Yen’s selloff continued overnight together with strong rebound in US 10-year yield. The Japanese currency remains pressured in Asian session and remains vulnerable. At the same time, Euro and Sterling are also weakening notably. Dollar is rebounding, but for now, Canadian and Australian are still the strongest one for the week. There is prospect for the greenback to overtake the first place, but that might need some strong non-farm payroll data tomorrow.

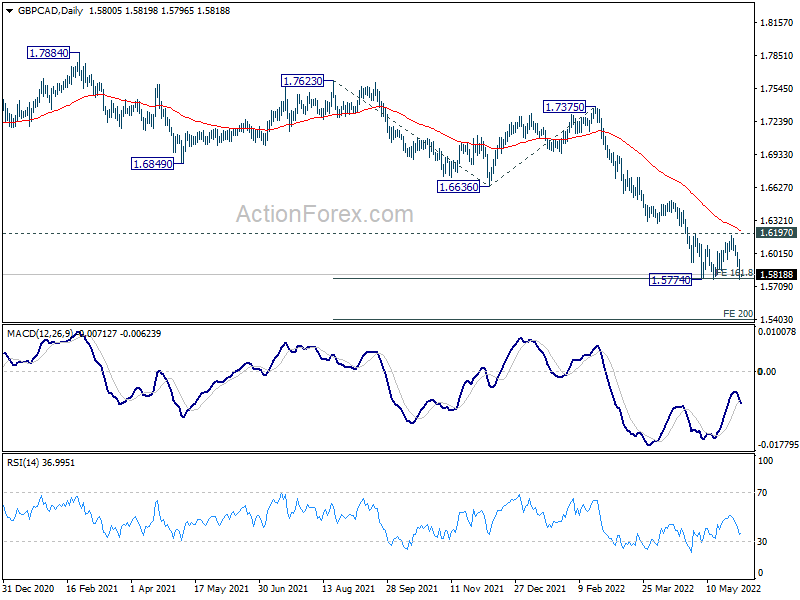

Technically, both GBP/CAD and EUR/CAD appear to be ready for down trend resumption, as part of the reaction to yesterday’s hawkish BoC rate hike. As for GBP/CAD, immediate focus is on 1.5774 support. Firm break there will confirm this bearish case and target 200% projection of 1.7623 to 1.6636 from 1.7375 at 1.5401. That might also be accompanied by deeper decline in GBP/USD back to 1.2154 short term bottom.

In Asia, at the time of writing, Nikkei is down -0.11%. Hong Kong HSI is down -1.57%. China Shanghai SSE is up 0.11%. Singapore Strait Times is down -0.46%. Japan 10-year JGB yield is up 0.0059 at 0.242. Overnight, DOW dropped -0.54%. S&P 500 dropped -0.75%. NASDAQ dropped -0.72%. 10-year yield rose 0.087 to 2.931.

Fed Daly: Let’s get to neutral as quickly as we can

San Francisco Fed President Mary Daly told CNBC yesterday, “I see a couple of 50-basis-point hikes immediately in the next couple of meetings to get there. And then we need to look around and see what else is going on.” She estimates that neutral rate is at around 2.50%, and said , “let’s get there as quickly as we can.”

“I’m looking for both supply to recover somewhat and demand to come back down a little bit. If neither of those things cooperate, then we need to go into restrictive territory,” Daly added.

Fed Bullard: We have a good plan with 50bps per meeting

St. Louis Fed President James Bullard reiterated yesterday, “I think we have a good plan for now. This 50 basis point per meeting increase is twice the normal pace that the committee has used in recent years which shows that there’s a lot of unanimity around expeditiously moving to neutral in this high-inflation environment that we’re in.”

Bullard also repeated that he wants to get rates to 3.5% by the end of the year. Then some of the rate hikes could be reversed late next year or in 2024. He pointed to the pre-pandemic rates, with Fed rates at 1.55%, 10-year yield at 1.86% and mortgage rates well below 4%. “This may provide a practical benchmark for where the constellation of rates may settle once inflation comes under control in the U.S.,” he said.

Fed Barkin: It makes perfect sense to normalize policy

Richmond Fed President Barkin said “it’s time both on rates and on the balance sheet to normalize where we are”. He added, with “inflation this elevated and the economy still this strong, it just makes perfect sense to do that.”

“When we get to the fall, I think we’re going to have a lot more information on the strength of the economy, we’ll have a lot more information on the pace of inflation. Those are the two things I’m paying the most attention to, and the stronger inflation and the stronger the economy, the more the case to do more, and to the extent that the two are weaker, the better the case is to do less,” he said.

BoJ Adachi: We should not forget strong yen led to two lost decades

BoJ board member Seiji Adachi said, “with the impact of the pandemic continuing, shifting to tighter monetary policy now would inflict huge damage to business and household activity… It’s premature to move toward tighter policy.”

“If the bank uses monetary policy to respond to short-term fluctuations (in exchange rates) before achieving its goal for underlying inflation, it would bring negative effects on the Japanese economy,” he said.

“We should not forget that a strong yen was among factors that led to Japan’s prolonged deflation and two ‘lost’ decades” of economic stagnation, he added.

On the data front

New Zealand terms of trade index rose 0.5% in Q1, below expectation of 1.3%. Australia trade surplus widened to AUD 10.5B in April, above expectation of AUD 9.0B. Japan monetary base rose 4.6% yoy in May, above expectation of 2.3% yoy.

Looking ahead, Swiss CPI and Eurozone PPI will be released in European session. Later in the day, US will release ADP employment, jobless claims, non-farm productivity and factory orders.

