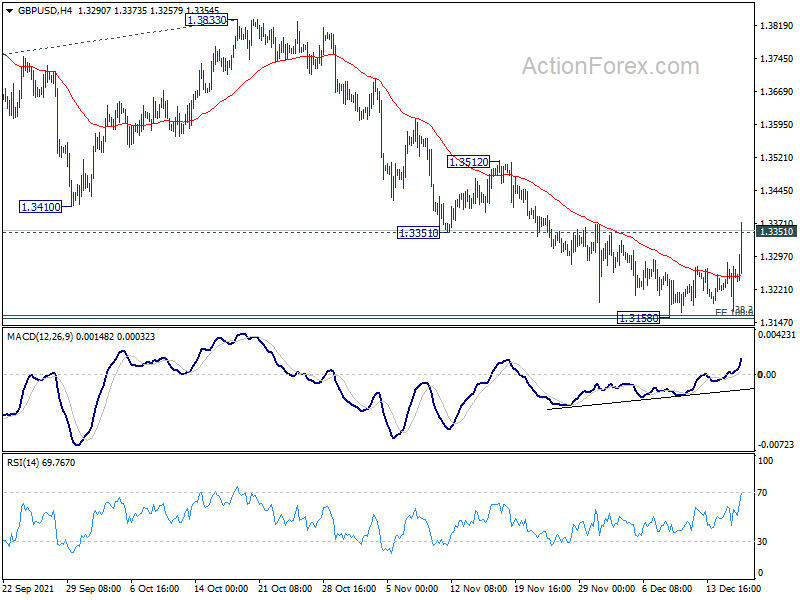

Sterling rises broadly after BoE surprised the markets by raising interest rates and maintains a hawkish tone. Solid risk-on sentiment as well as strong job data boosts Aussie as the second strongest. Euro is not performing badly after ECB announces to end PEPP net purchases in March. Indeed, the common currency is trying to catch up with the Pound. On the other hand, Dollar is trading broadly lower despite Fed’s hawkish turn yesterday. Yen is even weaker while Swiss Franc is not too far behind.

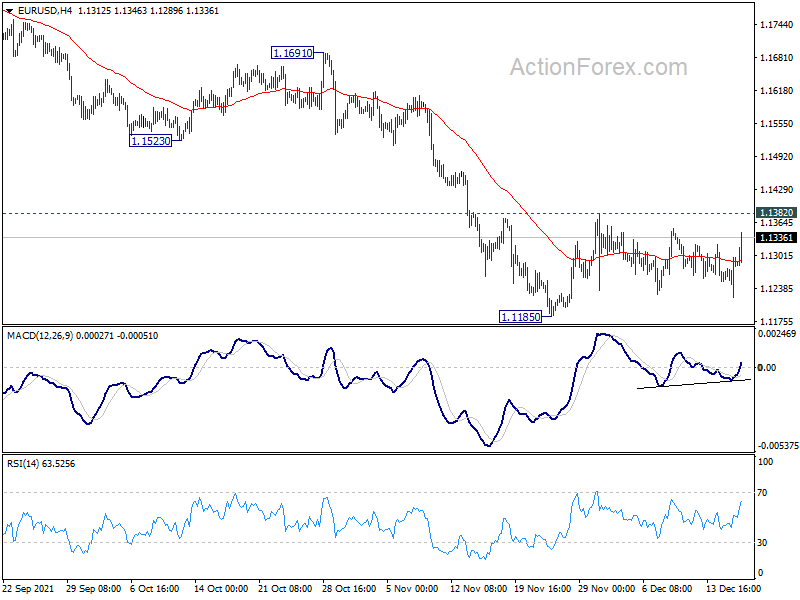

Technically, near term bullishness in Sterling and Aussie is rather apparent with break of resistance levels against Dollar. We’ll now see if EUR/USD would break through 1.1382 resistance to give Dollar another punch. 0.9156 support in USD/CHF is another level to watch.

In Europe, at the time of writing, FTSE is up 0.95%. DAX is up 1.54%. CAC is up 1.33%. Germany 10-year yield is up 0.0469 at -0.312. Earlier in Asia, Nikkei rose 2.13%. Hong Kong HSI rose 0.23%. China Shanghai SSE rose 0.75%. Singapore Strait Times rose 0.45%. Japan 10-year JGB yield dropped -0.0048 to 0.045.

