Overall market sentiment improved a lot after Russia said it pulled back some troops near the border of Ukraine. As worries of imminent war eased, Gold and oil price dip notably, while stocks rebound. Euro is staging a recovery, together with Aussie and Kiwi. On the other hand, Yen and Dollar are turning softer, together with Canadian. Sterling and Swiss Franc are mixed for the moment.

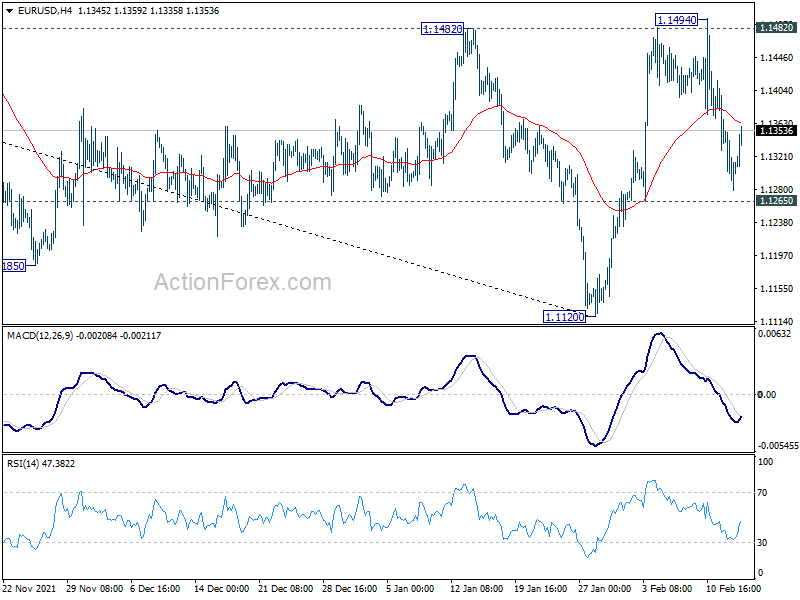

Technically, EUR/USD has somewhat defended 1.1265 minor support for now, maintaining mild near term bullish bias. There is prospect of extending the rebound to retest 1.1483 key near term resistance. Meanwhile, EUR/JPY could also be heading back to 133.13/133.44 resistance zone. But is should be noted level these levels would also be broken if the Russia/Ukraine situation is totally cleared.

In Europe, at the time of writing, FTSE is up 0.79%. DAX is up 1.61%. CAC is up 1.29%. Germany 10-year JGB yield is up 0.040 at 0.322. Earlier in Asia, Nikkei dropped -0.79%. Hong Kong HSI dropped -0.82%. China Shanghai SSE rose 0.50%. Singapore Strait Times rose 0.01%. Japan 10-year JGB yield dropped -0.0019 to 0.216.

US PPI rose 1% mom, 9.7% yoy in Jan

US PPI for final demand rose 1.0% mom in January, above expectation of 0.6% mom. PPI for final demand services rose 0.7% mom. PPI for final demand goods rose 1.3% mom. For the 12-month period, PPI was unchanged at 9.7% yoy, above expectation of 9.2% yoy.

Excluding foods, energy and trade services, PPI rose 0.9% mom, largest since January 2021. For the 12-monht period, PPI less foods, energy, and trade services rose 6.9% yoy.

Empire state manufacturing index rose for m-0.7 to 3.1 in February, below expectation of 10.0.

Germany ZEW rose to 54.3, outlook continues to improve despite growing economic and political uncertainties

Germany ZEW Economic Sentiment rose from 51.7 to 54.3 in February, above expectation of 53.5. Current Situation index rose from -10.2 to -8.1, worse than expectation of -7.0.

Eurozone ZEW Economic Sentiment dropped from 49.4 to 48.6, below expectation of 52.3. Current Situation Index rose 6.8 to 0.6. Inflation expectations for Eurozone rose 3.6 pts to -35.1. 53.2% of expects expect inflation rate to decline in the next six months.

“The economic outlook for Germany continues to improve in February despite growing economic and political uncertainties. Financial market experts expect an easing of pandemic-related restrictions and an economic recovery in the first half of 2022. They still expect inflation to decline, albeit at a slower pace and from a higher level than in previous months. Consequently, more than 50 per cent of the experts now predict that short-term interest rates in the euro area will rise in the next six months,” comments ZEW President Professor Achim Wambach on current expectations.

