Commodity currencies soften mildly in Asian session today, following weaker than expected economic data from China. On the other hand, Yen is leading Dollar and Swiss Franc higher. Euro and Sterling are mixed for now. Overall sentiment is mixed, with notable gains in Nikkei but other Asian indexes are sluggish. Gold is still struggling to break away from 1800 handle. WTI crude oil is dipping below 92 handle.

Technically, one focus today is one whether buying in Yen would pick up momentum again. One level to watch is AUD/JPY’s reaction to 93.46 minor support in case of deeper retreat. More too look at include 135.63 minor support in EUR/JPY and 161.08 minor support in GBP/JPY. Break of these levels would argue that Yen bulls are back on board.

In Asia, at the time of writing, Nikkei is up 1.14%. Hong Kong HSI is down -0.08%. China Shanghai SSE is up 0.15%. Singapore Strait Times is down -0.22%. Japan 10-year JGB yield is down -0.0021 at 0.187.

Japan GDP grew 0.5% qoq in Q2, exceeding pre-pandemic level finally

Japan GDP grew 0.5% qoq in Q2, below expectation of 0.6% qoq. In annualized term, GDP grew 2.2%, below expectation of 2.5%. The size of the economy was lifted to JPY 542.1T, exceeding pre-pandemic level in Q4 2019.

Growth was driven by 1.1% gain in private consumption. Capital expenditure rose 1.4%. Public investment rose 0.9%. Exports and imports rose 0.9% and 0.7% respectively.

China data disappoints, PBoC cuts MLF rate

China industrial production rose 3.8% yoy in July, below expectation of 4.6% yoy, slowed from 3.9% yoy. Retail sales rose 2.7% yoy, below expectation of 5.0% yoy, slowed from 3.1% yoy. Fixed asset investment rose 5.7% ytd yoy, below expectation of 6.2%.

“The national economy maintained strong recovery momentum,” the NBS said in a statement. But it warned of rising stagflation risks globally and said “the foundation for the recovery of the domestic economy has yet to be consolidated.”

Separately, PBoC cut a key interest rate for the second time this year and withdrew some cash from the banking system on Monday The rate on one-year medium-term lending facility (MLF) loans is lowed by 10 bps to 2.75%. The PBOC attributed its move to “keep banking system liquidity reasonably ample”.

NZ BusinessNZ services dropped to 51.2, back below average

New Zealand BusinessNZ Performance of Services Index dropped from 54.7 to 51.2 in July. Activity/Sales dropped from 55.8 to 54.4. Employment dropped from 52.7 to 49.2.New orders/business dropped from 60.5 to 52.5. Stocks/inventories dropped from 54.0 to 53.1. Supplier deliveries dropped from 48.4 to 47.3.

BNZ Senior Economist Doug Steel said that “it is difficult to be sure from one month’s data, but July’s outcome is the lowest since February, has retreated further from the recent 54.9 peak set in May, and is back below average.”

RBNZ to hike 50bps, and lots of data featured

RBNZ is expected to raise the Official Cash Rate by another 50bps to 3.00% this week. Tightening bias should be maintained based on the May’s projected path for interest rate. The question is whether RBNZ would signal that “front-loading” of rate hike is complete, giving that interest rate is in restrictive region. That is, the pace of tightening would be back on data-dependent mode. In terms of central bank activities, RBA and Fed will release minutes.

Economic calendar is very busy this week, with particular focus on US retail sales. Eurozone ZEW economic sentiment is another focus. Also, UK will publish employment, CPI and retail sales. Moreover, Canada CPI, Australia employment and a batch of China data could also be market moving.

Here are some highlights for the week:

- Monday: Japan GDP; China retail sales, industrial production, fixed asset investment; Swiss PPI; Canada manufacturing sales, wholesale sales; US Empire State manufacturing, NAHB housing index.

- Tuesday: RBA minutes; Japan tertiary industry index; UK employment; Eurozone trade balance; German ZEW; Canada CPI, housing starts; US housing starts and building permits, industrial production.

- Wednesday: RBNZ rate decision; Australia wage price index; Japan trade balance, machine orders; UK CPI, PPI; Eurozone employment, GDP; US retail sales, business inventories, FOMC minutes.

