Markets are clearly in some risk aversion actions after Fed laid out the balance sheet runoff plan. Nikkei is leading other Asian stocks lower, after US indexes tumbled overnight. Australian Dollar is dragged down by the sentiment, followed by Kiwi and Loonie. On the other hand, Euro is recovering mildly for today. But for the week, Dollar is currently the strongest one, as supported by surging treasury yield and Fed expectations. Euro is still the weakest on dovish ECB and Ukraine uncertainty.

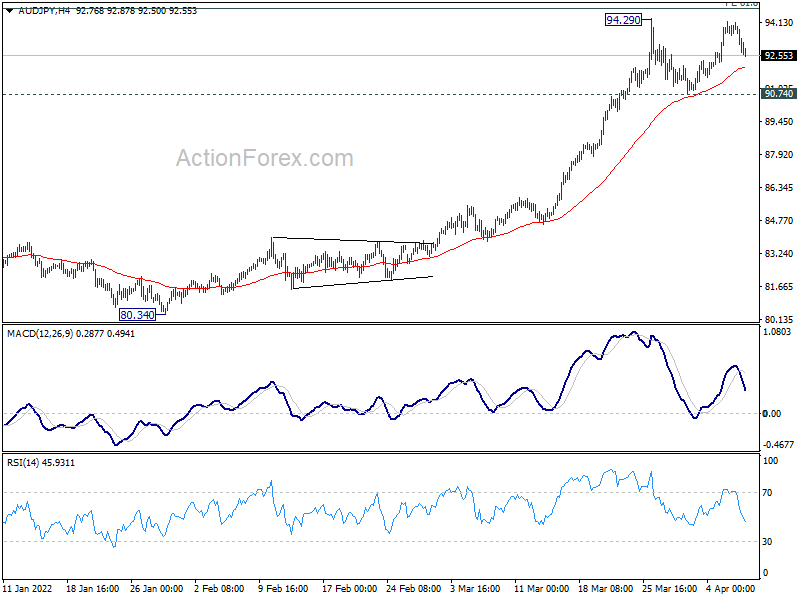

Technically, Aussie is apparently turning weaker today, but the selloff is not disastrous. A focus will be on 90.74 support in AUD/JPY. As long as this level holds, firstly, AUD/JPY’s outlook will stay bullish for another rally through 94.29 high. Secondly, that should help floor selling in Aussie elsewhere. However, firm break of 90.74 would be a warning that the tide in Aussie is turning near term bearish.

In Asia, at the time of writing, Nikkei is down -2.00%. Hong Kong HSI is down -0.85%. China Shanghai SSE is down -0.76%. Singapore Strait Times is down -0.55%. Japan 10-year JGB yield is down -0.0087 at 0.236. Overnight, DOW dropped -0.42%. S&P 500 dropped -0.97%. NASDAQ dropped -2.22%. 10-year yield rose 0.053 to 2.609.

Fed plans to shrink balance sheet by $95B per month

In the minutes of the March 15-16 FOMC meeting, many participants said they would have preferred a 50bps hike because inflation was well above target, and risks were to the upside. However, a number of them pointed out the “greater near-term uncertainty” associated with the Russia invasion of Ukraine. Thus, a 25bps hike was taken at that meeting.

However, “many participants noted that one or more 50 basis point increases in the target range could be appropriate at future meetings, particularly if inflation pressures remained elevated or intensified.

Meanwhile “all participants” agreed that balance sheet runoff should start “at a coming meeting”. ” Participants generally agreed that monthly caps of about $60 billion for Treasury securities and about $35 billion for agency MBS would likely be appropriate. Participants also generally agreed that the caps could be phased in over a period of three months or modestly longer if market conditions warrant.

BoJ Noguchi: Takes significant time to justify stimulus withdrawal

Bank of Japan board member Asahi Noguchi said while core consumer inflation may exceed 2% from April, it’s mainly driven by external factors rather than domestic demand. He added, “Japan is not experiencing the kind of high inflation seen in many other countries.”

“In a country still mired in a sticky deflationary mindset, it will take significant time to stably achieve our 2% inflation target and justify a withdrawal of stimulus,” he added.

