Risk-on sentiment is gather steam today with major European indexes trading broadly higher, while US futures point to higher open. WTI crude oil is also up another 2.5% and is back above 70 handle. In the currency markets, Australian Dollar is leading the rebound in commodity currencies, with help from a slightly more upbeat RBA statement. European majors are the worst performers together with Yen, while Dollar is mixed.

Technically, focus is now on some European-commodity crosses with today’s development. In particular, EUR/CAD is heading back to 1.4162 support after earlier rejection by 1.4580 support turned resistance. Break will resume larger down trend and target 100% projection of 1.5783 to 1.4580 from 1.5096 at 1.3893.

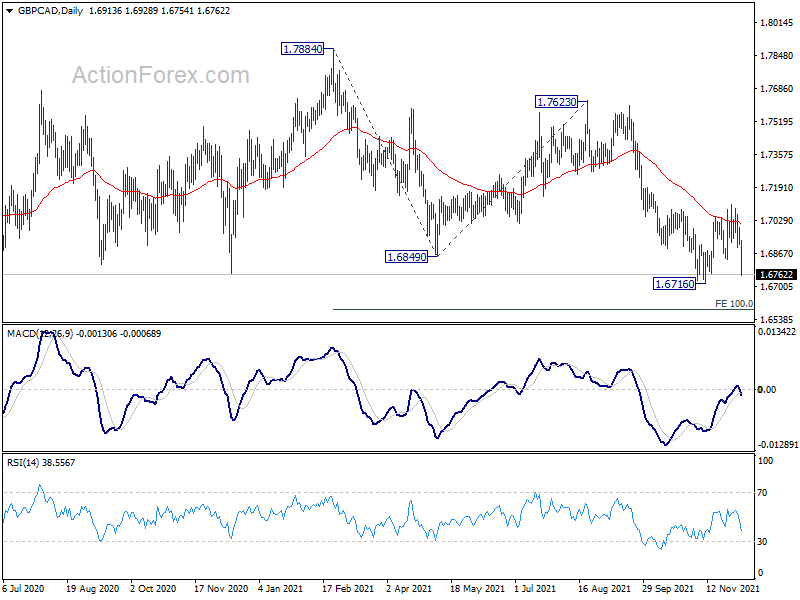

Also, GBP/CAD is diving back to 1.6716 support after rejection by 55 day EMA. Break will resume larger down trend for 100% projection of 1.7884 to 1.6849 from 1.7623 at 1.6588.

In Europe, at the time of writing, FTSE is up 1.19%. DAX is up 2.08%. CAC is up 2.34%. Germany 10-year yield is up 0.0219 at -0.365. Earlier in Asia, Nikkei rose 1.89%. Hong Kong HSI rose 2.72%. China Shanghai SSE rose 0.16%. Singapore Strait Times rose 0.59%. Japan 10-year JGB yield rose 0.139 to 0.055.

US exports rose 8.1% in Oct, import rose 0.9%, trade deficit narrowed

US exports rose 8.1% to USD 223.6B in October. Imports rose 0.9% to USD 290.7B. Trade deficit narrowed to USD -67.1B, from USD -81.4B, but widened than expectation of USD -66.9B. The figure reflected a decrease in goods deficit to USD -83.9B and increased in services surplus to USD 16.8B. Year-to-date, trade deficit increased 29.7% from the same period in 2020.

Canada trade surplus rose to CAD 2.1B in Oct, exports and imports surged to record

Canada exports rose 6.4% to reach a record CAD 56.2B in October. Exports grew in 8 of 11 product sections. The combined gains in exports of motor vehicles and parts and energy products accounted for almost 80% of the total growth.

Imports rose 5.3% to record CAD 54.1B. Gains were observed in 7 of 11 product sections. Motor vehicles and parts responsible for almost two-thirds of the monthly increase.

Trade surplus widened from CAD 1.4B to CAD 2.1B. well above expectation of CAD 1.6B. That’s also the largest surplus so far in 2021.