- Thursday: Australia employment; Swiss Trade balance; Eurozone CPI final; Canada IPPI and RMPI; US Philly Fed survey, jobless claims, existing home sales.

- Friday: New Zealand trade balance; Japan CPI; Germany PPI; UK Gfk consumer confidence, retail sales; Eurozone current account; Canada retail sales.

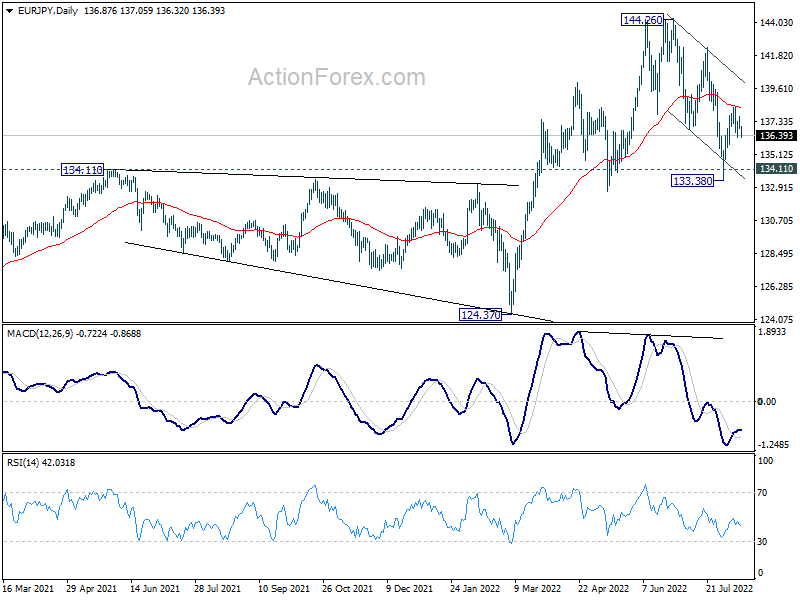

EUR/JPY Daily Outlook

Daily Pivots: (S1) 136.60; (P) 137.00; (R1) 137.70; More….

Intraday bias in EUR/JPY remains neutral for the moment. On the upside, break of 138.38, and sustained trading above 55 day EMA (now at 138.29) will suggest that whole correction from 144.26 has completed. Further rally would then be seen back to retest 144.26 high. However, break of 135.63 will turn bias back to the downside for 133.38 low instead.

In the bigger picture, up trend from 114.42 (2020 low) is seen as the third leg of the pattern from 109.30 (2016 low). Further rally is in favor as long as 134.11 resistance turned support holds, even in case of deep pull back. Next target is 149.76 (2015 high). However, sustained break of 134.11 will be a sign of medium term bearish reversal and turn focus to 124.37 support for confirmation.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | Rightmove House Price Index M/M Aug | -1.30% | 0.40% | ||

| 23:50 | JPY | GDP Q/Q Q2 P | 0.50% | 0.60% | -0.10% | |

| 23:50 | JPY | GDP Deflator Y/Y Q2 P | -0.40% | -0.80% | -0.50% | |

| 02:00 | CNY | Retail Sales Y/Y Jul | 2.70% | 5.00% | 3.10% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Jul | 5.70% | 6.20% | 6.10% | |

| 02:00 | CNY | Industrial Production Y/Y Jul | 3.80% | 4.60% | 3.90% | |

| 04:30 | JPY | Industrial Production M/M Jun F | 9.20% | -7.50% | -7.50% | |

| 06:30 | CHF | Producer and Import Prices M/M Jul | 0.40% | 0.30% | ||

| 06:30 | CHF | Producer and Import Prices Y/Y Jul | 6.70% | 6.90% | ||

| 12:30 | CAD | Manufacturing Sales M/M Jun | -2.00% | |||

| 12:30 | CAD | Wholesale Sales M/M Jun | 1.60% | |||

| 12:30 | USD | Empire State Manufacturing Index Aug | 5.1 | 11.1 | ||

| 14:00 | USD | NAHB Housing Market Index Aug | 55 | 55 |