Australia AiG services dropped to 56.2, intensifying price and wage pressures

Australia AiG Performance of Services Index dropped -3.8 pts to 56.2 in March. Sales dropped sharply by -14.9 to 53.7. Employment dropped -0.3 to 54.4. But new orders rose 2.4 to 63.5. Input prices jumped 11.5 to 77.5. Selling prices also rose 4.2 to 64.5. Average wages surged 11.8 to 67.7.

Innes Willox, Chief Executive of the national employer association Ai Group, said: “Australia’s services sector continued its positive run in March although the pace of growth slowed in the face of intensifying input price pressures, difficulties in finding staff and further wage pressures.”

Also from Australia, goods and services export was relatively unchanged over the month at AUD28.8B in February. Goods and services imports rose 12% mom to AUD 41B. Trade surplus shrank to AUD 7.46B, smaller than expectation of AUD 11.70B.

Looking ahead

Swiss unemployment rate and foreign currency reserves will be released in European session. Germany will release industrial production. Eurozone will release retail sales. But main focus will be on ECB monetary policy meeting accounts. Later in the day, US will release jobless claims.

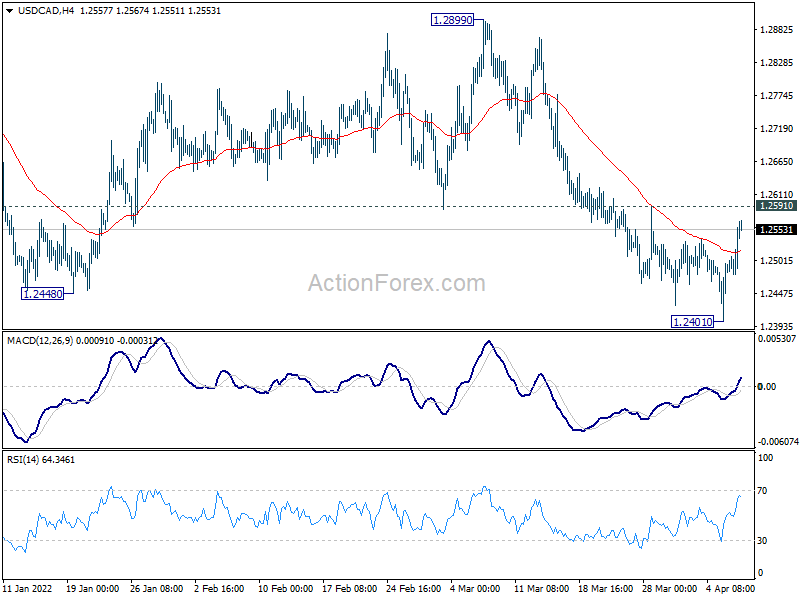

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2427; (P) 1.2462; (R1) 1.2522; More…

Intraday bias in USD/CAD remains neutral for the moment. Another fall could still be seen with 1.2591 resistance intact. Corrective pattern from 1.2005 could have completed already. Break of 1.2401 will target 1.2286 support and then 1.2005 low. However, on the upside, break of 1.2591 will dampen this bearish case, and turn bias back to the upside for 1.2899 resistance instead.

In the bigger picture, focus stays on 38.2% retracement of 1.4667 (2020 high) to 1.2005 (2021 low) at 1.3022. Sustained break there should confirm that the down trend from 1.4667 has completed after defending 1.2061 long term cluster support. Further rise would then be seen towards 61.8% retracement at 1.3650. However, rejection by 1.3022 will maintain medium term bearishness. Break of 1.2005 will resume the down trend from 1.4667 and that carries larger bearish implications too.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Services Index Mar | 56.2 | 60 | ||

| 01:30 | AUD | Trade Balance (AUD) Feb | 7.46B | 11.70B | 12.89B | 11.79B |

| 05:00 | JPY | Leading Economic Index Feb P | 103 | 102.5 | ||

| 05:45 | CHF | Unemployment Rate Mar | 2.20% | 2.20% | ||

| 06:00 | EUR | Germany Industrial Production M/M Feb | 0.00% | 2.70% | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Mar | 938B | |||

| 09:00 | EUR | Eurozone Retail Sales M/M Feb | 0.60% | 0.20% | ||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:30 | USD | Initial Jobless Claims (Apr 1) | 200K | 202K | ||

| 14:30 | USD | Natural Gas Storage | 18.0B | 26B |