The tone of the markets was well set by Fed Chair Jerome Powell’s indication of smaller rate hike in the upcoming FOMC meeting. The biggest reactions were found in treasury yields, which decline was surprisingly steep. US stocks ended higher but upside momentum appeared to be diminishing.

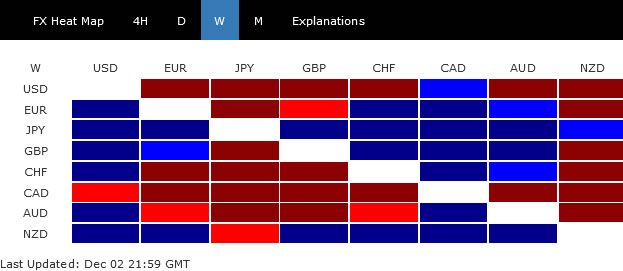

Dollar was sold off broadly and closed as the second worst performer, next to Canadian. Australian Dollar was actually the third weakest, arguing that risk-on sentiment wasn’t that solid. Yen was the strongest, as supported by falling yields, followed by Kiwi and then Sterling. Euro and Swiss Franc ended mixed.

Investors cheered Powell, but turning cautious

Fed Chair Jerome Powell’s speech at the Brookings Institution was the biggest market mover last week, and pretty much set the tone. In short, Powell said that, “it makes sense to moderate the pace of our rate increases as we approach the level of restraint that will be sufficient to bring inflation down”, adding that, the time for moderating the pace of rate increases may come as soon as the December meeting.” Stocks rose while treasury yield and Dollar tumbled as reactions to the speech. Solid non-farm payroll growth with stronger wage increases provided some jitters, but didn’t alter the path.

The decline in treasury yields at the long end was rather decisive and significant. But momentum in stocks and Dollar was not. As pointed out by many Fed officials, at this stage of the tightening cycle, it’s not the size of a move that matters. Rather, the terminal rate and the timing to get there carry much more significance. Thus, traders might start to turn cautious and wait for new economic projections at the FOMC meeting on December 15 to get some hints on the answers to the two questions, before taking another committed move.

DOW’s close above 34281.36 resistance was a bullish development. But upside momentum is clearly diminishing as seen in daily MACD. There is still prospect of a pull back in the near term, and bring of 33583.77 support will indicate the start of a correction. But as long as 33583.77 holds, DOW could still edge higher before making a near term top.

S&P 500’s rebound from 3491.58 is much less convincing that DOW’s corresponding move. SPX is still kept well below 4325.28 resistance. Indeed, break of 3906.54 support should have 55 day EMA taken out too, and would open up the case for retesting 3491.58 low.

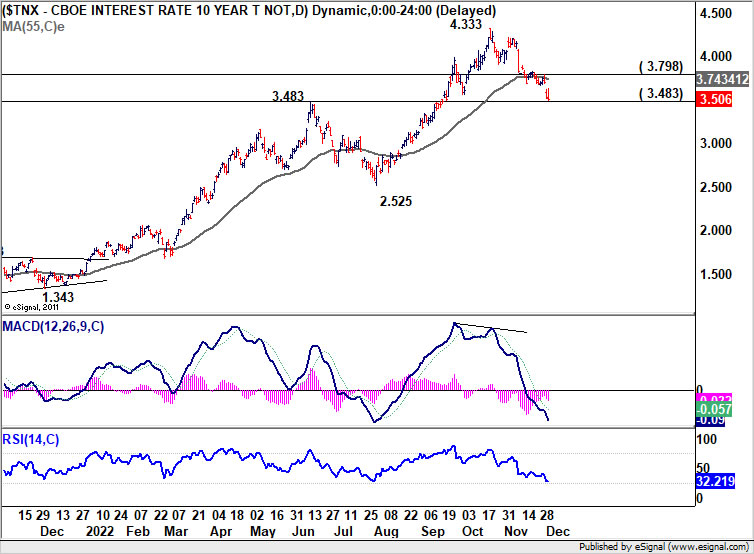

10-year yield to defend key support level

US 10-year yield’s steep decline was a surprise. The move away from 55 day EMA is starting the argue that it’s already in a medium term correction. Still, rebound from current level will have 3.483 resistance turned support defended. Break of 3.798 resistance will bring stronger rise back towards 4.333 high, and keep the correction short term.

However, sustained break of 3.483 will extend the fall from 4.333 to 55 week EMA (now at 2.897), or even further to 38.2% retracement of 0.398 to 4.333 at 2.829. Such development would be an heavy drag on all Yen pairs, in particular USD/JPY.

