Yen’s selloff re-accelerates after Fed Chair Jerome Powell hinted at a 50bps rate hike at next meeting in May. Dollar is firming up broadly, but trails Canadian. Loonie is supported by extended rebound in oil price, as well as expectations of more BoC tightening too. Swiss Franc is currently the second weakest, followed by Sterling and Euro. Aussie and Kiwi are mixed for now.

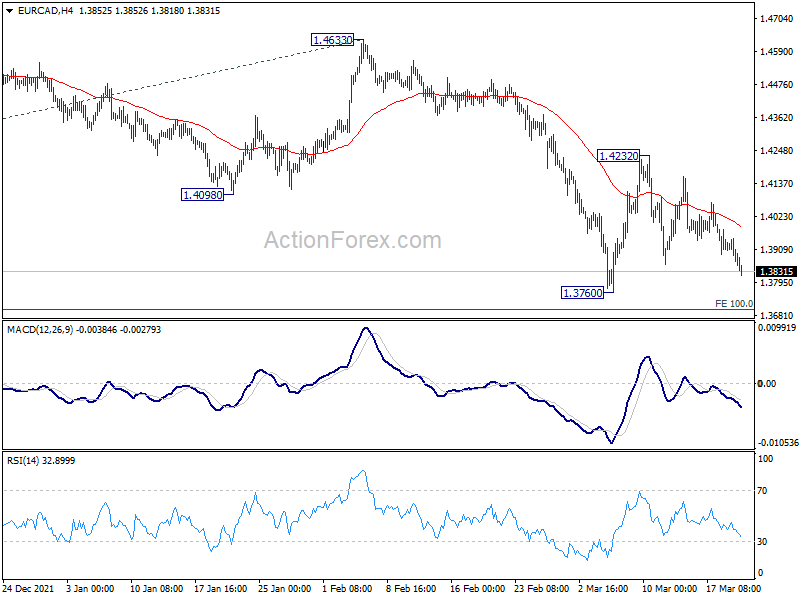

Technically, in addition to the selloff in Yen, attention will also be on return of weakness in Euro. In particular, EUR/CAD has taken out 1.3856 minor support and it’s heading back to 1.3760. Firm break there will resume medium term down trend. EUR/AUD is falling to corresponding low at 1.4561 and break will align with outlook too. At the same time, EUR/GBP is pressing 0.8358 minor support and break will bring retest of 0.8201 low.

In Asia, at the time of writing, Nikkei is up 1.44%. Hong Kong HSI is up 1.13%. China Shanghai SSE is up 0.14%. Singapore Strait Times is down -0.17%. Japan 10-year JGB yield is up 0.0183 at 0.226. Overnight, DOW dropped -0.58%. S&P 500 dropped -0.04%. NASDAQ dropped -0.40%. 10-year yield rose 0.167 to 2.315.

Fed Powell hints on 50bps hike next, 10-year yield surges

US benchmark treasury yield jumped sharply overnight after Fed Chair Jerome Powell gave green light to more aggressive tightening pace. He said, “there is an obvious need to move expeditiously to return the stance of monetary policy to a more neutral level, and then to move to more restrictive levels if that is what is required to restore price stability.”

In particular, he added, “if we conclude that it is appropriate to move more aggressively by raising the federal funds rate by more than 25 basis points at a meeting or meetings, we will do so.”

Fed fund futures are now indicating 61.6% chance of a 50bps hike at May 4 meeting to 0.75-100%, up from 43.9% a day ago.

10-year yield rose 0.167 to close at 2.315. Near term outlook in TNX will stay bullish as long as 2.065 resistance turned support holds. Next target is 100% projection of 0.398 to 1.765 from 1.343 at 2.710.

BoJ Kuroda: We need to patiently maintain our powerful monetary easing

BoJ Governor Haruhiko Kuroda reiterated to the parliament today that it’s still premature to discuss details on stimulus exit. “Given recent price developments, we need to patiently maintain our powerful monetary easing,” he said.