US initial jobless claims rose back to 204k, continuing claims dropped to 1.85m

US initial jobless claims rose 18k to 206k in the week ending December 11, above expectation of 192k. Four-week moving average of initial claims dropped -16k to 204k, lowest level since November 15, 1969.

Continuing claims dropped -154k to 1845k in the week ending December 4, lowest since March 14, 2020. Four-week moving average of continuing claims dropped -66k to 1963k, lowest since March 14, 2020 too.

Also released, Philly Fed manufacturing index dropped from 39 to 15.4 in December, below expectation of 30.0. Housing starts rose to 1.68m annualized rate while building permits rose to 1.71m.

BoE hikes to 0.25%, some modest tightening still needed

BoE decided to raise the Bank Rate by 0.15 bps to 0.25%, with 8-1 vote. Silvana Tenreyro was the only MPC member voted for no change. The MPC also voted unanimously to maintain the stock of government bond purchases at GBP 875B, and corporate bond purchases at GBP 20B.

The central bank said it will review developments, including the impact of Omicron, in the February Monetary Policy Report, with focus on medium term prospects for inflation. There are “two-sided risks around inflation outlook in the medium term”. But, “some modest tightening of monetary policy over the forecast period is likely to be necessary to meet the 2% inflation target sustainably”.

UK PMI composite dropped to 53.2, hit once again by COVID-19

UK PMI Manufacturing dropped from 58.1 to 57.6 in December, matched expectations. PMI Services dropped sharply from 58.5 to 53.2, well below expectation of 57.5, a 10-month low. PMI Composite dropped from 57.6 to 53.2, also a 10-month low.

Chris Williamson, Chief Business Economist at IHS Markit, said: “The flash PMI data show the UK economy being hit once again by COVID-19, with growth slowing sharply at the end of the year led by a steep drop in spending on services by households. Some brighter news came through from manufacturing, where an easing of supply chain delays helped lift production growth, but more importantly also helped take some upward pressure off prices to hint at a peaking of inflation.”

ECB to end net PEPP purchases in March, temporarily raise APP purchases in Q2 and Q3

ECB announced to “discontinue”net asset purchases under the pandemic emergency purchase programme (PEPP) at the end of March 2022. Reinvestment horizon for PEPP will be extended until at least the end of 2024.

Monthly net asset purchases under the original asset purchase programme (APP) will be doubled to EUR 40B in Q2, then slow to EUR 30B in Q3, and back to EUR 20B in Q4 for “as long as necessary”.

Meanwhile, main refinancing rate, marginal lending facility rate and deposit facility rate were held unchanged at 0.00%, 0.25%, and -0.50% respectively. Forward guidance is maintained that there will be a “transitory period in which inflation is moderately above target.”

Eurozone PMI composite dropped to 53.4, another blow from COVID-19

Eurozone PMI Manufacturing dropped from 58.4 to 58.0 in December, a 10-month low but above expectation of 57.7. PMI Services dropped from 55.9 to 53.3, an 8-month low and missed expectations of 54.2. PMI Composite dropped from 55.4 to 53.4, a 9-month low.

Chris Williamson, Chief Business Economist at IHS Markit said: “The eurozone economy is being dealt yet another blow from COVID-19… Germany is being especially hard hit, seeing the economy stall for the first time in a year-and-a-half, but the growth slowdown is broad based across the region.

“Encouragement comes from the manufacturing sector, where the strain on supply chains is showing some signs of easing, in turn helping to revive factory production… Easing supply constraints have alleviated some of the upward pressures on inflation, though the overall rate of price increase in December was still the second-highest on record. While inflation could soon peak, the rate of increase remains elevated.”

Germany PMI Manufacturing rose from 57.4 to 57.9 in December, above expectation of 57.0. PMI Services dropped sharply from 52.7 to 48.4, below expectation of 51.0, back in contraction, and a 10-month low. PMI Composite dropped from 52.2 to 50.0, an 18-month low.

France PMI Manufacturing dropped from 55.9 to 54.9 in December, below expectation of 55.3. PMI Services dropped from 57.4 to 57.1, above expectation of 55.6. PMI Composite dropped from 56.1 to 55.6.

SNB stands pat, upgrades 2021 and 2022 inflation forecasts

SNB kept the sight deposits rate unchanged at -0.75% as widely expected. It also remained “remains willing to intervene in the foreign exchange market as necessary, in order to counter upward pressure on the Swiss franc”. The Swiss Franc “remains highly valued”.

