The markets are rather quiet in Asian session. Stock indexes are trading higher but no follow through buying is seen. In the forex markets, major pairs and crosses are stuck inside Friday’s range, with commodity currencies a touch firmer. Activity could remain subdued with an empty calendar for today. Yet, volatility is guaranteed with five major central bank meeting scheduled for the week, plus a lot of important data ahead.

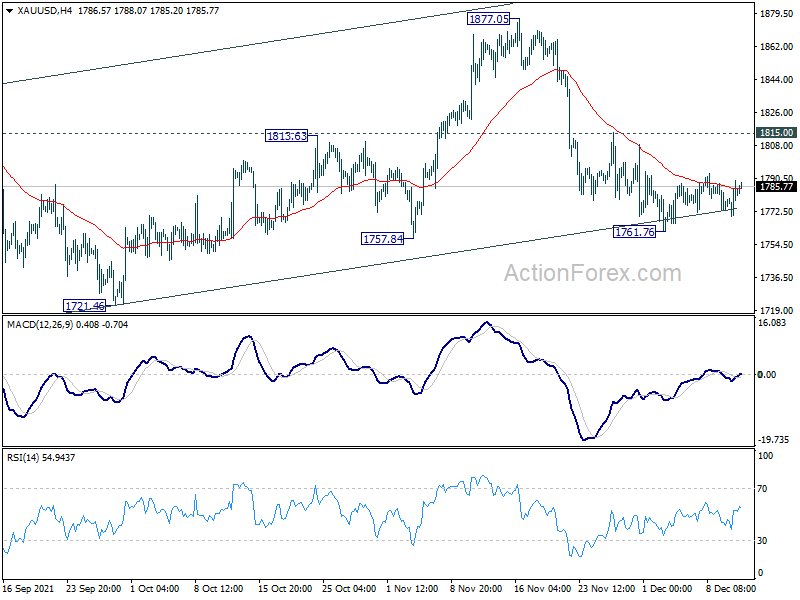

Technically, we continue to pay attention for signs of breakout in Dollar. In particular, we’re talking about ranges of 1.1185/1382 in EUR/USD, 112.52/113.94 in USD/JPY and 0.9156/0.9274 in USD/CHF. At the same time, we’ll monitor the next movement in Gold to confirm Dollar’s direction. For now, more decline is expected in Gold as long as 1815 minor resistance holds. Break of 1761.76 will resume the fall from 1877.05 towards 1721.46 support next.

In Asia, at the time of writing, Nikkei is up 0.87%. Hong Kong HSI is up 1.03%. China Shanghai SSE is up 1.00%. Singapore Strait Times is up 0.29%. Japan 10-year JGB yield is down -0.0025 at 0.054.

Japan Tankan large manufacturing index unchanged a 18, outlook ticked down

According to the BoJ’s Tankan survey in Q4, large manufacturing index was unchanged at 18, below expectation of 19. Large manufacturing outlook dropped from 14 to 13, below expectation of 19.

Non-manufacturing index rose sharply from 2 to 9, well above expectation of 6. That’s the highest reading since December 2019. Non-manufacturing outlook also rose from 3 to 8, but missed expectation of 10.

Output price index for large enterprises jumped from 10 to 16, highest since the 1980s. Input prices index also rose from .37 to 49, highest since 2008.

Large firms are expecting to increased capital spending by 9.3% in the year ending in March 2022, lower than expectation of 9.8%.

Also released, machine orders rose 3.8% mom in October, above expectation of 2.1% mom. That’s the first rise in three months.

NZIER: NZ inflation to stay above RBNZ target mid-point through to 2025

NZIER lowered near-term economic outlook of New Zealand, reflecting the impact of pandemic restrictions, “which turned out to persist for longer than initially expected”. For the year to March 2022, GDP growth was revised down from 4.5% to 4.3%. But growth for 2023 was revised up from 4.5% to 4.6%.

Growing capacity pressures are contributing to a sharp rise in inflation. CPI is expected to 5.1% in 2022 (up from prior estimate of 3.0%), and remain elevated above RBNZ’s inflation target mid-point of 2% “through to 2025”.

NZD trade-weighted index forecast was revised lower “partly reflecting market disappointment at smaller than expected interest rate increased from the Reserve Bank in its November meeting.” NZD TWI is expected to peak at 74.5 for the year to March 2023 (revised down from 74.8), then ease to 72.7 in 2025.

Fed, ECB, BoE, SNB, BoJ, plus lots of data

Five major central bank will meet this week. Fed Chair Jerome Powell has already indicated that FOMC will consider faster pace of tapering. That would give Fed more flexibility to raise interest rates earlier to counter inflation, which is at multi-decade high. Fed’s new economic projections and more importantly the dot-plot of interest rate expectations would be watched closely.

ECB will need to signal what it’s going to with the Pandemic Emergency Purchase Programme next. It’s reported that the PEPP will still end in March as scheduled. But ECB would probably boost the regular Asset Purchase Programme temporary to smooth out the transition. The boost could come in as a form of envelope until the end of the year. Also, it could just lift the monthly purchases for a short period of time, and reveal later.

BoE officials had been talking up rate hike even before November meeting. But the outlook changed drastically after the arrival of Omicron and return to restrictions. Even a known hawk Michael Sanders turned cautious, preferring to wait and see Omicron’s impact first. So, it’s more likely that BoE will keep powder dry for the moment.

SNB is generally expected to keep monetary policy unchanged, and maintain that negative interest rate and the willingness to intervene remain necessary. BoJ will keep the parameters of the QQE with Yield Curve Control unchanged, but it might start scaling back some emergency funding.