Dollar index sitting on important support zone

Dollar index’s close below 38.2% retracement of 89.20 to 114.77 at 105.00 is a bearish sign. Yet, it’s still sitting close to an important support zone between 104.63 and 55 week EMA (now at 104.00). There is still prospect of forming a bottoming at current level. Break of 107.19 resistance should at least bring rebound back to 55 day EMA (now at 108.62).

However, sustained trading below the 55 day EMA will open up deeper correction to 61.8% retracement at 98.96, which is below 100 handle. If that happens, we might at extended rally in stocks and correction in yields at the same time.

Yen surged broadly, boosted by falling yields

Yen was the biggest winner for the week as lifted by the steep decline in US and European benchmark yields. There was also some support from new board member Naoki Tamura’s push for policy framework review, which could eventually lead to an end of the ultra-loose monetary policy (well, perhaps next year).

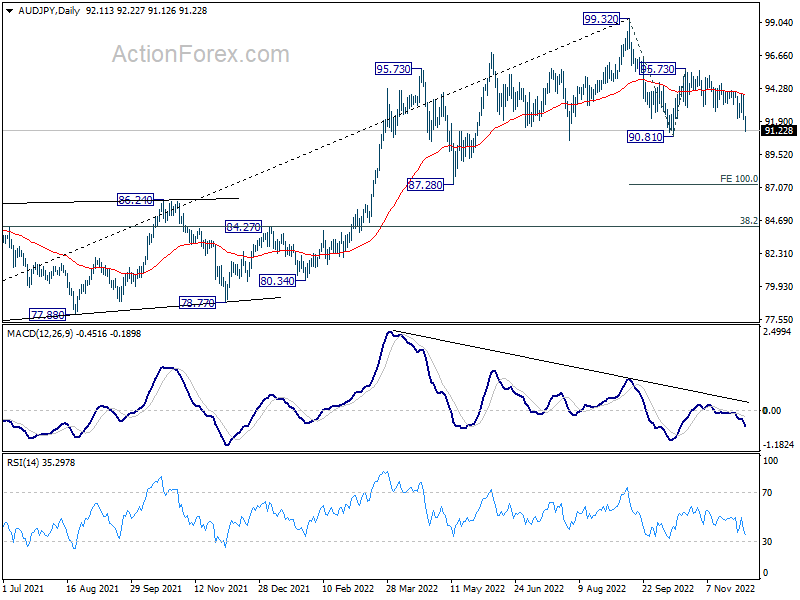

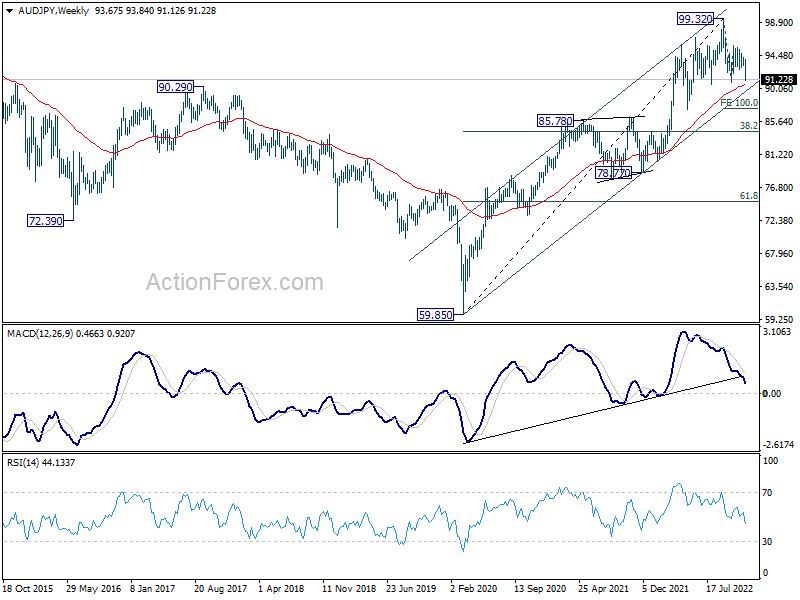

After some hesitation, AUD/JPY’s near term decline finally took off and further fall should be seen to retest 90.81 support soon. Firm break there will resume the decline fall from 99.32, as a correction to larger up trend. Next target will be 100% projection of 99.32 to 90.81 from 95.73 at 87.22.

Also, if that happens, 55 week EMA would likely be taken out decisively, which would indicate that AUD/JPY is already correcting the rise form 59.85 (2020 low). That would open up further decline to 38.2% retracement of 59.85 to 99.32 at 84.24.

