Dollar is trying to recover in early US session, with help from 10-year yield which reclaims 3.5% handle. Yet again there is now clear follow through buying. News flow is slow today, without much surprise from US PPI data. As Fed is already in a blackout period, there is no comment from US monetary policy makers. Trading would likely remain subdued, until FOMC rate decision and economic projections next week.

In Europe, at the time of writing, FTSE is down -0.10%. DAX is up 0.31%. CAC is up 0.01%. Germany 10-year yield is up 0.0683 at 1.886. Earlier in Asia, Nikkei rose 1.18%. Hong Kong HSI rose 2.32%. China Shanghai SSE rose 0.30%. Singapore Strait Times rose 0.31%. Japan 10-year JGB yield dropped -0.0006 to 0.256.

US PPI up 0.3% mom, 7.4% yoy in Nov

US PPI for final demand rose 0.3% mom in November, above expectation of 0.1% mom. PPI services rose 0.4% mom while PPI goods rose 0.1% mom. PPI less foods, energy, and trade services rose 0.3% mom.

For the 12 months ended in November, PPI rose 7.4% yoy, down from October’s 8.1% yoy, matched expectations. PPI less foods, energy, and trade services rose 4.9% yoy,

China CPI slowed to 1.6% yoy in Nov, core CPI down -0.6% yoy

China CPI slowed from 2.1% yoy to 1.6% yoy in November, below expectation of 1.7% yoy. Core CPI, excluding food and energy, was down -0.6% yoy, unchanged from October. Food prices slowed from 7.0% yoy to 3.7% yoy. Non-food prices were unchanged at 1.1% yoy.

“In November, due to the domestic epidemic, seasonal factors, and a higher base of comparison in the same period last year, CPI turned from rising to falling month on month and fell back year on year,” said chief NBS statistician Dong Lijuan.

PPI was unchanged at -1.3% yoy, above expectation of -1.5% yoy. “In November, PPI rose slightly month on month as a result of price increases in coal, oil and non-ferrous metals, and continued to fall year on year due to a high base of comparison from the same period last year,” added Dong.

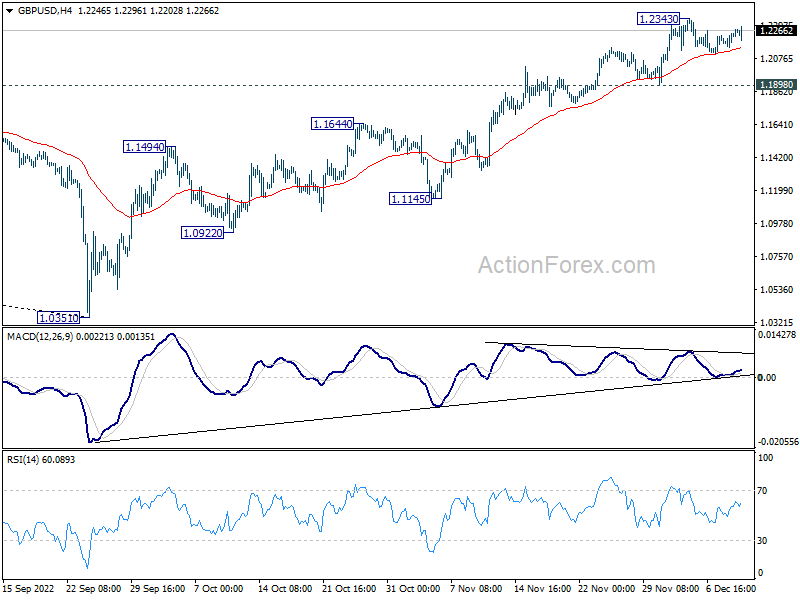

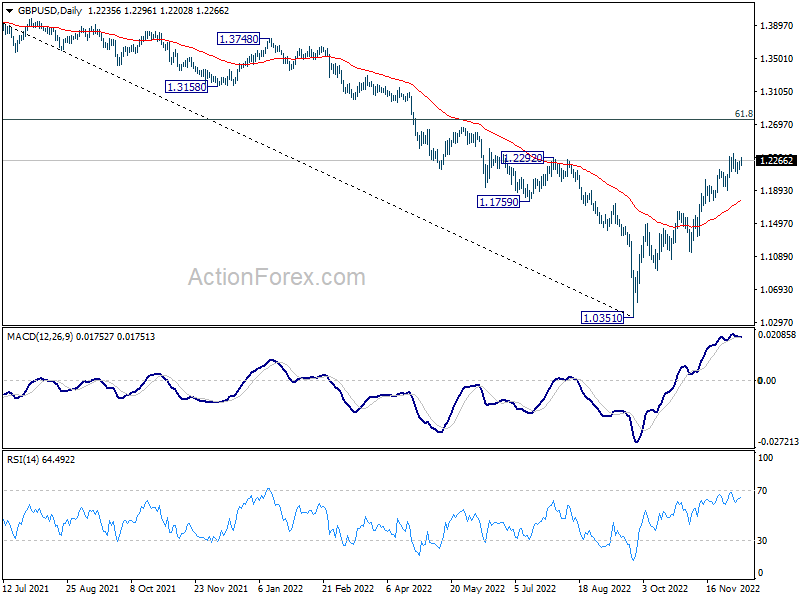

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2178; (P) 1.2213; (R1) 1.2271; More…

Intraday bias in GBP/USD remains neutral. Consolidation from 1.2343 could extend. But further rise remains mildly in favor as long as 1.1898 support holds. On the upside, break of 1.2343 will resume the rally from 1.0351 and target 1.2759 medium term fibonacci level next. However, firm break of 1.1898 support will confirm short term topping and turn bias back to the downside.

In the bigger picture, rise from 1.0351 medium term bottom is at least correcting whole down trend from 1.4248 (2021 high). Further rise is expected as long as 1.1644 resistance turned support holds. Next target is 61.8% retracement of 1.4248 to 1.0351 at 1.2759. Sustained break there will pave the way back to 1.4248.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Nov | 3.10% | 3.00% | 3.10% | |

| 01:30 | CNY | CPI Y/Y Nov | 1.60% | 1.70% | 2.10% | |

| 01:30 | CNY | PPI Y/Y Nov | -1.30% | -1.50% | -1.30% | |

| 13:30 | CAD | Capacity Utilization Q3 | 82.60% | 83.00% | 83.80% | 82.80% |

| 13:30 | USD | PPI M/M Nov | 0.30% | 0.10% | 0.20% | 0.30% |

| 13:30 | USD | PPI Y/Y Nov | 7.40% | 7.40% | 8.00% | 8.10% |

| 13:30 | USD | PPI Core M/M Nov | 0.40% | 0.30% | 0.00% | 0.10% |

| 13:30 | USD | PPI Core Y/Y Nov | 6.20% | 6.00% | 6.70% | |

| 15:00 | USD | Michigan Consumer Sentiment Index Dec P | 53.3 | 56.8 | ||

| 15:00 | USD | Wholesale Inventories Oct F | 0.80% | 0.80% |