The markets are surprisingly calm despite some initial volatility on escalation in Russia Ukraine situation. News of sanctions on Russia are staying to flow out, with the UK sanctioning five Russians banks and three individuals. Germany also put the certification of the Nord Stream 2 gas pipeline on hold. But there are just very little reactions in the markets.

Major European indexes are mixed in very tight range while DOW futures are just slightly down. Yields of benchmark treasuries are indeed rising. Gold is hovering around 1900 handle after initial rally lost momentum. WTI crude oil also retreats quickly after breaching 95.98 resistance very briefly.

In the currency markets, Kiwi and Aussie are currently the strongest ones. Euro is following closely with help from rally in German yields. Sterling remains the worst performing, but Swiss Franc and Yen are also weak. Dollar and Loonie are mixed in between.

At the time of writing, FTSE is up 0.24%. DAX is down -0.31%. CAC is down -0.03%. Germany 10-year yield is up 0.070 at 0.278. Earlier in Asia, Nikkei dropped -1.71%. Hong Kong HSI dropped -2.69%. China Shanghai SSE dropped -0.96%. Singapore Strait Times dropped -1.04%. Japan 10-year JGB yield dropped -0.0108 to 0.198.

BoE Ramsden: 50bps hike would have been warranted in Feb

BoE Deputy Governor Dave Ramsden said a speech, “personally I felt that the 0.5pp increase in Bank Rate would have been warranted in February, in line with a watchful and responsive approach to monetary policy”.

“I have concerned about the emerging inflationary impetus from a tight labour market and from a broadening out in price pressures since last summer… have been voting for some front-loaded tightening in monetary policy since last September”, he added.

“Looking ahead, like the rest of the Committee I judge that if the economy develops broadly in line with the February MPR forecast, some further modest tightening in monetary policy is likely to be appropriate in the coming months,” he said”.

Nevertheless he emphasized that the word ” modest” was “significant”. “I do not envisage Bank Rate rising to anything like its pre-2007 level of 5% or above, let alone to the kind of levels we used to see before the MPC was formed in 1997,” he said.

Germany Ifo business climate rose to 98.9, betting on an end to coronavirus crisis

Germany Ifo Business Climate rose from 96.0 to 98.9 in February, above expectation of 96.5. Current Assessment Index rose from 96.2 to 98.6, above expectation of 96.6. Expectations index rose from 95.8 to 99.2, above expectation of 96.5.

By industry, manufacturing rose from 20.0 to 23.5. Services rose from 7.7 to 13.5. trade rose from -1.3 to 6.6. Construction rose from 8.0 to 8.3.

Ifo said, “the German economy is betting on an end to the coronavirus crisis. However, the escalation of the crisis engulfing Ukraine remains a risk factor.”

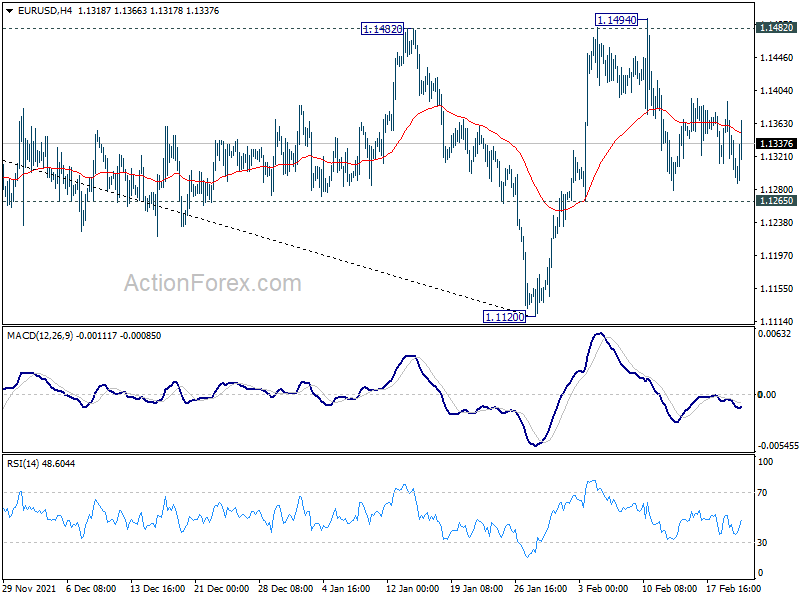

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1282; (P) 1.1336; (R1) 1.1364; More…

