Dollar is trying to extend near term rebound with help from surging treasury yields and risk-off sentiments in stocks. But Canadian Dollar is still outshining slightly, as support by oil price rally. Aussie and Kiwi are soft, but selloffs are mainly centered around European majors. Euro is particularly weak as it looks set to resume recent down trend against Sterling and Swiss Franc too.

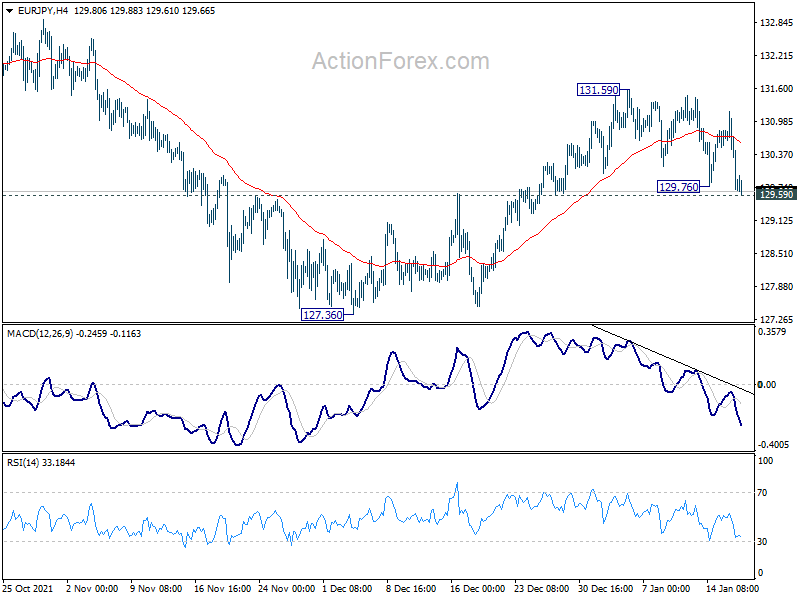

Technically, Yen is also trying to firm up too, even though it’s lagging behind the greenback and Loonie. A focus will be on 129.59 support in EUR/JPY. Sustained break there will dampen our original bullish view of near term reversal. That would indicate that rebound form 127.26 has completed at 131.59 already, and bring deeper fall back to this low. That could be a prelude to more Yen strength elsewhere.

In Asia, at the time of writing, Nikkei is down -2.26%. Hong Kong HSI is up 0.02%. China Shanghai SSE is down -0.29%. Singapore Strait Times is down -0.01%. 10-year JGB yield is down -0.0026 at 0.149. Overnight, DOW dropped -1.51%. S&P 500 dropped -1.84%. NASDAQ dropped -2.60%. 10-year yield rose 0.093 to 1.865.