USD/JPY Daily Outlook

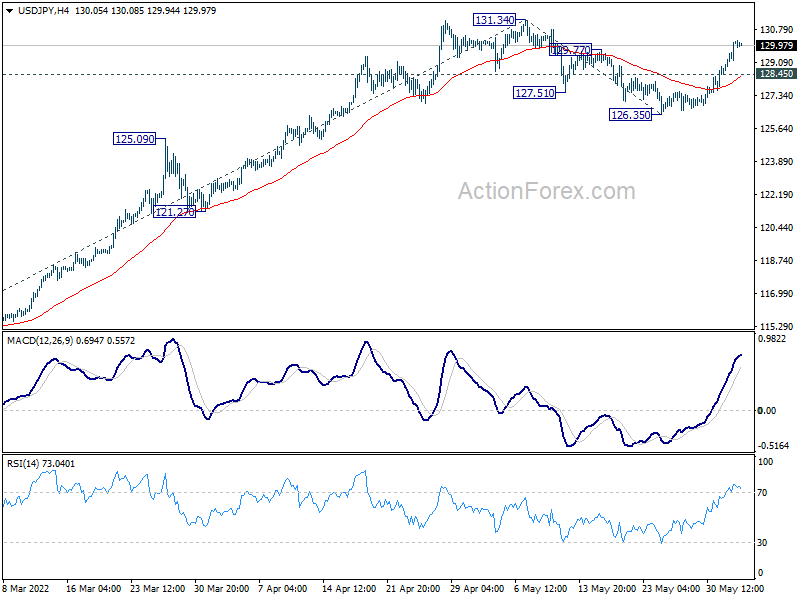

Daily Pivots: (S1) 129.15; (P) 129.67; (R1) 130.69; More…

USD/JPY’s break of 129.77 minor resistance indicates that pull back from 131.34 has completed with three waves down to 126.35. Intraday bias stays on the upside for 131.34 first. Firm break there will confirm up trend resumption. Next target is 61.8% projection of 114.40 to 131.34 from 126.35 at 136.81. On the downside, below 128.45 minor support will delay the bullish case and turn bias neutral first.

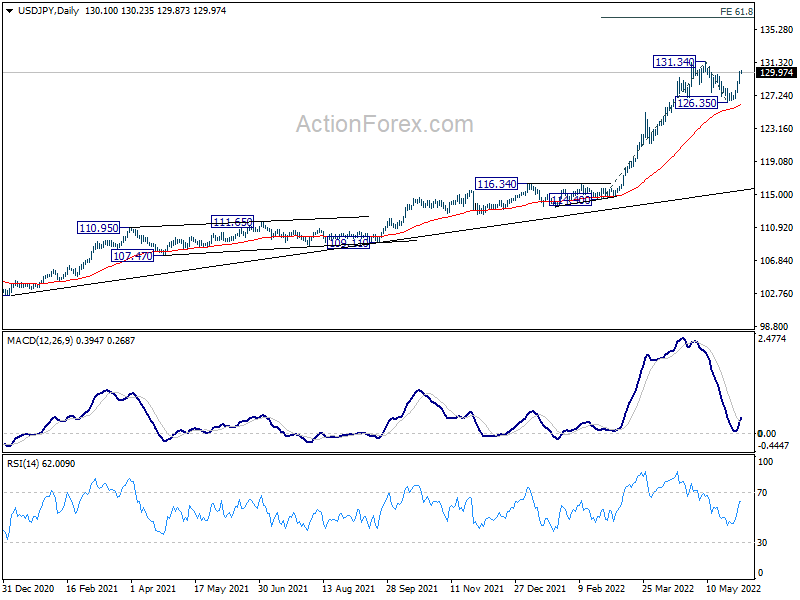

In the bigger picture, current rally is seen as part of the long term up trend form 75.56 (2011 low). Sustained trading above 61.8% projection of 75.56 (2011 low) to 125.85 (2015 high) from 98.97 at 130.04 will pave the way to 100% projection at 149.26, which is close to 147.68 (1998 high). For now, this will remain the favored case as long as 121.27 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Terms of Trade Index Q1 | 0.50% | 1.30% | -1.00% | -0.90% |

| 23:50 | JPY | Monetary Base Y/Y May | 4.60% | 2.30% | 6.60% | |

| 01:30 | AUD | Trade Balance (AUD) Apr | 10.50B | 9.02B | 9.31B | 9.74B |

| 06:30 | CHF | CPI M/M May | 0.30% | 0.40% | ||

| 06:30 | CHF | CPI Y/Y May | 2.60% | 2.50% | ||

| 09:00 | EUR | Eurozone PPI M/M Apr | 2.30% | 5.30% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Apr | 38.60% | 36.80% | ||

| 11:30 | USD | Challenger Job Cuts Y/Y May | 6.00% | |||

| 12:15 | USD | ADP Employment Change May | 280K | 247K | ||

| 12:30 | USD | Initial Jobless Claims (May 27) | 205K | 210K | ||

| 12:30 | USD | Nonfarm Productivity Q1 | -7.50% | -7.50% | ||

| 12:30 | USD | Unit Labor Costs Q1 | 11.60% | 11.60% | ||

| 12:30 | CAD | Building Permits M/M Apr | 0.50% | -9.30% | ||

| 14:00 | USD | Factory Orders M/M Apr | 0.80% | 2.20% | ||

| 14:30 | USD | Natural Gas Storage | 86B | 80B | ||

| 15:00 | USD | Crude Oil Inventories | -3.0M | -1.0M |