBS statistician Fu Jiaqi.

“However, online consumption grew faster, retail sales of basic living goods increased relatively well, some upgraded consumption was higher than overall, and retail businesses such as supermarkets and convenience shops increased steadily.”

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.90; (P) 144.32; (R1) 145.17; More….

EUR/JPY’s rebound from 140.75 resumed after brief retreat and intraday bias is back on the upside. Outlook is unchanged that correction from 148.38 could have completed at 140.75. Break of 146.12 resistance will target a retest on 148.38 high. For now, further rise will remain in favor as long as 143.48 support holds, in case of retreat.

In the bigger picture, considering bearish divergence condition in weekly MACD, 148.38 could be a medium term top already. Fall from there is probably correcting whole up trend from 114.42 (2020 low). Deeper decline would be seen to 55 week EMA (now at 138.08), or further to 38.2% retracement of 114.42 to 148.38 at 135.40 before completion.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | GDP Q/Q Q3 | 2.00% | 0.80% | 1.70% | 1.90% |

| 23:50 | JPY | Trade Balance (JPY) Nov | -1.73T | -1.24T | -2.30T | -2.21T |

| 00:00 | AUD | Consumer Inflation Expectations Dec | 5.20% | 6.00% | ||

| 00:30 | AUD | Employment Change Nov | 64.0K | 19.4K | 32.2K | 43.1K |

| 00:30 | AUD | Unemployment Rate Nov | 3.40% | 3.40% | 3.40% | |

| 02:00 | CNY | Industrial Production Y/Y Nov | 2.20% | 3.40% | 5.00% | |

| 02:00 | CNY | Retail Sales Y/Y Nov | -5.90% | -3.90% | -0.50% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Nov | 5.30% | 5.60% | 5.80% | |

| 04:30 | JPY | Tertiary Industry Index M/M Oct | 0.20% | 0.40% | -0.40% | |

| 08:30 | CHF | SNB Interest Rate Decision | 1.00% | 1.00% | 0.50% | |

| 09:00 | CHF | SNB Press Conference | ||||

| 12:00 | GBP | BoE Interest Rate Decision | 3.50% | 3.50% | 3.00% | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 7–0–2 | 9–0–0 | 9–0–0 | |

| 13:15 | CAD | Housing Starts Nov | 264K | 255K | 267K | 265K |

| 13:15 | EUR | ECB Main Refinancing Rate | 2.50% | 2.50% | 2.00% | |

| 13:30 | USD | Initial Jobless Claims (Dec 9) | 211K | 230K | 230K | 231K |

| 13:30 | USD | Retail Sales M/M Nov | -0.60% | -0.10% | 1.30% | |

| 13:30 | USD | Retail Sales ex Autos M/M Nov | -0.20% | 0.20% | 1.30% | |

| 13:30 | USD | Empire State Manufacturing Index Dec | -11.2 | -0.2 | 4.5 | |

| 13:30 | USD | Philadelphia Fed Manufacturing Survey Dec | -13.8 | -11.3 | -19.4 | |

| 13:45 | EUR | ECB Press Conference | ||||

| 14:15 | USD | Industrial Production M/M Nov | 0.10% | -0.10% | ||

| 14:15 | USD | Capacity Utilization Nov | 79.80% | 79.90% | ||

| 15:00 | USD | Business Inventories Oct | 0.40% | 0.40% | ||

| 15:30 | USD | Natural Gas Storage | -39B | -21B |