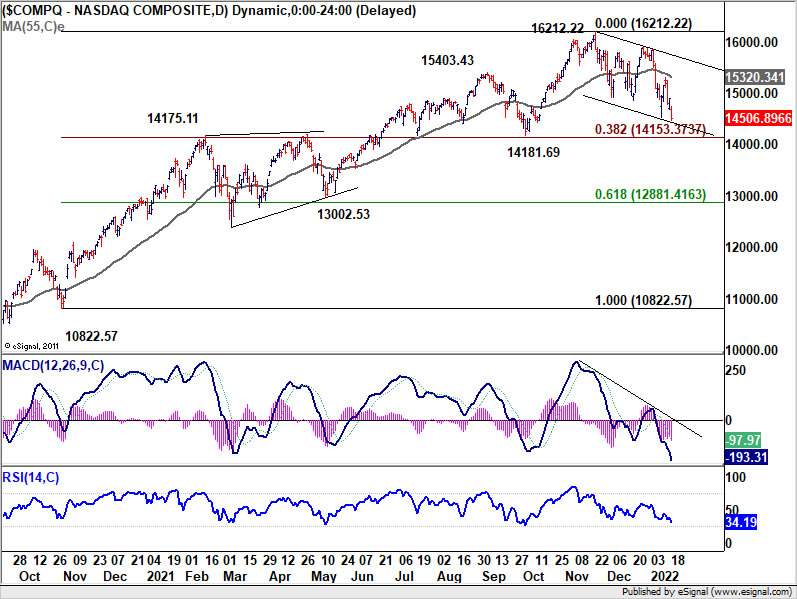

NASDAQ lost -2.6% while 10-yr yield extends up trend

Major US stock indexes, particularly the NASDAQ tumbled sharply overnight, while benchmark treasury yields surged. Investors are still in the process of adjusting to the evolution of a more aggressive Fed in terms of stimulus withdrawal. At the same time, it’s unsure when the no-longer-transitory inflation would start easing down, and Fed’s response to that.

NASDAQ dropped -2.6% to close at 14506.89. The development is not a surprise as price actions from 16212.22 are seen as correcting the up trend from 10822.57 to 16212.22. Deeper fall could be seen. But we’d expect strong support around 14100/14200 to contain downside to bring rebound. The support zone coincides with 14715.11 resistance turned support, 14181.69 structural support, and 38.2% retracement of 10822.57 to 16212.22 at 14153.37. However, sustained break of this level will argue that NASDAQ is already in a larger scale correction.

10-year yield rose 0.093 to close at 1.865. The medium term up trend is back in full force. 2% handle now looks rather approachable. But TNX should start to feel heavy above there. There should be strong resistance from 2.16/18 zone to repel the rally. This is a cluster level of 61.8% projection of 0.398 to 1.765 from 1.343 at 2.187 and 61.8% retracement of 3.248 to 0.398 at 2.159. But then, a strong break there would indicate some substantial underlying development is underway.

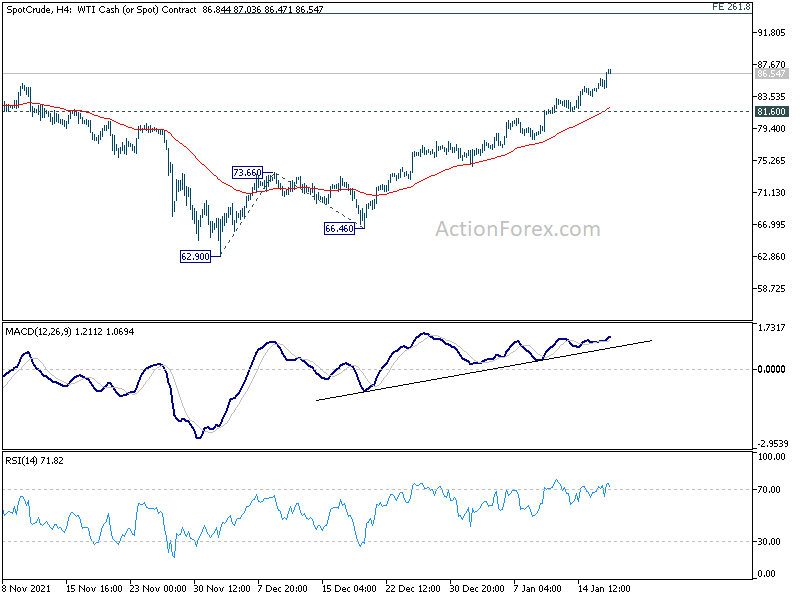

WTI oil hits 7-yr high, EUR/CAD downside breakout

WTI crude oil surged through a key resistance overnight and hit the highest level since 2014. The outage of Turkey’s Kirkuk-Ceyhan pipeline after an explosion was a factor causing concerns over supplies. In the background, there are also geopolitical issues surrounding Russia.

With 85.92 resistance taken out, WTI crude oil is resuming up trend from the 2020 spike low. For the near term, further rally is expected as long as 81.60 support holds. Next target 90 handle. But WTI could try to hit 261.8% projection of 62.90 to 73.66 from 66.46 at 94.62 before topping.