Kuroda said consumer prices are likely to rise. However, he warned that “instead of leading to higher wages and corporate profits, such cost-push inflation will weigh on the economy in the long run by hurting corporate profits and households’ real income.”

New Zealand Westpac consumer confidence dropped to 92.1, lowest since 2008

New Zealand Westpac consumer confidence dropped from 99.1 to 92.1 in Q1, hitting the lowest level since the global financial crisis in 2008. Present conditions index dropped from 94.8 to 90.1. Expected conditions index dropped from 101.9 to 93.5. One-year economic outlook dropped from -11.2 to -22.8. Five-year economic outlook dropped from 10.0 to 0.8.

Westpac said:”Households have reported that their financial position has deteriorated as the economy has been buffeted by a multitude of headwinds. That includes rising consumer prices and higher mortgage rates, both of which are squeezing households’ disposable incomes. The rapid spread of Omicron is also likely to have dampened confidence in recent weeks.

Looking ahead

UK will release public sector net borrowing. Eurozone will release current account. Canada will release IPPI and RMPI.

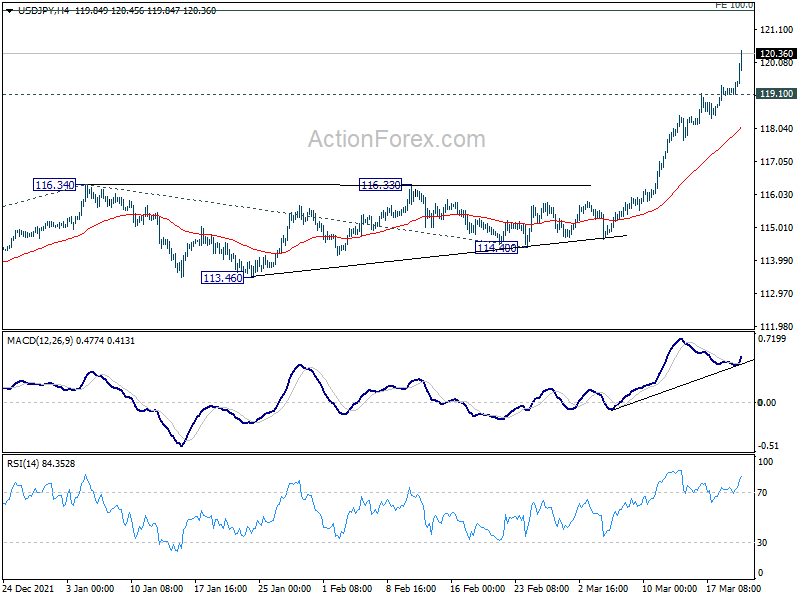

USD/JPY Daily Outlook

Daily Pivots: (S1) 119.21; (P) 119.36; (R1) 119.61; More…

USD/JPY’s rally continues today and hits as high as 120.45 so far. Intraday bias remains on the upside. Current up trend should target 100% projection of 109.11 to 116.34 from 114.40 at 121.63 next. On the downside, below 119.10 will turn intraday bias neutral and bring consolidation. But downside should be contained well above 116.34 resistance turned support to bring another rally.

In the bigger picture, the break of 118.65 resistance (2016 high) suggest that up trend from 98.97 (2016 low) is resuming, with rise from 101.18 (2020 low) as the third leg. Medium term outlook will remain bullish as long as 113.46 low. Sustained trading above 118.65 will pave the way to 125.85 (2015 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 20:00 | NZD | Westpac Consumer Survey Q1 | 92.1 | 99.1 | ||

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Feb | -4.5B | -3.7B | ||

| 09:00 | EUR | Eurozone Current Account (EUR) Jan | 24.3B | 22.6B | ||

| 12:30 | CAD | Industrial Product Price M/M Feb | 1.20% | 3.00% | ||

| 12:30 | CAD | Raw Material Price Index M/M Feb | -0.60% | 6.50% |