German ZEW dropped to 29.9, suffering noticeably from latest pandemic development

Germany ZEW Economic Sentiment dropped to 29.9 in December, down from 31.7, but beat expectation of 25.3. Current Situation index dropped sharply to -7.4, down from 12.5. That’s the first negative reading since June. Inflation Expectations dropped -19.0 pts to -33.3. 56.6% of experts expected inflation rate to decline in the next six months.

Eurozone ZEW Economic Sentiment rose from 25.9 to 26.8, above expectation of 23.5. Current Situation indicator dropped -13.9 pts to -2.3.

“The German economy is suffering noticeably from the latest developments in the COVID-19 pandemic. Persisting supply bottlenecks are weighing on production and retail trade. The decline in economic expectations shows that hopes for much stronger growth in the next six months are fading. Especially the earnings expectations of export-oriented and consumer-related industries are assessed more negatively,” comments ZEW President Professor Achim Wambach on current expectations.

Also from Germany, industrial production rose 2.8% mom in October, well above expectation of 0.8% mom.

France trade deficit widened to EUR -7.5B in October. Swiss unemployment rate dropped to 2.5% in November. Swiss foreign currency reserves rose to CHF 1006B in November.

Eurozone GDP growth finalized at 2.2% qoq in Q3, EU at 2.1% qoq

According to the final revised data, Eurozone GDP grew 2.2% qoq 3.0% yoy in Q3. GDP volumes remained -0.3% below pre-pandemic level in Q4 2019. Household consumption rose 4.1%. Government final consumption expenditure rose 0.3%. Gross fixed capital formation dropped -0.9%. Exports rose 1.2%. Imports rose 0.7%.

Household final consumption expenditure in Eurozone rose 2.1%. Government final expenditure rose 0.1%. Gross fixed capital formation dropped -0.2%. The contributions from external balance were positive while change in inventories was slightly negative.

EU GDP grew 2.1% qoq, 4.1% yoy. GDP volumes remained -0.1% below pre-pandemic level in Q4 2019. Austria (+3.8%) recorded the highest increase of GDP compared to the previous quarter, followed by France (+3.0) and Portugal (+2.9%). Lowest growth rates were observed in Romania and Slovakia (+0.4%), while GDP remained stable in Lithuania (0.0%).

RBA keeps cash rate at 0.1%, asset purchase as 4B a week

RBA left monetary policy unchanged as widely expected. The cash rate target is held at 0.10%. It reiterated that “the Board will not increase the cash rate until actual inflation is sustainably within the 2 to 3 per cent target range.”

Asset purchases will continue at AUD 4B a week until at least mid-February 2022. The decision on the program in February will be guided by the same three considerations used from the outset: “the actions of other central banks; how the Australian bond market is functioning; and, most importantly, the actual and expected progress towards the goals of full employment and inflation consistent with the target.”

More on RBA: RBA Stayed Put, Cautiously Optimistic Over Domestic Economy

Australia AiG services rose to 49.6, underachieving relative to expectations

Australia AiG Performance of Services rose 2.0 pts to 49.6 in November. Sales dropped -1.6 to 53.6. Employment dropped -0.6 to 56.2. New orders rose 8.6 to 47.4. Supplier deliveries rose 0.9 to 40.4. Input prices dropped -8.3 to 65.3. Selling prices dropped -3.5 to 58.2.

Ai Group Chief Executive, Innes Willox, said: “The Australian services sector was broadly stable in November, underachieving relative to expectations of a more convincing recovery after the COVID-19 downturn in recent months.”

Also released, house price index rose 5.0% qoq in Q3, slightly below expectation of 5.1% qoq.

RBNZ Hawkesby: A higher currency helps us achieve objectives more quickly

RBNZ Assistant Governor Christian Hawkesby said today that the central bank would take “considered steps” in raising interest rate. He added, “we have more confidence around the fact that the labour market is tight and that’s going to build inflation pressures.”

Regarding the government’s plan to reopen borders from January, Hawkesby said “One risk we are conscious of in the very short term is that even when the borders reopen, that actually becomes easier for more Kiwis to leave the country than it does for foreigners to come in… So there is a potential that the labour market gets tighter before it gets looser”.