Eurozone exports of goods to the rest of the world grew 14.1% yoy to EUR 218.7B in December. Imports rose 36.7% yoy to EUR 223.3B. Trade deficit came in at EUR -4.6B. Intra-Eurozone trade rose 27.8% yoy to EUR 191.9B.

In seasonally adjusted terms, exports dropped -0.6% mom while imports rose EUR 3.1% mom. Trade deficit was at EUR -9.7B, larger than expectation of EUR -2.5B.

For whole of 2021, exports rose 14.1% to EUR 2434.4B. Imports rose 21.4% to EUR 2305.9B. Trade surplus came in at EUR 128.4B, down from EUR 233.9B in 2020.

Eurozone GDP grew 0.3% qoq, 4.6% yoy in Q4. Annual growth 2021 was at 5.2%. Employment rose 0.5% qoq.

UK payrolled employees rose 108k in Jan, unemployment rate unchanged at 4.1% in Dec

UK payrolled employees rose rose 0.4% mom, or 108k, to 29.5m in January. Over the year, payrolled employees grew 4.8% yoy, or 1.35m. Claimant count dropped -31.9k.

In the three months to December, unemployment rate was unchanged at 4.1%, matched expectations. That’s still 0.1% higher than before the pandemic, but down -0.2% from the previous three-month period. Employment rate rose 0.1% to 75.5%, comparing to the previous 3-month period.

Average earnings including bonus rose 4.3% 3moy, much better than expectation of 3.9%. Average earnings excluding bonus rose 3.7% 3moy, above better than expectation of 3.6%.

BoJ Kuroda: Baseline for economy and prices to gradually pick up

BoJ Governor Haruhiko Kuroda reiterated that the baseline forecast is for Japan’s economy and prices to gradually pick up as rising real household income underpins consumption. Nevertheless, the “economic and price conditions warrant maintaining our easy monetary policy.”

He acknowledged that the market operation of an offer to buy unlimited amount of bonds on Monday successfully pushed 10-year JGB yield from near 0.25% to 0.22%. But he emphasized it’s a “last resort” and a “powerful means not used explicitly by other central banks.” “We don’t expect to conduct such operation frequently. We’ll do this as needed,” he added.

Japan GDP grew 1.3% qoq in Q4, remains slightly be pre-pandemic level

Japan GDP grew 1.3% qoq in Q4, slightly below expectation of 1.4% qoq. In annualized term, GDP grew 5.4%, below expectation of 5.8%.

Private consumption grew 2.7% qoq, accounting for much of the growth. Capital expenditure rose 0.4% qoq. External demand rose 0.2% qoq.

For 2021 as a whole, GDP grew 1.7%, marking the first expansion in three years. The seasonally-adjusted real GDP size at JPY 541T remains slightly below pre-pandemic level of late 2019.

RBA minutes: Prepared to be patient on interest rate

In the minutes of February 1 meeting, RBA reiterated that it “will not increase the cash rate until actual inflation is sustainably within the 2 to 3 per cent target band.” It’s “too early to conclude that it was sustainably within the target band”. There were uncertainties about “how persistent the pick-up in inflation would be as supply-side problems were resolved” and “wages growth also remained modest”. The central bank is “prepared to be patient”.

Omicron outbreak “had affected the economy, but had not derailed the recovery”. The economy was “resilient” and was expected to “pick up as case numbers trended lower”. Job market had “recovered strongly” with central forecasts seeing unemployment to fall to “levels not seen since early 1970s”. Wages growth was expected to pick-up, buy only gradually.

Inflation had “picked up more quickly than the Bank had expected”, but was still “lower than in many other countries”. “Some moderation” in inflation was expected as “supply problems were resolved.” Stronger growth in labour costs was expected to become the “more important driver of inflation”. The central forecast was for underlying inflation to be within the target band over both 2022 and 2023.

