The market in the North American session took a breather from the geopolitical news from Ukraine early on, to focus on the Canadian jobs report for February. Most of the time, Canada and the US release their jobs report on the same first Friday of the calendar month. However because of calendar nuances, there are instances where they don’t overlap. This month was one of those instances.

Canada reported much stronger than expected job gain of 336.6K vs 160K estimate. The gain was the largest since October 2020. The unemployment rate tumbled to 5.5% from 6.2% estimate. That took the unemployment rate below the pre-pandemic level of 5.7%. The participation rate increase to 65.4%,and both full and part-time employment rose sharply. The private sector added 347K jobs. Average hourly earnings were up 3.3% versus 2.4% last month.

Admittedly, the prior month was worse than expected as result of omicron, but the bounce back gains this month were much stronger and certainly justify the Bank of Canada’s decision to raise rates despite the lower jobs last month.

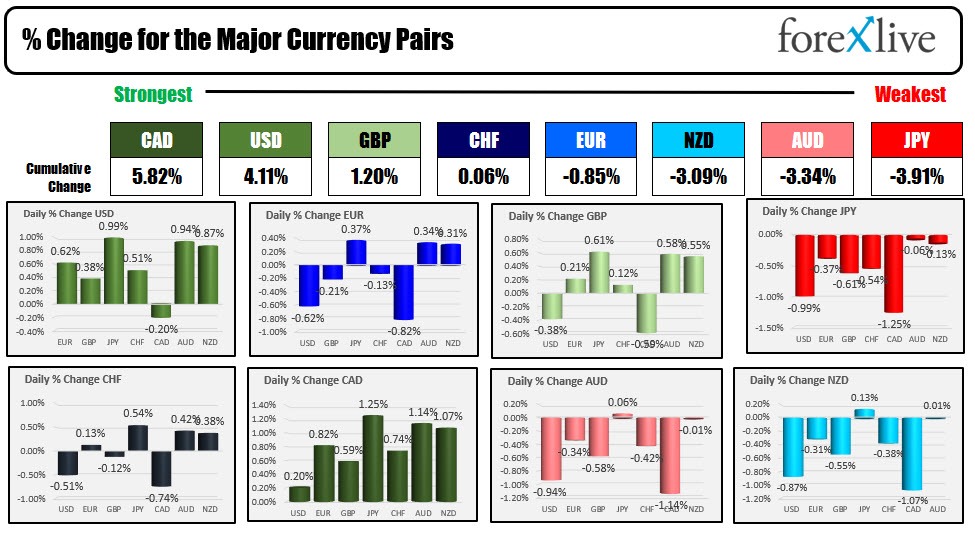

The data helped to push the CAD to the top of the strongest weakest of the major currencies. The JPY was the weakest. The USD – although lower vs the CAD – at solid gains against the other major currencies with a near 1% rise verse the JPY and AUD (0.99% and 0.94% respectively). The greenback rose 0.87% verse the NZD as well.

The US dollar bounce back over the last two trading days in what was an up, down and back up trading week for the greenback. The dollar index (DXY) last Friday closed at 98.509. The high price on Monday extended to 99.418 before rotating back to the downside and reaching a low yesterday at 97.712. That low was near the broken 61.8% retracement of the move down from the March 2020 high at 96 7.727.

However the price rebounded into the close yesterday and continued that rebound today. It is currently trading at 99.12 which is not far from the high for the week.

Helping the greenback move back to the upside was a run back to the upside in US rates after bottoming on Monday right at its 100 day moving average (see blue line in the chart below) at 1.668%. The rest of the week was spent moving higher, and the yield is closing the week near 2.00%. That is a gain of 33 basis points from the low to the high.

For the 2 year yield, the rate on Monday bottomed at 1.424% and is ending the week at 1.752% which is also a 33 basis point gain.

Recall at the start the week there was anxiety from the Russian Ukraine weekend news. Crude oil prices shot up to $130. There was a flight into the relative safety of the US dollar and US debt. However, as oil prices moved back to the downside (crude oil was down -5.49% on the week), so did treasury prices (which led to higher yields).

In other markets to end the week,

- Spot gold had a volatile up and down week reaching a high of $2070.42 before falling back down today to a intraday low of $1958.84. The price is closing near $1988.13 down around $8.46 -0.42% on the day. The price closed last week near $1970.95. For the week the price is up $17.18 or 0.87%

- WTI crude oil futures are going out near $109.09 that’s up $3.07 or 2.9%. As mentioned the high price reached $130.50 in the early trading on Monday before rotating to the downside and trading as low as $103.63 on Wednesday. Today’s low reached $104.48 with an intraday high of $110.29.

In the stock markets today, the European indices all closed higher for the day and also higher for the week despite the tensions in Ukraine. The US major stock indices were different story as all them close lower today and closed lower for the week. The major US indices are down six of the last seven trading days.

Fundamentally today, the US announced that they would revoke permanent normal trade relations with Russia. As such they announced that they would cease importing diamonds, caviar and other seafood, and liquor products including vodka. Meanwhile the G7 announced additional sanctions as well saying that they too would deny Russia most favored nation status relating to key products, that they would work collectively to prevent Russia from obtaining financing from leading multinational institutions, they will suspend Russia’s membership rights to the IMF and World Bank, and continue to pressure Russia’s elite/oligarchs. Both the US and EU also said that they would ban the export of luxury goods to Russia.

In the US, Michigan consumer sentiment data fell to a near 11 year low (lowest level since September 2011) the index came in at 59.7 much lower than the expected 61.4% fall from 62.8% February. Higher oil prices and the Russian/Ukraine conflict soured the consumers mood. Inflation measures also increased with the one year inflation expectations jumping to 5.4% which was the highest reading since 1981 (up from 4.9% of February). The five year inflation expectations remain steady 3.0% for the second straight month.

Next week, the FOMC will meet on Tuesday and Wednesday with their interest rate decision announced on Wednesday at 2 PM ET. The expectations are for the Fed to raise rates by 25 basis points. Market traders will be focused on the dot plot along with the Fed’s central tendencies for GDP growth, employment, and inflation.

In December, the Fed was targeting three hikes in 2022 (up to 0.75% to 1.0% from 0.0% to 0.25%). That most certainly will be going up. We know from Feds Bullard that he would like to see the equivalent of 100 basis point increase by the 4th of July. Other Fed officials are penciling in four hikes for 2022, with the bias for more if inflation does not start to come back down. There is a chance for the expectations to rise to 5 hikes.

Also on the schedule is retail sales and PPI in the US. The Bank of England will also meet and are expecting to raise rates for the 3rd time in 3 meetings (15 hike, 25 hike, and another 25 basis point hike next week as they continue to fight inflation).

Australia will release jobs data.

On Sunday, the US will spring forward with their clocks which will make the time difference between the US and London 4 hours until that is changed later in the month (March 27). So the 4 PM London fixing will be at 12 noon, and London traders will exit for the day near 1 PM ET (vs 12 PM normally). US data released at 8:30 AM ET, will come out at 1230 London time vs 1330 normally. I know it is not that difficult, but I always have to think a little extra hard to keep things straight.

Hope you all have a safe and joyous weekend.

Peace…..