Dollar is on the strong side in quiet trading in Asia, together with Yen and Swiss Franc. But the greenback is just staying in familiar range against. On the other hand, Euro and Sterling are the softer ones. Aussie is also trading with an undertone after mixed job data. But overall, most major pairs and crosses in the forex markets are still stuck inside last week’s range for now.

Technically, attention will be on whether Dollar could break through near term resistance levels before the week ends. The levels include 1.2002 support in GBP/USD, 0.6868 support in AUD/USD, 135.57 resistance in USD/JPY, and 1.2984 resistance in USD/CAD.

In Asia, at the time of writing, Nikkei is down -0.85%. Hong Kong HSI is down -0.54%. China Shanghai SSE is down -0.46%. Singapore Strait Times is up 0.50%. Japan 10-year JGB yield is up 0.0079 at 0.194. Overnight, DOW dropped -0.50%. S&P 500 dropped -0.72%. NASDAQ dropped -1.25%. 10-year yield rose 0.069 to 2.893.

Australia lost -40.9k jobs, but unemployment rate dropped to 3.4%

Australia employment contracted -40.9k in July, much worse than expectation of 25.0k growth. Full time jobs decreased by 86.9k while part time jobs rose 46k.

Unemployment rate dropped from 3.5% to 3.4%. Participation rate dropped notably from 66.8% to 55.4%. Monthly hours worked in all jobs dropped -16m hours, or -0.8% mom.

“The fall in unemployment in July reflects an increasingly tight labour market, including high job vacancies and ongoing labour shortages, resulting in the lowest unemployment rate since August 1974,” Bjorn Jarvis, head of labour statistics at the ABS, said.

RBNZ Orr: Monetary policy was too loose for a period

RBNZ Governor Adrian Orr told a parliamentary committee, “our core inflation is too high and that suggests at some point monetary policy was too loose for a period.”

“I have already apologized for the current level of inflation. I have already said that the Reserve Bank was party to that,” he added.

However, “the worst mistake we could be having would be fighting deflation, unnecessary unemployment and economic collapse,” he said. “We have ended up with the better problem — but it is a problem — which is inflation, core inflation of 4-6% that we need to put back in the bottle.”

Looking ahead

Swiss trade balance and Eurozone CPI final will be released in European session. Later in the day, Canada will release IPPI and RMPI. US will release jobless claims, Philly Fed survey and existing home sales.

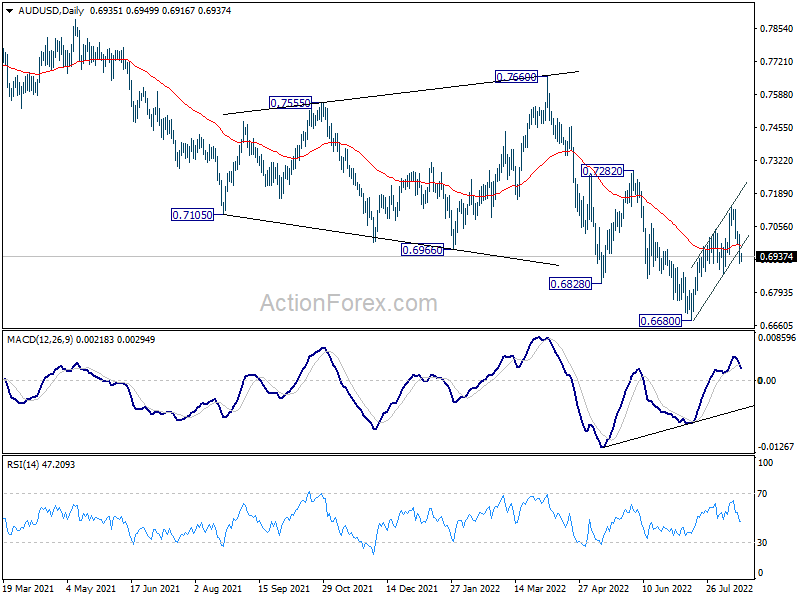

AUD/USD Daily Report

Daily Pivots: (S1) 0.6889; (P) 0.6959; (R1) 0.7008; More…

AUD/USD’s fall from 0.7135 is still in progress and intraday bias stays mildly on the downside for 0.6868 support. Firm break there argue that whole rebound from 0.6680 is finished, and bring retest of 0.6680 low. On the upside, above 0.7030 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 0.8006 (2021 high) is seen more as a corrective pattern to rise from 0.5506 (2020 low). Or it could be a bearish impulsive move. In either case, outlook will remain bearish as long as 0.7282 resistance holds. Next target is 61.8% retracement of 0.5506 to 0.8006 at 0.6461.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Employment Change Jul | -40.9K | 25.0K | 88.4K | |

| 01:30 | AUD | Unemployment Rate Jul | 3.40% | 3.50% | 3.50% | |

| 06:00 | CHF | Trade Balance (CHF) Jul | 3.55B | 3.80B | ||

| 09:00 | EUR | Eurozone CPI Y/Y Jul F | 8.90% | 8.90% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Jul F | 4.00% | 4.00% | ||

| 12:30 | CAD | Industrial Product Price M/M Jul | -1.10% | |||

| 12:30 | CAD | Raw Material Price Index Jul | -0.10% | |||

| 12:30 | USD | Initial Jobless Claims (Aug 12) | 261K | 262K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Aug | -6.2 | -12.3 | ||

| 14:00 | USD | Existing Home Sales Jul | 4.85M | 5.12M | ||

| 14:30 | USD | Natural Gas Storage | 38B | 44B |