EUR/CAD followed and broke 1.4162 low to resume the down trend from 1.5991. Near term outlook will now stay bearish as long as 1.4357 resistance holds. Next target is 61.8% projection of 1.5096 to 1.4162 from 1.4644 at 1.4067. Firm break there could trigger downside acceleration to 100% projection at 1.3710.

Australia consumer sentiment dropped to 102.2 in Jan, cautiously pessimistic on economic conditions

Australia Westpac-MI consumer sentiment index dropped from 104.3 to 102.2 in January. The -2% decline was much better than the -5.2% fall during the first month of the delta outbreak in New South Wales, the -6.1% drop in Victoria’s second wave in 2020, not to mention the epic -17.7% collapse in early 2020.

The ‘economic conditions, next 12 months’ sub-index dropped -9.6% from 104.9 to 94.8, a swing from “cautious optimism to cautious pessimism”. 55% of respondents, an outright majority, expected mortgage interest rates to rise over the next 12 months. Unemployment Expectations Index increased by 8.2% to 112.7, marking a significant deterioration.

RBA would make a decision on the bond purchases program at the February 1 meeting. Westpac expects the central bank to choose to “scale back rather than full wind down, in response to the sudden emergence of Omicron. But that would depend on the upcoming employment and inflation data.

Looking ahead

UK inflation data are the main focuses in European session, with CPI and PPI featured. Germany will release CPI final. Eurozone will release current account. Later in the day, attention will be on Canada inflation data and wholesale sales. US will release housing starts and building permits.

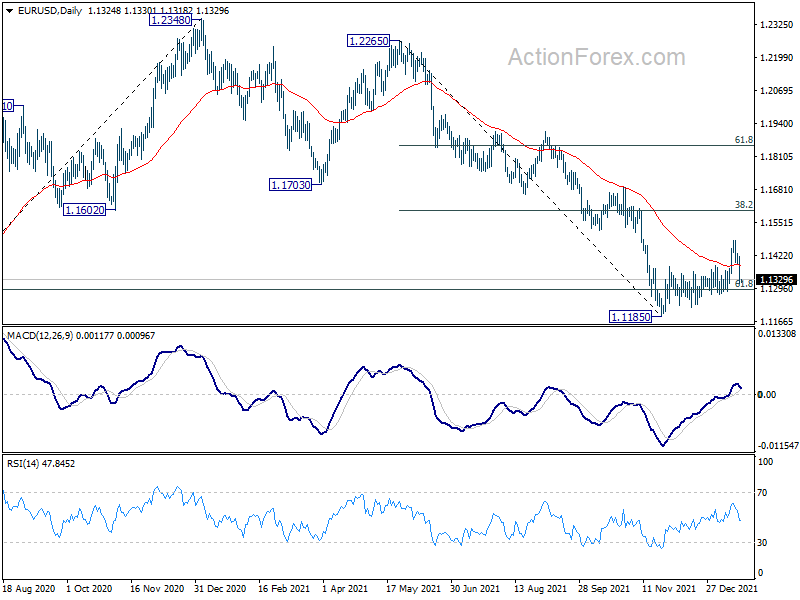

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1288; (P) 1.1355; (R1) 1.1394; More…