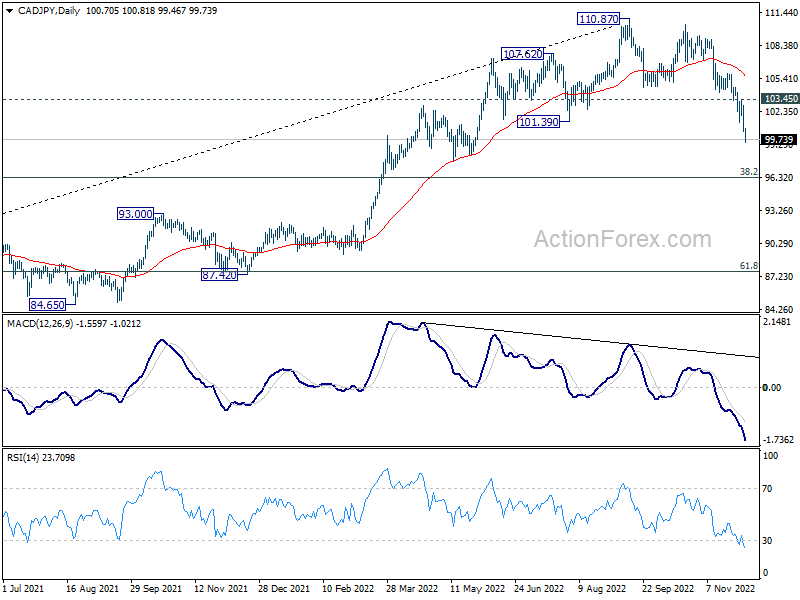

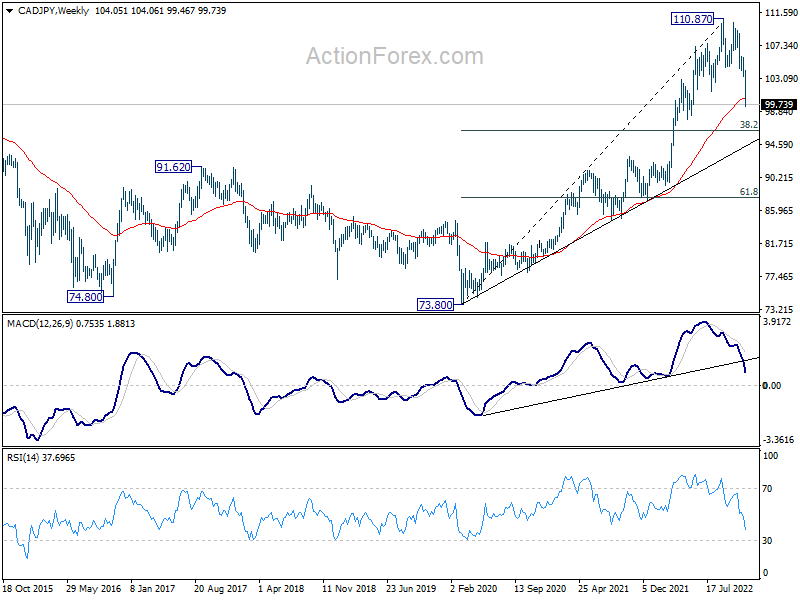

CAD/JPY’s development was even more bearish, with a close below 55 week EMA (now at 100.45). It’s likely already in correction to whole up trend from 73.80 (2020 low). Deeper decline is expected as long as 103.45 resistance holds. Next target is 38.2% retracement of 73.80 to 110.87 at 96.70.

