Euro remains in the spotlight in Asian session, as post-ECB rally is extending. Dollar is particularly in pressure as markets are awaiting disappointment from non-farm payroll job data. Yen is currently the second weakest for the week, following the greenback. Aussie is the second strongest, next to Euro, followed by Kiwi. Focuses will turn to non-farm payroll report from the US today, and the reactions from stocks, yields and currencies.

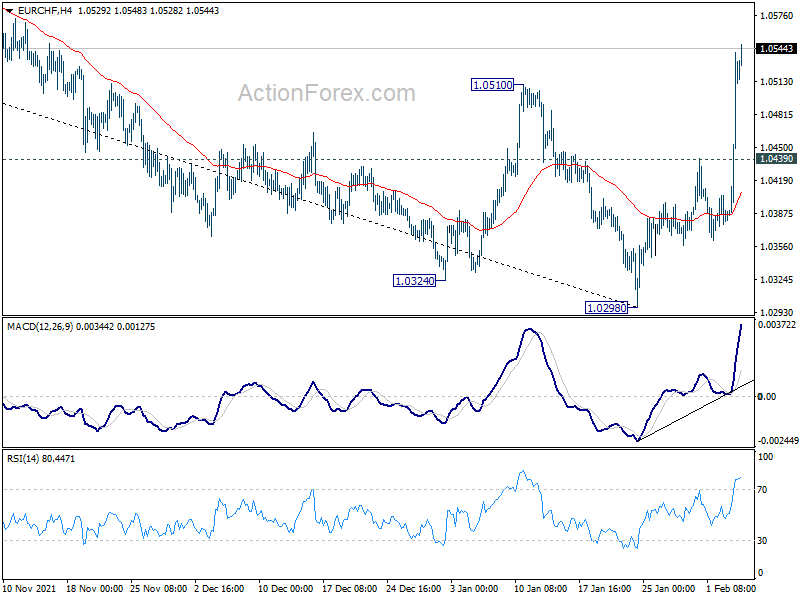

Technically, EUR/GBP’s break of 0.8421 resistance, as well as 55 day EMA, now raises the chance of major bottoming at 0.8282, just ahead of 0.8276 key long term support. Further rally should at least be seen towards 0.8598 resistance to have a test on it. EUR/CHF’s break of 1.0510 resistance also indicates medium term bottoming at 1.0298. Now, focus will be on 1.1482 resistance in EUR/USD. Firm break there will align with the bullish outlook in Euro.

In Asia, at the time of writing, Nikkei is up 0.76%. Hong Kong HSI is up 3.18%. China is still on holiday. Singapore Strait Times is up 0.20%. Japan 10-year yield is up 0.0259 at 0.206, back above 0.2 handle! Overnight, DOW dropped -1.45%. S&P 500 dropped -2.44%. NASDAQ dropped -3.74%. 10-year yield rose 0.061 to 1.827.

Fed Barkin: Interest rates at pre-pandemic levels are place to reassess

Richmond Fed President Thomas Barkin in a Reuters interview, “it is a straightforward call to say we ought to get rates back into better position. It does not feel to me like there is enough information to say holy cow we have to restrain the economy right now.”

Barkin added that the federal funds rate should be raised back to where it was just before the pandemic, that is, a range of 1.50-1.75%. “Pre-pandemic levels are the place to reassess. Where we were pre-pandemic was under every member of the (Federal Open Market Committee’s) assessment of where neutral was,” he said.

“Then we can look around and say do you want to then start to move into the range … where we are starting to restrain?”

BoJ Kuroda: Hard to see inflation sustainably reach target without wages rise

BoJ Governor Haruhiko Kuroda told the parliament today that inflation remains subdued in Japan because of the delay in recovery from pandemic, the public’s deflationary mindset and firms’ assumption that prices won’t rice much.

“In Japan, nominal wages haven’t risen much. It’s hard to see inflation sustainably reach our 2 per cent target unless wages rise in tandem with prices,” he said.

“It’s important to maintain powerful monetary easing to support the economy, and help generate steady wage and price growth.”

Dollar index shaky as NFP might disappoint

US non-farm payroll report is a major focus today. Markets are expecting 150k job growth in January. Unemployment rate is expected to stay unchanged at 3.90%. Average hourly earnings are expected to grow 0.50% mom.

Looking at related economic data, ADP private job was a big disappointment with -301k losses. ISM manufacturing employment ticked up from 53.9 to 54.5. ISM services employment dropped from 54.9 to 52.3. Four-week moving average of initial jobless claims rose from 205k to 255k. All in all, there are prospects of downside surprise in today’s NFP readings, except wages growth.

