Yen trades broadly higher in Asian session, following broad based weakness in the stock markets. Nevertheless, mild risk-off sentiment is providing no support to Dollar, nor the hawkish comments from Fed officials. Dollar remains the worst performing one for the week, followed by Swiss Franc. Yen is now the strongest, followed by Aussie and Kiwi. The economic calendar is active today with UK GDP and US retail sales, which could be market moving.

Technically, as Yen appears to be picking up buying, we’ll pay some attention to its pairs. In particular, break of 130.01 minor support in EUR/JPY, and 154.86 minor support in GBP/JPY, will argue that the near term rebound in them are over. We could then see Yen crosses accelerating downward in general, with USD/JPY being dragged further towards 112.52 structural support.

In Asia, at the time of writing, Nikkei is down -1.76%. Hong Kong HSI is down -0.99%. China Shanghai SSE is down -0.59%. Singapore Strait Times is up 0.37%. Japan 10-year yield is up 0.0190 at 0.150. Overnight, DOW dropped -0.49%. S&P 500 dropped -1.42%. NASDAQ dropped -2.51%. 10-year yield dropped -0.014 to 1.711.

Fed Waller: Three rate hikes still a good baseline

Fed Governor Christopher Waller told Bloomberg TV, “three hikes is still a good baseline; we will have to wait and see what inflation looks like in the second half of the year.”

If inflation continues to be high, the case will be made for four, maybe five, hikes,” he said, but added that if inflation abated — as many forecasters including him expect it will — “then you could actually pause and not even go the full three.”

“We can start to let the balance sheet run off earlier and that will take some pressure of longer-end rates and also lead to a tightening in policy,” Waller added.

Fed Daly: Lift off in March is a quite reasonable thing

In a Reuters interview, San Francisco Fed President Mary Daly said, “lifting off in March when you have an unemployment rate of 3.9%, and an inflation rate that’s north of our price stability goal of average 2% inflation, to me seems a quite reasonable thing.” But she didn’t offer her prediction on the number of rate hike needed this year.

Daly also said even with the rate hikes, “we are not bridling the economy and starting to restrain it.” Rate would remain well below the “neutral” level of 2.50%. Meanwhile, once Fed has raised rates once or twice, she said, it should start shrinking the balance sheet as a “predictable” manner.

Fed Harker: Four hikes is not out of question

An a CNBC interview, Philadelphia Fed President Patrick Harker said “we do need to take action on inflation. It is more persistent than we thought a while ago. I’ve been off the ‘transitory’ team for a while now”. “Three [hikes] is what I’ve penciled in, but four is not out of the question in my mind,” he said.

But Harker preferred a slower approach regarding balance sheet run-off. He thinks the Fed should wait until it raises rates “for sake of argument 100 basis points,” or four hikes, before starting the wind down the asset purchases. “I don’t want to do that all at once. I think that’s just the wrong way to go,” he said. “Let’s do them in stages.”

Fed Evans: The committee strongly expecting two, three, four rate increases this year

Chicago Fed President Charles Evans said, “I readily admit – I have to be humble about this – I did not expect the inflation rates that we’re seeing and they have lasted longer than I expected. And because they have lasted longer, I know that we need to take action more quickly than I would have guessed last year.”

“We need to be adjusting monetary policy to something close to neutral,” he said. “The committee very strongly is expecting two, three, four rate increases this year. We’ll see how it plays out.”

Fed Barkin: More aggressive normalization needed if inflation remain elevated and broad-based

Richmond Fed Bank President Thomas Barkin said yesterday, “the closer that inflation comes back to target levels, the easier it will be to normalize rates at a measured pace,”

“But were inflation to remain elevated and broad-based, we would need to take on normalization more aggressively, as we have successfully done in the past,” he added.

Barkin also said labor shortage is a “long lasting phenomenon”, with “baby boomers retiring” and “immigration slowing”. Officials may need to accept that labor force participation is “stagnant”.

On the data front

Japan PPI rose 8.5% yoy in December, below expectation of 8.8% yoy. China trade surplus widened to USD 94.5B in December, above expectation of USD 73.4B.

UK GDP and production will be the main focus in European session, together with trade balance. Eurozone will also release trade balance.

Later in the day, US will release retail sales, import price, industrial production, U of Michigan sentiment and business inventories.