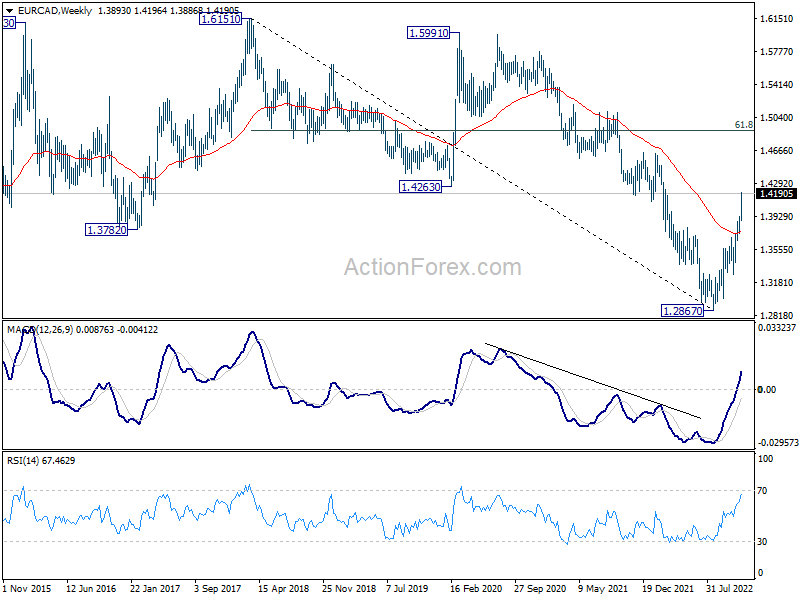

Loonie selloff accelerates as BoC tightening close to a pause

Taking about Canadian Dollar, it ended as the worst performer last week on talks that BoC could pause earlier than Fed which leave its terminal rate lower. Opinions are divided on whether BoC would raise interest rate by 25bps or 50bps this week. Yet, there is consensus that this hike, or another one in January, would be the end of the cycle.

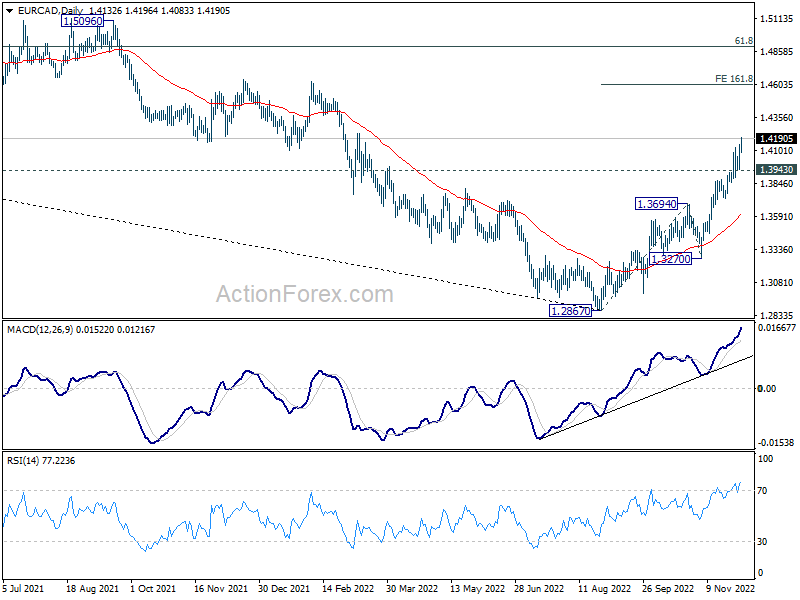

EUR/CAD’s rally accelerated to as high as 1.4196 last week and there is not sign of topping yet. Further rally is expected as long as 1.3943 support holds. Next target is 161.8% projection of 1.2867 to 1.3694 from 1.3270 at 1.4608.

Also, note that sustained break of 1.4263 support turned resistance should confirm the completion of whole down trend from 1.6151 (2018 high), with three waves down to 1.2867 (2022 low). Further rally should be seen to 61.8% retracement of 1.6151 to 1.2867 at 1.4897 and above in the medium term.