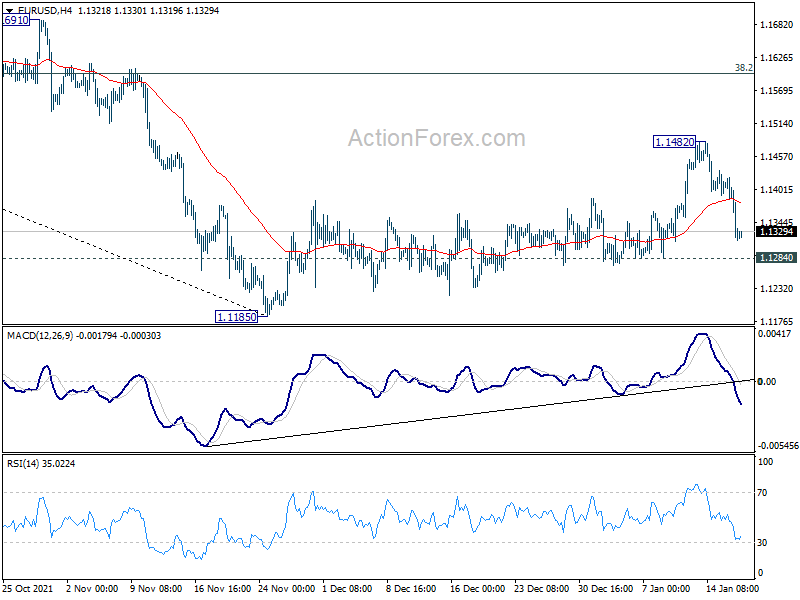

EUR/USD’s fall from 1.1482 accelerates lower today and focus is now on 1.1284 support. Outlook is unchanged that rebound from 1.1185 is seen as corrective move. Break of 1.1284 will argue that larger down trend from 1.2348 is ready to resume. Intraday bias will be back on the downside for retesting 1.1185 low first. Also, in case of another rise, upside should be limited by 38.2% retracement of 1.2265 to 1.1185 at 1.1598 eventually.

In the bigger picture, there are various ways of interpreting the fall from 1.2348 (2021 high). It could be a correction to rise from 1.0635 (2020 low), the fourth leg of a sideway pattern from 1.0339 (2017 low), or resuming long term down trend. In any case, outlook will now stay bearish as long as 1.1703 support turned resistance holds. Sustained break of 61.8% retracement of 1.0635 to 1.2348 at 1.1289 would pave the way back to 1.0635.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:00 | EUR | Germany CPI M/M Dec F | 0.50% | 0.50% | ||

| 07:00 | EUR | Germany CPI Y/Y Dec F | 5.30% | 5.30% | ||

| 07:00 | GBP | CPI M/M Dec | 0.30% | 0.70% | ||

| 07:00 | GBP | CPI Y/Y Dec | 5.20% | 5.10% | ||

| 07:00 | GBP | Core CPI Y/Y Dec | 4.00% | 4.00% | ||

| 07:00 | GBP | PPI Input M/M Dec | 0.70% | 1.00% | ||

| 07:00 | GBP | PPI Input Y/Y Dec | 13.70% | 14.30% | ||

| 07:00 | GBP | PPI Output M/M Dec | 0.60% | 0.90% | ||

| 07:00 | GBP | PPI Output Y/Y Dec | 9.40% | 9.10% | ||

| 07:00 | GBP | PPI Core Output M/M Dec | 0.80% | 0.80% | ||

| 07:00 | GBP | PPI Core Output Y/Y Dec | 8.60% | 7.90% | ||

| 09:00 | EUR | Eurozone Current Account (EUR) Oct | 20.3B | 18.1B | ||

| 13:30 | USD | Housing Starts Dec | 1.65M | 1.68M | ||

| 13:30 | USD | Building Permits Dec | 1.71M | 1.71M | ||

| 13:30 | CAD | Wholesale Sales M/M Nov | 2.80% | 1.40% | ||

| 13:30 | CAD | CPI M/M Dec | 0.20% | 0.20% | ||

| 13:30 | CAD | CPI Y/Y Dec | 4.70% | 4.70% | ||

| 13:30 | CAD | CPI Common Y/Y Dec | 2.10% | 2.00% | ||

| 13:30 | CAD | CPI Median Y/Y Dec | 2.90% | 2.80% | ||

| 13:30 | CAD | CPI Trimmed Y/Y Dec | 3.40% | 3.40% |

#shorts #crypto #forex #trading #patterns

#shorts #crypto #forex #trading #patterns