A decision about reinvestment of asset purchases would be made at the May meeting, with the key considerations being the “state of the economy and the outlook for inflation and unemployment.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1269; (P) 1.1319; (R1) 1.1358; More…

EUR/USD recovered ahead of 1.1265 minor support. Intraday bias remains neutral and further rise is still mildly in favor. On the upside break of 1.1482 will target 38.2% retracement of 1.2348 to 1.1120 at 1.1589 next. Sustained break there will argue that whole fall from 1.2348 has completed too and target 61.8% retracement at 1.1879. On the downside, however, break of 1.1265 support will dampen this bullish view and bring retest of 1.1120 low instead.

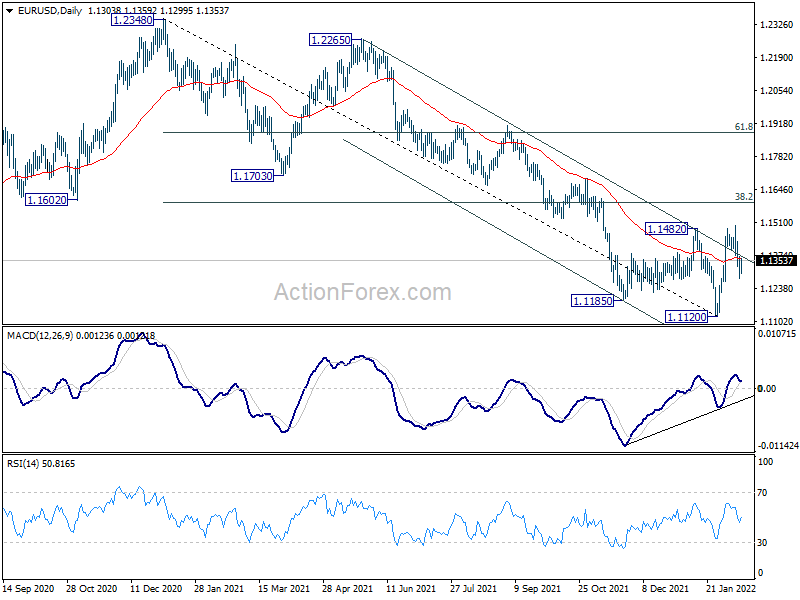

In the bigger picture, the decline from 1.2348 (2021 high) is seen as a leg inside the range pattern from 1.2555 (2018 high). Sustained trading above 55 week EMA (now at 1.1613) will argue that it has completed and stronger rise would be seen back towards top of the range between 1.2348 and 1.2555. However, firm break of 1.0635 (2020 low) will raise the chance of long term down trend resumption and target a retest on 1.0339 (2017 low) next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q4 P | 1.30% | 1.40% | -0.90% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 P | -1.30% | -1.20% | -1.20% | |

| 00:30 | AUD | RBA Minutes | ||||

| 04:30 | JPY | Industrial Production M/M Dec F | -1.00% | -1.00% | -1.00% | |

| 07:00 | GBP | Claimant Count Change Jan | -31.9K | -43.3K | -51.6K | |

| 07:00 | GBP | ILO Unemployment Rate (3M) Dec | 4.10% | 4.10% | 4.10% | |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Dec | 3.70% | 3.60% | 3.80% | |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Dec | 4.30% | 3.90% | 4.20% | |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Dec | -9.7B | -2.5B | -1.3B | -1.8B |

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | 0.30% | 0.30% | 0.30% | |

| 10:00 | EUR | Eurozone Employment Change Q/Q Q4 P | 0.50% | 0.40% | 0.90% | |

| 10:00 | EUR | Germany ZEW Economic Sentiment Feb | 54.3 | 53.5 | 51.7 | |

| 10:00 | EUR | Germany ZEW Current Situation Feb | -8.1 | -7 | -10.2 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Feb | 48.6 | 52.3 | 49.4 | |

| 13:15 | CAD | Housing Starts Jan | 230.8K | 270.0K | 236.1K | 238.4K |

| 13:30 | USD | Empire State Manufacturing Index Feb | 3.1 | 10 | -0.7 | |

| 13:30 | USD | PPI M/M Jan | 1.00% | 0.60% | 0.20% | 0.40% |

| 13:30 | USD | PPI Y/Y Jan | 9.70% | 9.20% | 9.70% | 9.80% |

| 13:30 | USD | PPI Core M/M Jan | 0.80% | 0.50% | 0.50% | 0.60% |

| 13:30 | USD | PPI Core Y/Y Jan | 8.30% | 8.10% | 8.30% |