The new conditional inflation forecasts for 2021 and 2022 were revised higher “primarily due to higher import prices, all all for oil products and for goods affected by global supply bottlenecks”. New forecast stands at 0.6% for 2021, 1.0% for 2022 and 0.6% for 2023, comparing to September forecasts of 0.5% for 2021, 0.7% for 2022, and 0.6% for 2023. They based on assumption that policy rate remains at -0.75% over the entire forecast horizon.

As for the economy, the baseline scenario is a “continuation of the economic recovery next year”. SNB expects GDP growth of around 3% for 2022 while unemployment is “likely to decline again somewhat”.

Japan exports rose 20.5% yoy in Nov, imports surged 43.8% yoy to record

Japan’s exports rose 20.5% yoy to JPY 7367B in November. That’s the ninth straight months of increase, helped by 4.1% rise in auto shipments. Exports to China rose 155.0% yoy. Imports rose 43.8% yoy to JPY 8322B. That’s the largest amount on record since 1979, jacked up by 144.1% yoy rise in fuels. Trade surplus came in at JPY 955B.

In seasonally adjusted terms, exports rose 5.3% mom to JPY 7385B. Imports rose 5.9% mom to 7872B. Trade balance reported a deficit of JPY -487B.

Japan PMI manufacturing dropped to 53.3, recovery sustained with softening momentum

Japan PMI Manufacturing dropped from 54.0 to 53.3 in December. PMI Services dropped from 53.0 to 51.1. PMI Composite dropped from 53.3 to 51.8.

Annabel Fiddes, Economics Associate Director at IHS Markit, said: “The latest Flash PMI data showed that the Japanese private sector recovery was sustained in December, rounding off the best quarterly performance since Q4 2018. However, both manufacturers and services companies signalled softer rates of output and new order growth compared to November, to suggest a softening of momentum.”

Australia employment rose 366.1k in Nov, unemployment dropped sharply to 4.6%

Australia employment rose 366.1k in November, above expectation of 200k. Full-time employment rose 128.3k. Part-time employment rose 237.8k. Unemployment rate dropped sharply from 5.2% to 4.6%, better than expectation of 5.0%. Participation rate also jumped 1.4% to 66.1%. Monthly hours worked in all job rose 4.5% mom.

Also released, PMI manufacturing dropped from 59.2 to 57.4 in December. PMI Services dropped from 55.7 to 55.1. PMI Composite dropped from 55.7 to 54.9.

New Zealand GDP contracted -3.7% qoq in Q3, better than expectation

New Zealand GDP dropped -3.7% qoq in Q3, better than expectation of -4.3% qoq. For the year, GDP contracted -0.3% yoy, versus expectation of -1.6% yoy. Services industries dropped -2.7% qoq. Goods-producing industries dropped -7.3% qoq. Primary industries dropped -3.1% qoq.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3196; (P) 1.3239; (R1) 1.3306; More…

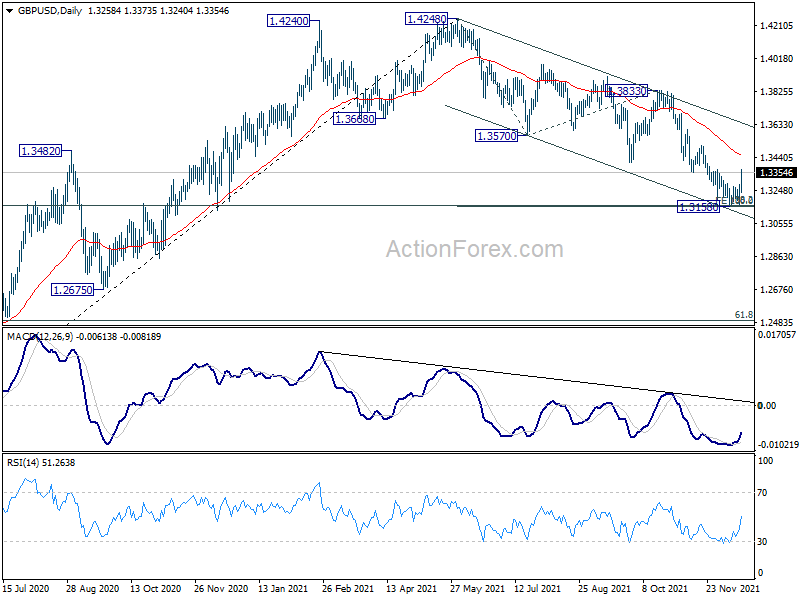

GBP/USD’s break of 1.3351 support turned resistance indicates that a short term bottom was formed at 1.3158 already. More importantly, it’s the first sign that correction from 1.4248 has complete with three waves down to 1.3158, after defending 1.3164 key medium term fibonacci level. Intraday bias is back on the upside for 1.3570 support turned resistance first. Firm break there will affirm this bullish case. On the downside, however, sustained break of 1.3164 will carry larger bearish implications.