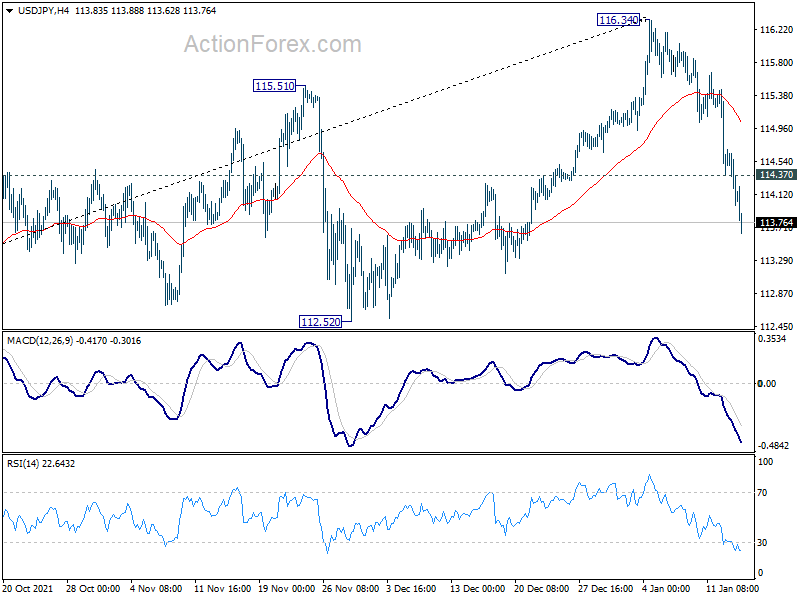

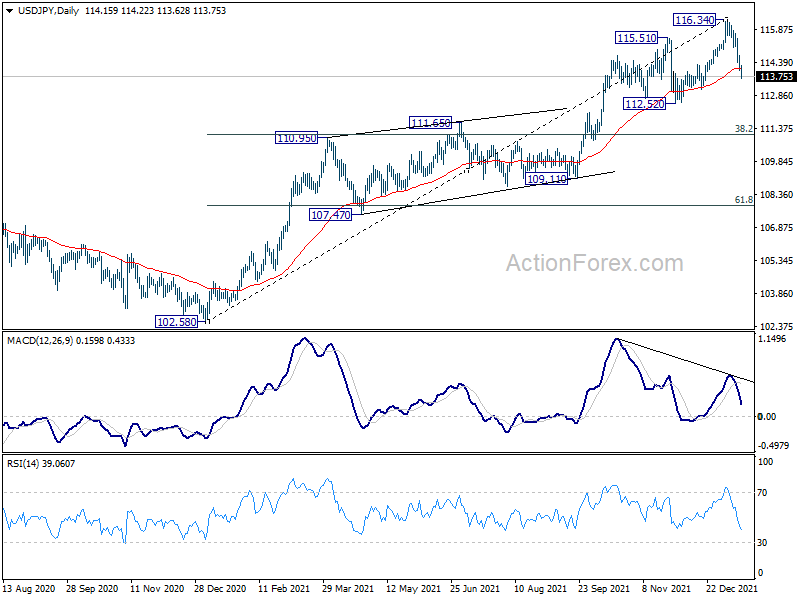

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.88; (P) 114.29; (R1) 114.59; More…

Intraday bias in USD/JPY remains on the downside as fall form 116.34 is accelerating towards 112.52 support. considering bearish divergence condition in in daily MACD, break of 112.52 will confirm that it’s already in correction to the up trend from 102.58. Deeper fall would be seen to 38.2% retracement of 102.58 to 116.34 at 111.08. on the upside, above 114.37 minor resistance will turn intraday bias neutral first.

In the bigger picture, no change in the view that rise from 102.58 is the third leg of the up trend from 101.18 (2020 low). Such rally should target a test on 118.65 (2016 high). Sustained break there will pave the way to 120.85 (2015 high) and raise the chance of long term up trend resumption. However, firm break of 112.52 support will dampen this bullish case and we’ll assess the outlook based on subsequent price actions later.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Dec | 8.50% | 8.80% | 9.00% | 9.20% |

| 02:00 | CNY | Trade Balance (USD) Dec | 94.5B | 73.4B | 71.7B | |

| 02:00 | CNY | Exports (USD) Y/Y Dec | 20.90% | 22% | ||

| 02:00 | CNY | Imports (USD) Y/Y Dec | 19.50% | 31.40% | 31.70% | |

| 02:00 | CNY | Trade Balance (CNY) Dec | 604.69B | 451B | 461B | |

| 02:00 | CNY | Exports (CNY) Y/Y Dec | 17.30% | 16.60% | ||

| 02:00 | CNY | Imports (CNY) Y/Y Dec | 16.00% | 26.00% | ||

| 07:00 | GBP | GDP M/M Nov | 0.40% | 0.10% | ||

| 07:00 | GBP | Manufacturing Production M/M Nov | 0.20% | 0.00% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Nov | -0.30% | 1.30% | ||

| 07:00 | GBP | Industrial Production M/M Nov | 0.20% | -0.60% | ||

| 07:00 | GBP | Industrial Production Y/Y Nov | 0.50% | 1.40% | ||

| 07:00 | GBP | Index of Services 3M/3M Nov | 0.50% | 1.10% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Nov | -14.2B | -13.9B | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Nov | 1.6B | 2.4B | ||

| 13:30 | USD | Retail Sales M/M Dec | 0.00% | 0.30% | ||

| 13:30 | USD | Retail Sales ex Autos M/M Dec | 0.20% | 0.30% | ||

| 13:30 | USD | Import Price Index M/M Dec | 0.30% | 0.70% | ||

| 14:15 | USD | Industrial Production M/M Dec | 0.40% | 0.50% | ||

| 14:15 | USD | Capacity Utilization Dec | 76.90% | 76.80% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Jan P | 70.6 | 70.6 | ||

| 15:00 | USD | Business Inventories Nov | 1.00% | 1.20% |

#shorts #crypto #forex #trading #patterns

#shorts #crypto #forex #trading #patterns