The markets are steady in Asia in a quiet start to the week. Euro is softening slightly, paring some of last week’s gain. Aussie and Kiwi also turn weaker on mild risk aversion. On the other hand, Dollar and Canadian are both regaining some grounds. It’s a relatively light week in terms of economic data and events. But US consumer inflation data on Thursday as every potential to give the markets a bang.

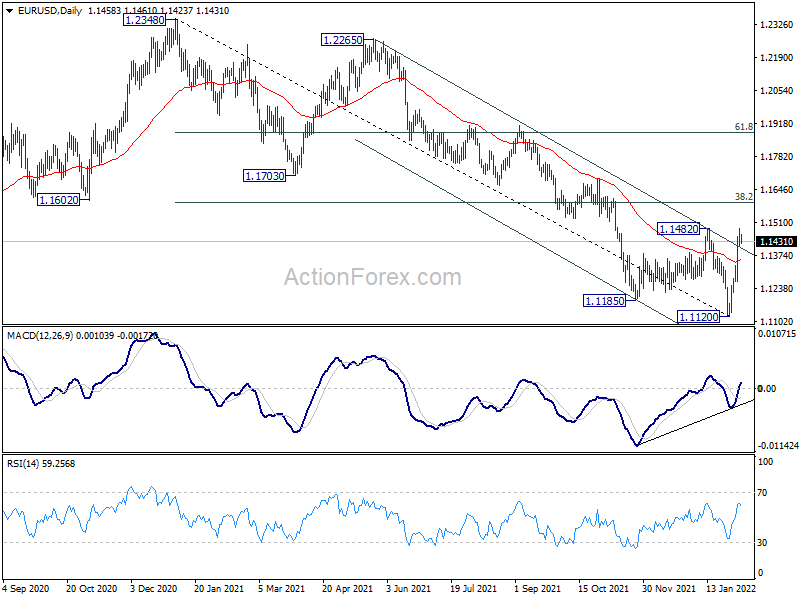

Technically, an immediate focus is 1.1482 resistance in EUR/USD. Firm break there would confirm medium term bottoming at 1.1120, on bullish convergence condition in daily MACD. Stronger rise should at least be seen to 38.2% retracement of 1.2348 to 1.1120 at 1.1589, with prospect of reversing whole down trend from 1.2348.

In Asia, at the time of writing, Nikkei is down -0.91%. Hong Kong HSI is down -0.47%. China Shanghai SSE is up 1.91%. Singapore Strait Times is up 0.23%. Japan 10-year JGB yield is up 0.0029 at 0.204, standing firm above 0.2 handle.

Australia AiG services rose to 56.2, rising sales, employment and new orders

Australia AiG Performance of Services Index rose 6.6 pts to 56.2 in January, hitting the highest level since June last year. Looking at some details, sales rose 5.3 to 58.9. Employment rose 0.5 to 56.7. New orders rose 10.5 to 57.9. Supplier deliveries rose 11.0 to 51.4. Input prices rose 0.8 to 66.1. Selling prices rose 4.0 to 62.2. Average wages dropped -2.9 to 56.9.

Innes Willox, Chief Executive of Ai Group, said: “The performance of Australia’s services sector rose over the December-January period with sales, employment and new orders all growing compared with November…. Businesses reported a slight easing of input price and wages pressures compared with November while selling prices rose indicating a belated and partial recovery of earlier cost rises. The rise in employment, while encouraging, came alongside numerous reports of the unavailability of staff and appears likely to reflect businesses hiring staff to cover for the workforce impacts of the Omicron wave.”

Australia retail sales dropped -4.4% in Dec, up 8.2% in Q4

Australia retail sales dropped -4.4% mom in December to AUD 31.93B. For Q4, sales rose 8.2%, fastest on record.

Ben James, Director of Quarterly Economy Wide Statistics, said: “Consumers enthusiastically returned to discretionary spending following the end of Delta related lockdowns in October, and the continued easing of restrictions over the quarter. Well publicised concerns over product availability and delivery timeliness led to consumers bringing forward their end of year shopping, in conjunction with a re-opening spending splurge due to pent up consumer demand.”

“This post lockdown recovery aligns well with the previous nationwide Covid lockdown recovery in the September quarter 2020 where sales rose 6.3 per cent, more than recovering the losses of the June 2020 quarter fall of 3.5 per cent”.

China PMI composite dropped to 50.1, triple pressures of contracting demand, supply shocks and weakening expectations

China PMI Services dropped from 53.1 to 51.4 in January, above expectation of 50.5. PMI Composite dropped from 53.0 to 50.1.