In the bigger picture, immediate focus is now on 38.2% retracement of 1.1409 to 1.4248 at 1.3164. Sustained break there will argue that whole rise from 1.1409 has completed at 1.4248, after rejection by 1.4376 long term resistance. That will revive some medium term bearishness and and target 61.8% retracement at 1.2493. However, strong rebound from current level will revive that case and up trend from 1.1409 is still in progress, and probably ready to resume.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | GDP Q/Q Q3 | -3.70% | -4.30% | 2.80% | 2.40% |

| 21:45 | NZD | GDP Y/Y Q3 | -0.30% | -1.60% | 17.40% | 17.90% |

| 22:00 | AUD | Manufacturing PMI Dec P | 57.4 | 59.2 | ||

| 22:00 | AUD | Services PMI Dec P | 55.1 | 55.7 | ||

| 23:50 | JPY | Trade Balance (JPY) Nov | -0.49T | -0.32T | -0.44T | -0.42T |

| 00:30 | AUD | Employment Change Nov | 366.1K | 200.0K | -46.3K | -56.0K |

| 00:30 | AUD | Unemployment Rate Nov | 4.60% | 5.00% | 5.20% | |

| 08:15 | EUR | France Manufacturing PMI Dec P | 54.9 | 55.3 | 55.9 | |

| 08:15 | EUR | France Services PMI Dec P | 57.1 | 55.6 | 57.4 | |

| 08:30 | EUR | Germany Manufacturing PMI Dec P | 57.9 | 57 | 57.4 | |

| 08:30 | EUR | Germany Services PMI Dec P | 48.4 | 51 | 52.7 | |

| 08:30 | CHF | SNB Interest Rate Decision | -0.75% | -0.75% | -0.75% | |

| 09:00 | EUR | Eurozone Manufacturing PMI Dec P | 58 | 57.7 | 58.4 | |

| 09:00 | EUR | Eurozone Services PMI Dec P | 53.3 | 54.2 | 55.9 | |

| 09:30 | GBP | Manufacturing PMI Dec P | 57.6 | 57.6 | 58.1 | |

| 09:30 | GBP | Services PMI Dec P | 53.2 | 57.5 | 58.5 | |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Oct | 2.4B | 5.7B | 6.1B | |

| 12:00 | GBP | BoE Interest Rate Decision | 0.25% | 0.10% | 0.10% | |

| 12:00 | GBP | BoE Asset Purchase Facility | 875B | 875B | 875B | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 8–0–1 | 2–0–7 | 2–0–7 | |

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0–0–9 | 0–3–6 | 0–3–6 | |

| 12:45 | EUR | Eurozone ECB Interest Rate Decision | 0.00% | 0.00% | 0.00% | |

| 13:30 | EUR | ECB Press Conference | ||||

| 13:30 | CAD | ADP Employment Change Nov | 231.8K | 65.8K | ||

| 13:30 | CAD | Wholesale Sales M/M Oct | 1.40% | 1.50% | 1.00% | |

| 13:30 | USD | Initial Jobless Claims (Dec 10) | 206K | 192K | 184K | 188K |

| 13:30 | USD | Housing Starts Nov | 1.68M | 1.57M | 1.52M | |

| 13:30 | USD | Building Permits Nov | 1.71M | 1.67M | 1.65M | |

| 13:30 | USD | Philadelphia Fed Manufacturing Dec | 15.4 | 30 | 39 | |

| 14:15 | USD | Industrial Production M/M Dec | 0.70% | 1.60% | ||

| 14:15 | USD | Capacity Utilization Dec | 76.70% | 76.40% | ||

| 14:45 | USD | Manufacturing PMI Dec P | 58.3 | |||

| 14:45 | USD | Services PMI Dec P | 58 | |||

| 15:30 | USD | Natural Gas Storage | -85B | -59B |

#optionbuying #optionstrading#trading#nifty #scalping #sharemarket #shorts #ytshorts

#optionbuying #optionstrading#trading#nifty #scalping #sharemarket #shorts #ytshorts