Dollar index had a steep decline this week, thanks to the strong rebound in EUR/USD. The question now is on whether long term fibonacci level of 61.8% retracement of 102.99 to 89.20 at 97.72 is too much for DXY to overcome. Sustained break of trend line support at around 95.00 will argue that a medium term top was formed at 97.44, on bearish divergence condition in daily MACD. In this case, DXY would likely drop through 94.62 towards 93.43 resistance turned support before finding a bottom. Reactions to today’s NFP could guidance the direction for the rest of the quarter.

Elsewhere

New Zealand building permits rose 0.6% mom in December. RBA monetary policy statement reiterated that the central bank will be patient on interest rates.

Germany factory orders, France industrial output, UK construction PMI and Eurozone retail sales will be released in European session.

Later in the day, Canada will release employment data and Ivey PMI while US will release non-farm payroll employment.

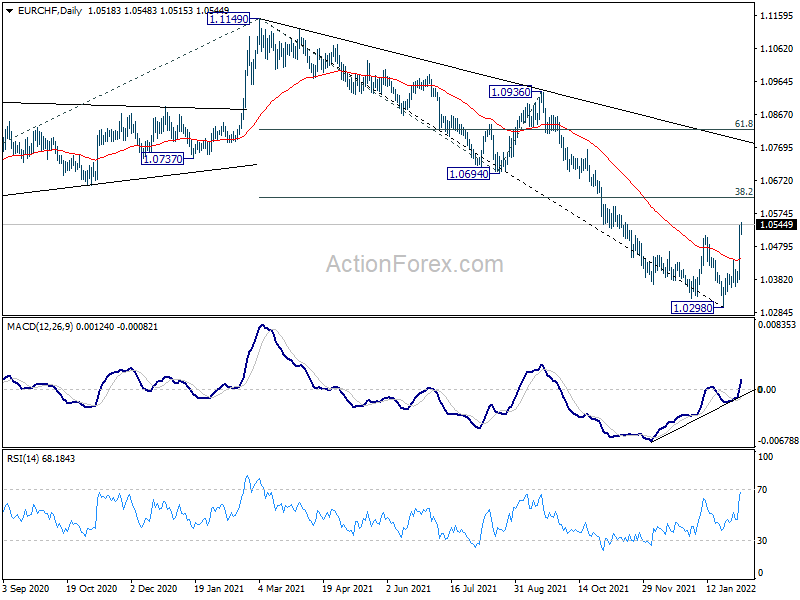

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0427; (P) 1.0485; (R1) 1.0587; More….

EUR/CHF’s rebound from 1.0298 accelerates to as high as 1.0548 so far. The strong break of 1.0510 resistance argues that a medium term bottom was already formed at 1.0298, on bullish convergence condition in daily MACD. Intraday bias is now on the upside for 38.2% retracement of 1.1149 to 1.0298 at 1.0623 first. Sustained trading above there will raise the chance of trend reversal and target 61.8% retracement at 1.0824 next. For now, further rise will remain in favor as long as 1.0439 minor support holds, in case of retreat.

In the bigger picture, current development suggests that a medium term bottom is formed at 1.0298 on bullish convergence condition in daily MACD. Rebound from there is still tentatively viewed part of a corrective pattern. That is, larger down trend from 1.2004 (2018) could still extend through 1.0298 to 61.8% projection of 1.2004 to 1.0505 to 1.1149 at 1.0223. However, sustained trading above 55 week EMA (now at 1.0671) will argue that the down trend is over, and bring stronger rise back to 1.1149 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Dec | 0.60% | 0.60% | ||

| 00:30 | AUD | RBA Monetary Policy Statement | ||||

| 07:00 | EUR | Germany Factory Orders M/M Dec | 0.50% | 3.70% | ||

| 07:45 | EUR | France Industrial Output M/M Dec | 0.50% | -0.40% | ||

| 09:30 | GBP | Construction PMI Jan | 54.3 | 54.3 | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Dec | -0.50% | 1.00% | ||

| 13:30 | USD | Nonfarm Payrolls Jan | 150K | 199K | ||

| 13:30 | USD | Unemployment Rate Jan | 3.90% | 3.90% | ||

| 13:30 | USD | Average Hourly Earnings M/M Jan | 0.50% | 0.60% | ||

| 13:30 | CAD | Net Change in Employment Jan | -121.5K | 54.7K | ||

| 13:30 | CAD | Unemployment Rate Jan | 6.00% | 5.90% | ||

| 15:00 | CAD | Ivey PMI Jan | 55.1 | 45 |

#optionbuying #optionstrading#trading#nifty #scalping #sharemarket #shorts #ytshorts

#optionbuying #optionstrading#trading#nifty #scalping #sharemarket #shorts #ytshorts