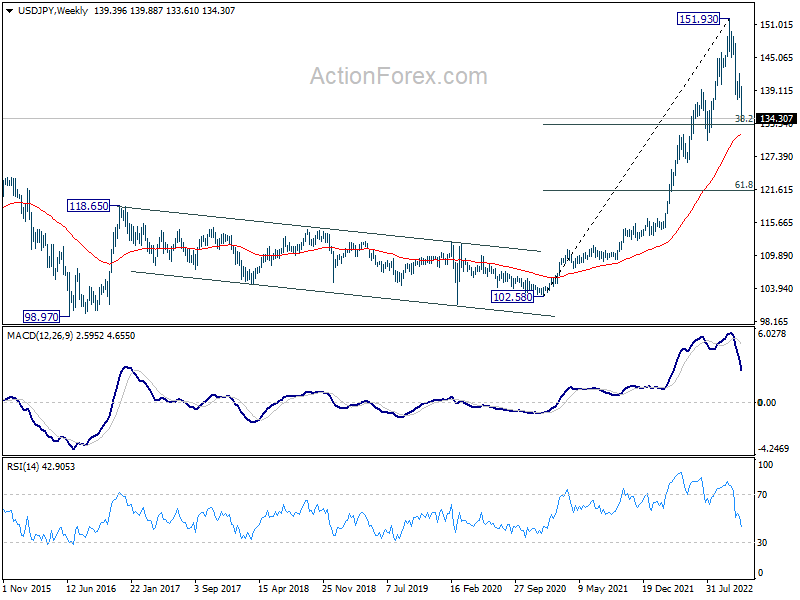

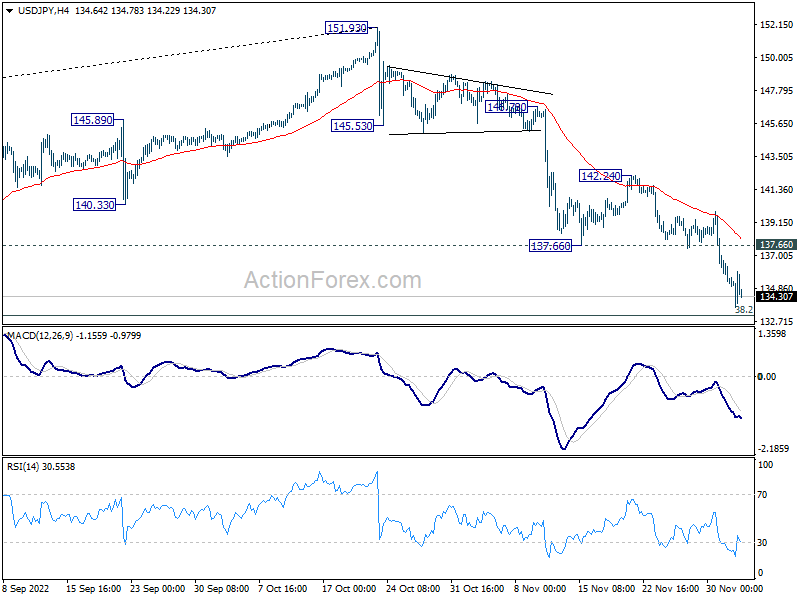

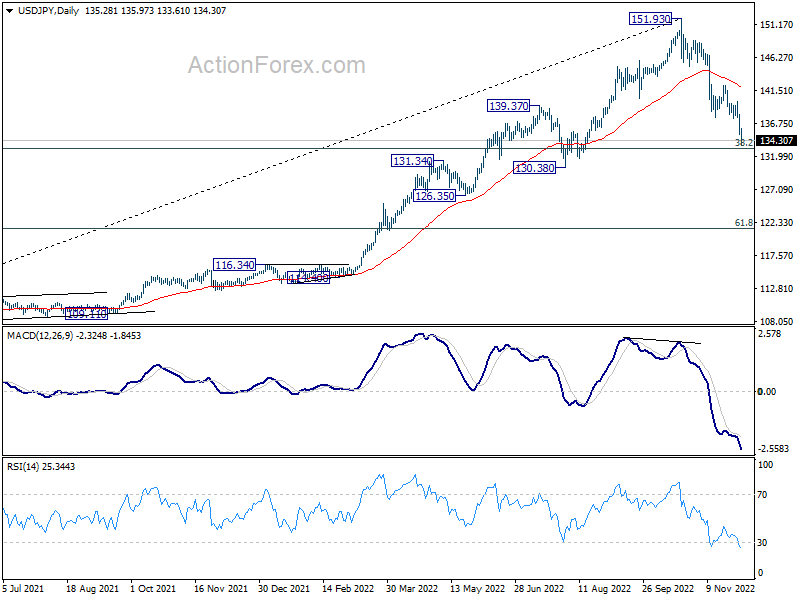

USD/JPY Weekly Outlook

USD/JPY’s fall from 151.93 resumed last week and hit as low as 133.61. Initial bias stays on the downside this week for 133.07 medium term fibonacci level or further to 55 week EMA. On the upside, break of 137.66 support turned resistance will turn intraday bias neutral first. However, near term risk will stay on the downside as long as 142.24 resistance holds, even in case of recovery.

In the bigger picture, a medium term top should be formed at 151.93. Fall from there is correcting larger up trend from 102.58. It’s too early to call for bearish trend reversal. But even as a corrective move, such decline should target 38.2% retracement of 102.58 to 151.93 at 133.07, or further to 55 week EMA (now at 131.33). Some support should be seen around this zone to bring rebound. However, sustained break of 55 week EMA will pave the way to 61.8% retracement at 121.43.

In the long term picture, rise from 102.58, as part of the up trend from 75.56 (2011 low) was put to a halt at 151.93, just ahead of 100% projection of 75.56 to 125.85 from 102.58 at 152.87. There is no clear sign of long term reversal yet. Such up trend is expected to resume at a later stage, as long as 125.85 resistance turned support holds.