EUR/USD recovers notably after initial dip today, but stays well inside range of 1.1265/1482. Intraday bias remains neutral and outlook is unchanged. On the upside, firm break of 1.1482 will target 38.2% retracement of 1.2348 to 1.1120 at 1.1589 next. Sustained break there will argue that whole fall from 1.2348 has completed too and target 61.8% retracement at 1.1879. On the downside, however, break of 1.1265 support will dampen this bullish view and bring retest of 1.1120 low instead.

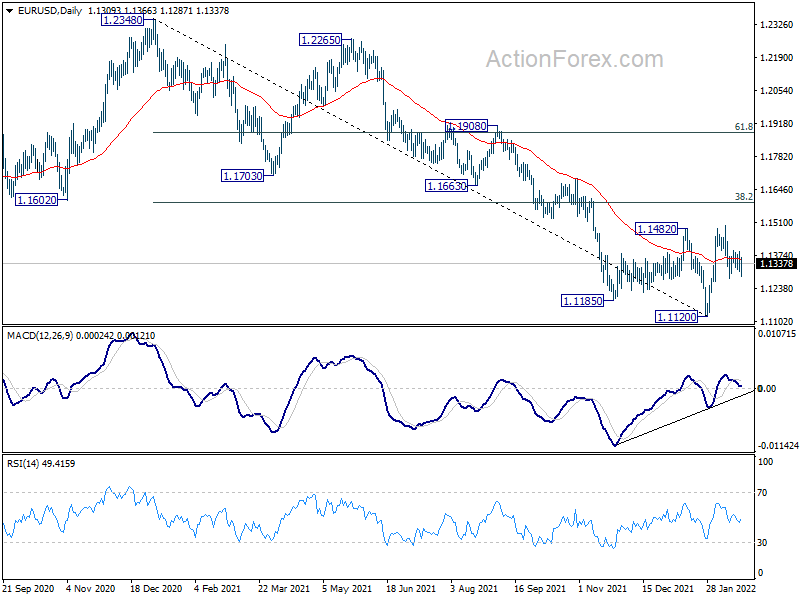

In the bigger picture, the decline from 1.2348 (2021 high) is seen as a leg inside the range pattern from 1.2555 (2018 high). Sustained trading above 55 week EMA (now at 1.1593) will argue that it has completed and stronger rise would be seen back towards top of the range between 1.2348 and 1.2555. However, firm break of 1.0635 (2020 low) will raise the chance of long term down trend resumption and target a retest on 1.0339 (2017 low) next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Jan | 1.20% | 1.20% | 1.10% | |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Jan | -3.7B | -3.6B | 16.1B | |

| 09:00 | EUR | Germany IFO Business Climate Feb | 98.9 | 96.5 | 95.7 | 96.0 |

| 09:00 | EUR | Germany IFO Current Assessment Feb | 98.6 | 96.6 | 96.1 | 96.2 |

| 09:00 | EUR | Germany IFO Expectations Feb | 99.2 | 96.5 | 95.2 | 95.8 |

| 14:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Dec | 18.00% | 18.30% | ||

| 14:00 | USD | Housing Price Index M/M Dec | 1.10% | 1.10% | ||

| 14:45 | USD | Manufacturing PMI Feb P | 56 | 55.5 | ||

| 14:45 | USD | Services PMI Feb P | 53 | 51.2 | ||

| 15:00 | USD | Consumer Confidence Feb | 110.2 | 113.8 |