Also, “at the moment a higher currency in the short term will actually help us achieve our objectives more quickly because a strong currency will feed through a lower tradeables inflation and feed through to lower inflation, and we are managing inflation from the top side.”

Separately, outgoing Deputy Governor Geoff Bascand said inflation is “definitely got some persistence to it for the next 12 months”. He added, we’ll see the CPI moving along at 4 percent over the next year, but we think it will moderate over time, some of those things that have driven it up won’t last forever.”

Bascand also said, “we will keep reducing stimulus and do our part to stop inflation from getting momentum into it.”

China exports rose 22% yoy in Nov, imports rose 31.7% yoy

In November in USD term, China exports rose 22.0% yoy, above expectation of 17.2% yoy. Imports rose 31.7% yoy, versus expectation of 19.5% yoy. Trade surplus narrowed to USD 71.7B, down from USD 84.5B, below expectation of USD 82.2B.

In CNY term, exports rose 16.6% yoy, below expectation of 17.2% yoy. Imports rose 26.0% yoy, above expectation of 9.4% yoy. Trade surplus narrowed to CNY 461B, down from CNY 546B, below expectation of CNY 575B.

From Japan, labor cash earnings rose 0.2% yoy in October, below expectation of 0.4% yoy. Household spending dropped -0.6% yoy, matched expectations.

AUD/USD Mid-Day Report

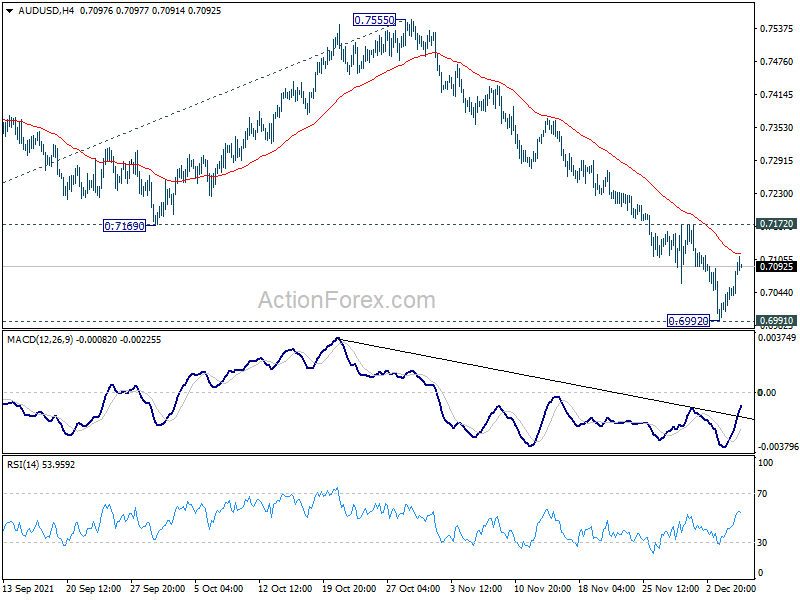

Daily Pivots: (S1) 0.6962; (P) 0.7031; (R1) 0.7068; More…

AUD/USD’s rebound from 0.6992 extends higher today but stays below 0.7172 resistance. Intraday bias is turned neutral first. On the upside, firm break of 0.7172 will indicate short term bottoming. Intraday bias will be turned back to the upside for 55 day EMA (now at 0.7281). On the downside, firm break of 0.6991 key structural support will carry larger bearish implication. Next target is 100% projection of 0.7890 to 0.7105 from 0.7555 at 0.6770.