The economic calendar is also ultra-busy. Here are some highlights for the week:

- Monday: Japan Tankan survey.

- Tuesday: Australia NAB business confidence; UK employment; Swiss PPI; Eurozone industrial production; US PPI.

- Wednesday: New Zealand current account; Australia Westpac consumer sentiment; China retail sales, fixed asset investment, industrial production; Japan tertiary industry index; UK CPI, PPI; Canada CPI, manufacturing sales; US retail sales, Empire state manufacturing, import price index, business inventories, NAHB housing index, FOMC rate decision.

- Thursday: New Zealand GDP;Australia PMIs, employment; Japan trade balance, PMI manufacturing; Eurozone PMIs; ECB rate decision; UK PMIs, BoE rate decision; SNB rate decision; US Philly Fed survey, jobless claims, building permits and housing starts, industrial production, PMIs.

- Friday: New Zealand ANZ business confidence; BoJ rate decision; Germany PPI, Ifo business climate; UK retail sales; Eurozone CPI final.

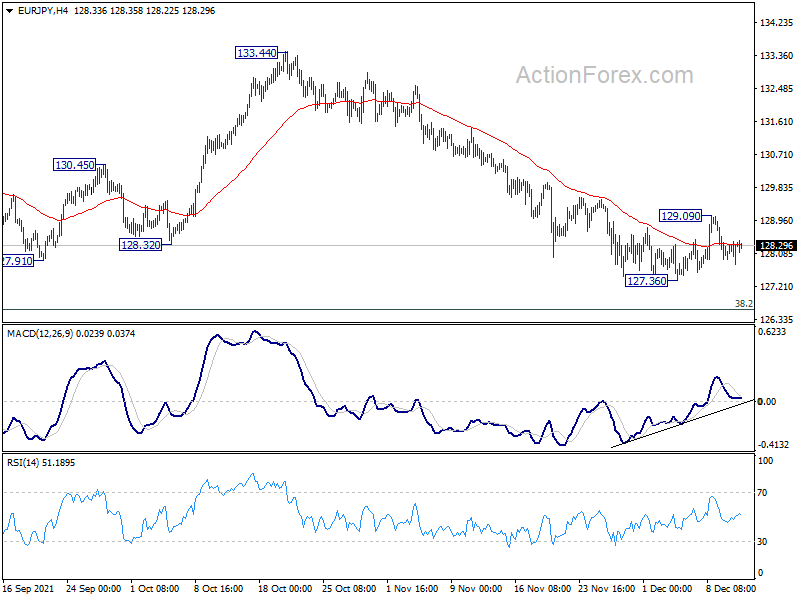

EUR/JPY Daily Outlook

Daily Pivots: (S1) 127.97; (P) 128.18; (R1) 128.55; More….

Intraday bias in EUR/JPY remains neutral at this point, as consolidation from 127.36 is extending. On the downside, break of 127.36 will resume larger pattern from 134.11 to 126.58 medium term fibonacci level. We’d look for some support from there to bring rebound. But sustained break of 126.58 will carry larger bearish implications. On the upside, break of 129.09 will bring stronger rebound to 55 day EMA (now at 129.66) and above.

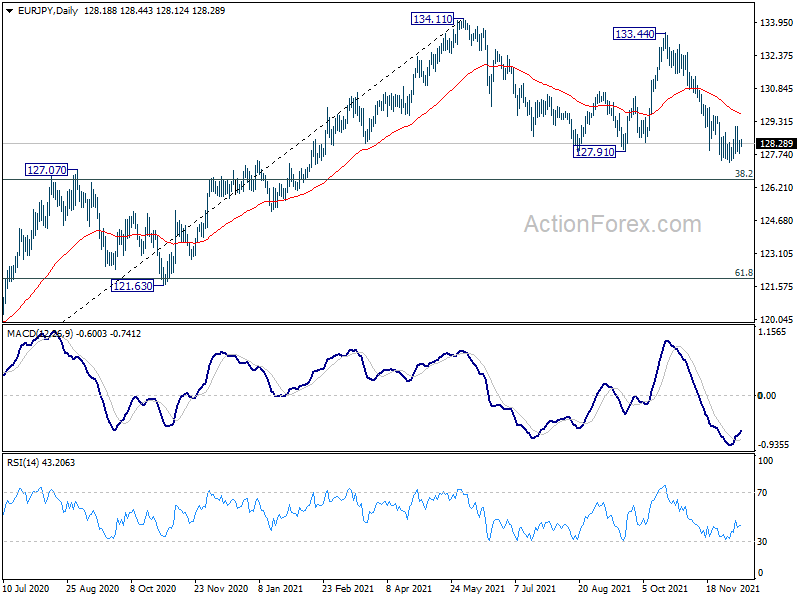

In the bigger picture, as long as 38.2% retracement of 114.42 (2020 low) to 134.11 at 126.58 holds, up trend from 114.42 is still in favor to continue. Break of 134.11 will target long term resistance at 137.49 (2018 high). However, sustained break of 126.58 will raise the chance of medium term bearish reversal. In this case, deeper decline would be seen to 61.8% retracement at 121.94, and possibly below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Tankan Large Manufacturing Index Q4 | 18 | 19 | 18 | |

| 23:50 | JPY | Tankan Non-Manufacturing Index Q4 | 9 | 6 | 2 | |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q4 | 13 | 19 | 14 | |

| 23:50 | JPY | Tankan Non – Manufacturing Outlook Q4 | 8 | 10 | 3 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q4 | 9.30% | 9.80% | 10.10% | |

| 23:50 | JPY | Machinery Orders M/M Oct | 3.80% | 2.10% | 0.00% | |

| 17:00 | GBP | Financial Stability Report |