Wang Zhe, Senior Economist at Caixin Insight Group said: “To sum up, both the manufacturing and services sectors weakened in January. Activity in the manufacturing sector shrank. Domestic demand was subdued, and overseas demand largely declined. The labor market remained under pressure. The gauges for input and output prices were stable, while the high prices of some raw materials remained a concern. The level of optimism among service enterprises declined.

“In December and January, the resurgence of Covid-19 in several regions such as Xi’an and Beijing forced local governments to tighten epidemic control measures, which restricted production, transportation and sales of goods. It has become more evident that China’s economy is straining under the triple pressures of contracting demand, supply shocks and weakening expectations.”

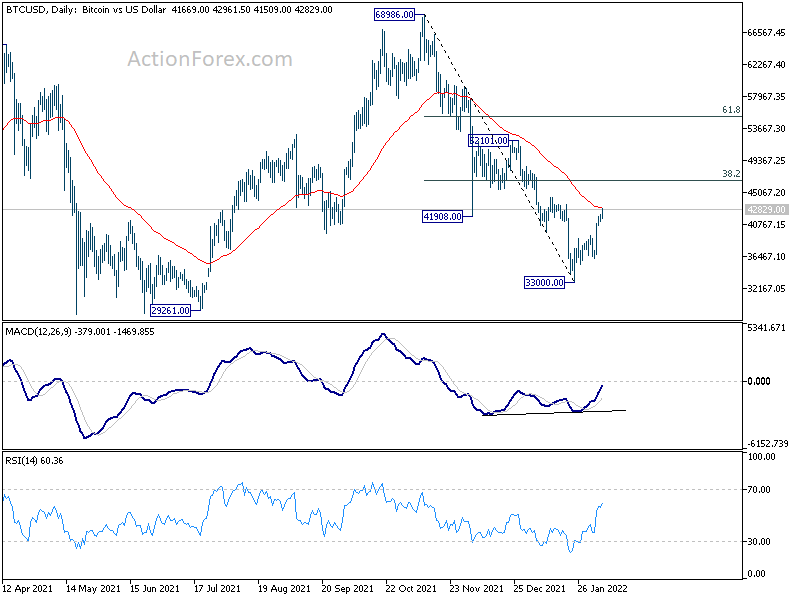

Bitcoin back above 40k, next hurdle at 46k

Bitcoin’s rebounded strongly over the week and and it’s now trading back above 42k handle. The decline from 68986 is seen as the first leg of a long term corrective pattern. Such fall should have completed at 33000, on bullish convergence condition in daily MACD.

Rise from 33000 is seen as the second leg of the pattern. Further rally is expected as long as 37309 support holds, back to 38.2% retracement of 68986 to 33000 at 46476. Sustained break there will target 61.8% retracement at 55239 and above. In this case, the even pattern would be a sideway one, with range set between 33000 and 68986.

However, rejection by 46476, or earlier, would argue that it’s developing into a deep correction that should have another down leg through 33000 and even 30k.

US CPI to highlight a relatively light week

US CPI will highlight a relatively light week. So far, Fed officials have tried to talk down the case for a 50bps rate hike at the March 15-16 meeting. Instead, they’d opt for a series of successive rate hikes. But if inflation figures continue to surprise on the upside, some of the hawks might start to change their mind.

Elsewhere, UK GDP data will be a focus. Eurozone Sentix investor confidence, Australia NAB business confidence, New Zealand RBNZ inflation expectations and China Caixin PMI services will also be watched.

Here are some highlights for the week:

- Monday: Australia AiG services, retail sales; China Caixin PMI services; Japan leading indicators; Swiss unemployment rate, foreign currency reserves; Germany industrial production; Eurozone Sentix investor confidence.

- Tuesday: Japan average cash earnings, household spending, current account; Australia NAB business confidence; France trade balance, Italy retail sales; Canada trade balance; US trade balance.

- Wednesday: Australia Westpac consumer sentiment; Japan M2, machine tool orders; New Zealand inflation expectations; Germany trade balance; Italy industrial production.

- Thursday: Japan PPI; UK RICS house price balance; US CPI, jobless claims.

- Friday: New Zealand BusinessNZ manufacturing index; Germany CPI final; UK GDP, production, trade balance; Swiss PPI; US U of Michigan consumer sentiment.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0547; (P) 1.0574; (R1) 1.0628; More….