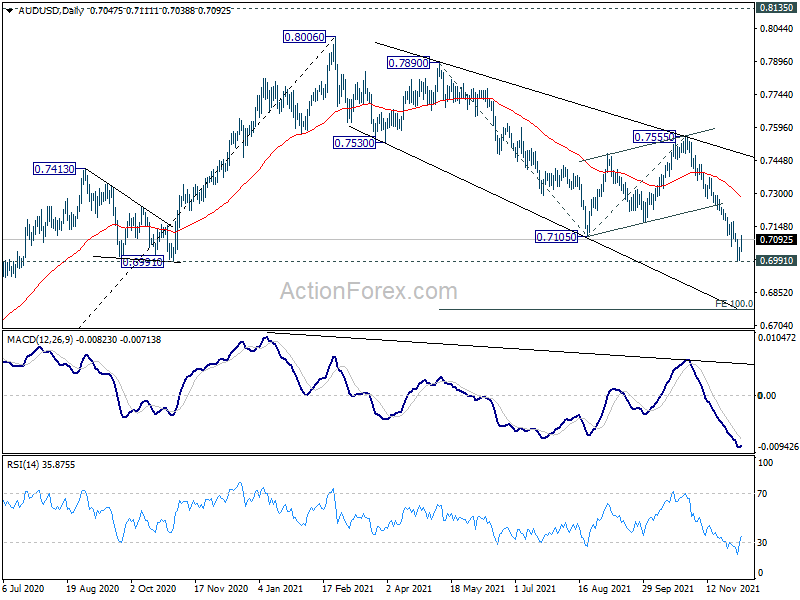

In the bigger picture, sustained break of 0.6991 cluster support will argue that the who up trend from 0.5506 might be finished at 0.8006, after rejection by 0.8135 long term resistance. Deeper decline would then be seen back to 61.8% retracement of 0.5506 to 0.8006 at 0.6461). For now, medium term outlook will stay bearish as long as 0.7555 resistance holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Services Index Nov | 49.6 | 47.6 | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Oct | 0.20% | 0.40% | 0.20% | |

| 23:30 | JPY | Household Spending Y/Y Oct | -0.60% | -0.60% | -1.90% | |

| 00:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Nov | 1.80% | 0.30% | -0.20% | |

| 00:30 | AUD | House Price Index Q/Q Q3 | 5.00% | 5.10% | 6.70% | |

| 02:00 | CNY | Trade Balance (USD) Nov | 71.7B | 82.2B | 84.5B | |

| 02:00 | CNY | Exports Y/Y Nov | 22.00% | 17.20% | 27.10% | |

| 02:00 | CNY | Imports Y/Y Nov | 31.70% | 19.50% | 20.60% | |

| 02:00 | CNY | Trade Balance (CNY) Nov | 461B | 575B | 546B | |

| 02:00 | CNY | Exports (CNY) Y/Y Nov | 16.60% | 17.20% | 20.30% | |

| 02:00 | CNY | Imports (CNY) Y/Y Nov | 26.00% | 9.40% | 14.50% | |

| 03:30 | AUD | RBA Interest Rate Decision | 0.10% | 0.10% | 0.10% | |

| 05:00 | JPY | Leading Economic Index Oct P | 102.1 | 100.2 | 100.9 | |

| 06:45 | CHF | Unemployment Rate Nov | 2.50% | 2.60% | 2.70% | |

| 07:00 | EUR | Germany Industrial Production M/M Oct | 2.80% | 0.80% | -1.10% | |

| 07:45 | EUR | France Trade Balance (EUR) Oct | -7.5B | -6.2B | -6.8B | -6.9B |

| 08:00 | CHF | Foreign Currency Reserves (CHF) Nov | 1006B | 923B | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 | 2.20% | 2.20% | 2.20% | |

| 10:00 | EUR | Eurozone Employment Change Q/Q Q3 F | 0.90% | 0.90% | 0.90% | |

| 10:00 | EUR | Germany ZEW Economic Sentiment Dec | 29.9 | 25.3 | 31.7 | |

| 10:00 | EUR | Germany ZEW Current Situation Dec | -7.4 | 5 | 12.5 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Dec | 26.8 | 23.5 | 25.9 | |

| 13:30 | USD | Trade Balance (USD) Oct | -67.1B | -66.9B | -80.9B | -81.4B |

| 13:30 | USD | Nonfarm Productivity Q3 | -5.20% | -4.90% | -5.00% | |

| 13:30 | USD | Unit Labor Costs Q3 | 9.60% | 8.40% | 8.30% | |

| 13:30 | CAD | Trade Balance (CAD) Oct | 2.1B | 1.6B | 1.9B | 1.4B |

| 15:00 | CAD | Ivey PMI Nov | 60.2 | 59.3 |