The US retail sales were anticipated today along with the Univ. of Michigan consumer sentiment. Recall from last month, the sharp fall in consumer sentiment was a catalyst for the Fed to hike by 75 basis points as concerns about inflation threatened the growth prospects in the economy..

For retail sales, after stronger than expected CPI this week, a runaway report could tilt the markets and the Fed to a 100 basis point hike at their July 27 meeting.

The retail sales did come out at 1.0% vs 0.8% with the control group up 0.8% vs 0.3% est, but there was a revision to that measure to -0.3% vs 0.0% last month which took out some of the sting of the increase

Later before the stock open, the industrial production and capacity utilization came out weaker which helped to quell any concerns about overheating growth.

Fed officials also allayed fears of a 100 basis point hike. Bostic, who earlier this week did not rule out 100 basis points, softened his tone saying moving “too dramatically” could undermine the economy. Fed’s Bullard did raise his projection for the end of year to 3.75% from 3.5%, but said he would defer to the committee on whether 75 or 100 is warranted. Later Fed’s Daly said the Fed is working to get inflation down without stalling the economy.

As far as the Univ. of Michigan sentiment, it rebounded from the low last month and perhaps more importantly showed lower inflation expectations 1 and 5 years forward.

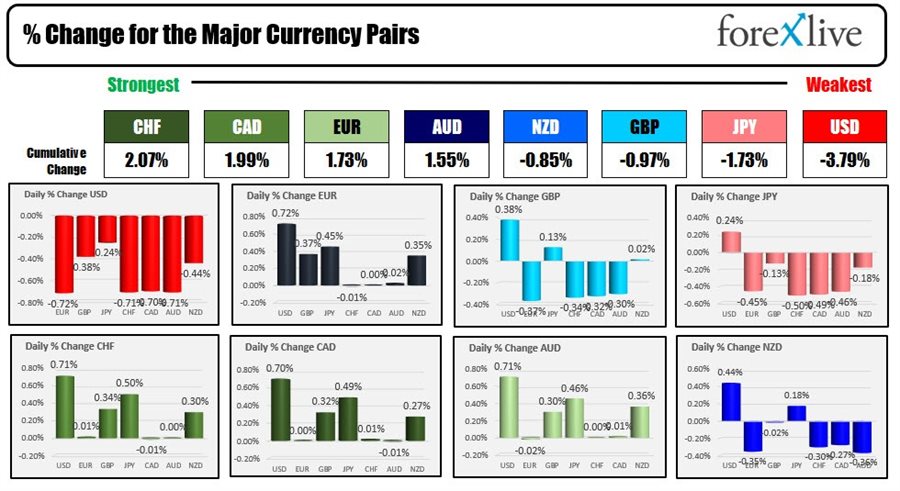

That paved the way for some risk on flows into stocks, and a lower USD as well. US yields moved modestly lower. The greenback moved lower as well, and is ending the day as the weakest of the majors, while the CHF is the strongest.

Looking at the stock indices, the:

- Dow industrial average rose 658.08 points or 2.15% to 31288.26

- S&P index rose 72.8 points or 1.92% to 3863.17

- NASDAQ index rose 201.25 points or 1.79% to 11452.43

- Russell 2000 rose 36.86 points or 2.16% to 1744.37

For the trading week, the gains today did not erase declines, but they did lessen the pain from the moves lower. Stocks were also helped by better-than-expected earnings and Citicorp which helped to send all financials higher today. The financial sector was the largest gainer today in the S&P with a gain of 3.5% on the day (all 11 sectors of the S&P rose today).

For the trading week:

- Dow industrial average fell -0.17%

- S&P index fell -0.99%

- NASDAQ index fell -1.56%

Although lower for the week, things could have been much worse.

In other markets to end the week:

- Spot gold is trading down $-3.37 -0.20% at $1706.70

- spot silver is trading up $0.25 or 1.39% at $18.68

- crude oil rose $1.82 to $97.60

- the price bitcoin also moved higher in reaction to the risk on flows is trading just below the $21,000 level at $20,929

In the US debt market today, yields moved modestly lower.

- 2 year yield is trading at 3.13%, -0.8 basis points. The high yield reached 3.269% this week

- 5 year yield is at 3.046%, -2.3 basis points. It’s high yield this week reached 3.154% for rotating back to the downside

- 10 year yield is at 2.924% down -4.1 basis point, with a high yield this week at 3.071%

- 30 year is trading at 3.083%, -2.6 basis points. It’s high yield reached 3.228%.

The 2-10 year spread is trading near -21 basis points after closing the week ago at -2.7 basis points. The low reached -27 basis points this week.

Wishing you all a good weekend.