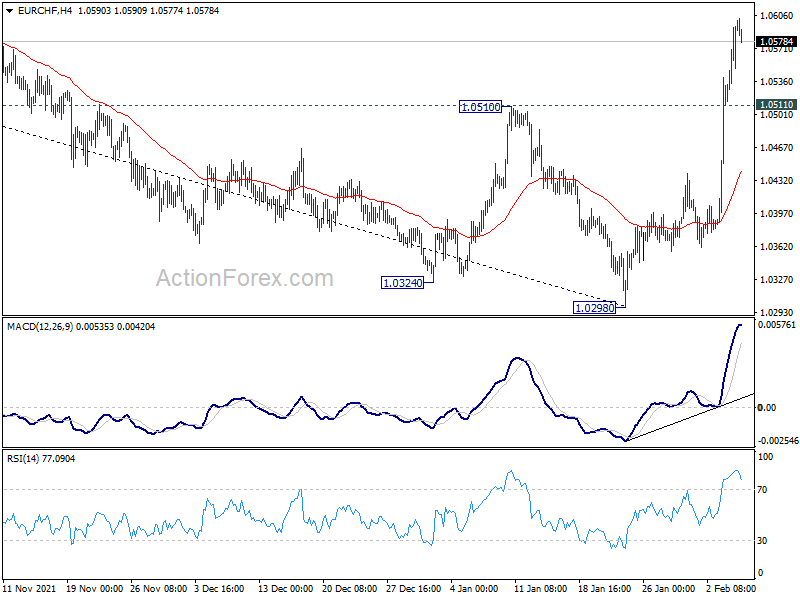

Intraday bias in EUR/CHF remains on the upside at this point. Rise from 1.2098 medium term bottom should target 8.2% retracement of 1.1149 to 1.0298 at 1.0623 first. Sustained trading above there will raise the chance of trend reversal and target 61.8% retracement at 1.0824 next. On the downside, below 1.0511 minor support will turn bias neutral and bring consolidation first, before staging another rally.

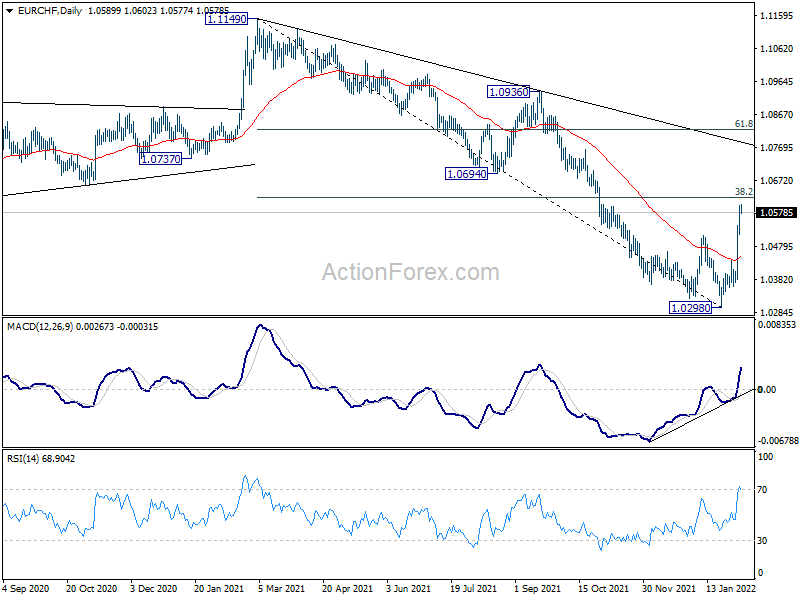

In the bigger picture, current development suggests that a medium term bottom is formed at 1.0298 on bullish convergence condition in daily MACD. Rebound from there is still tentatively viewed part of a corrective pattern. That is, larger down trend from 1.2004 (2018) could still extend through 1.0298 to 61.8% projection of 1.2004 to 1.0505 to 1.1149 at 1.0223. However, sustained trading above 55 week EMA (now at 1.0673) will argue that the down trend is over, and bring stronger rise back to 1.1149 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Services Index Jan | 56.2 | 49.6 | ||

| 01:45 | CNY | Caixin Services PMI Jan | 51.4 | 50.5 | 53.1 | |

| 05:00 | JPY | Leading Economic Index Dec P | 103.1 | 103.2 | ||

| 06:45 | CHF | Unemployment Rate M/M Jan | 2.40% | 2.40% | ||

| 07:00 | EUR | Germany Industrial Production M/M Dec | 0.80% | -0.20% | ||

| 08:00 | CHF | Foreign Currency Reserves (CHF) Jan | 945B | |||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Feb | 15.2 | 14.9 |

for beginner #shorts #crypto #forex #patterns #trading

for beginner #shorts #crypto #forex #patterns #trading