Dollar attempted for a rally overnight after hawkish comments from Fed Chair Jerome Powell, but momentum quickly faded. Instead, the greenback was dragged down by extended weakness in benchmark treasury yields. Overall market sentiment is stable in Asian session, helping commodity currencies rebound. Aussie is additionally lifted by better than expected GDP data. But then, any news regarding Omicron could trigger volatility again.

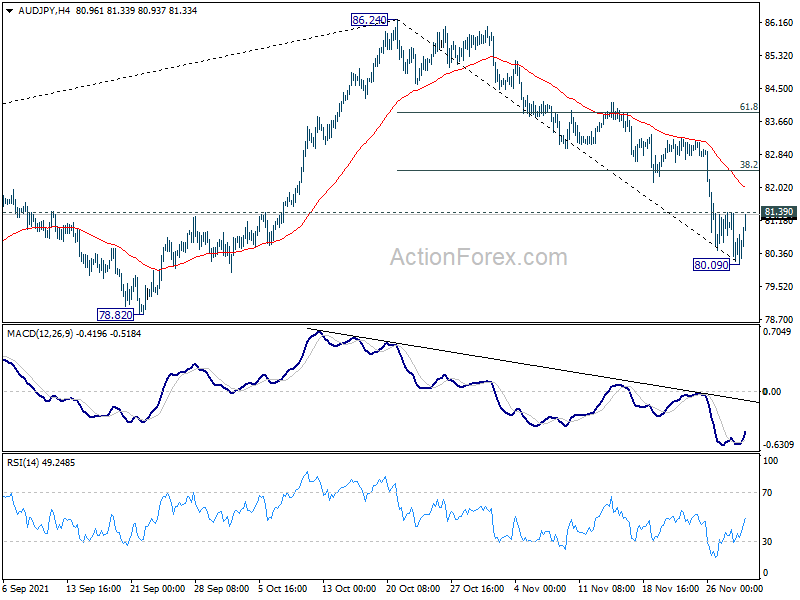

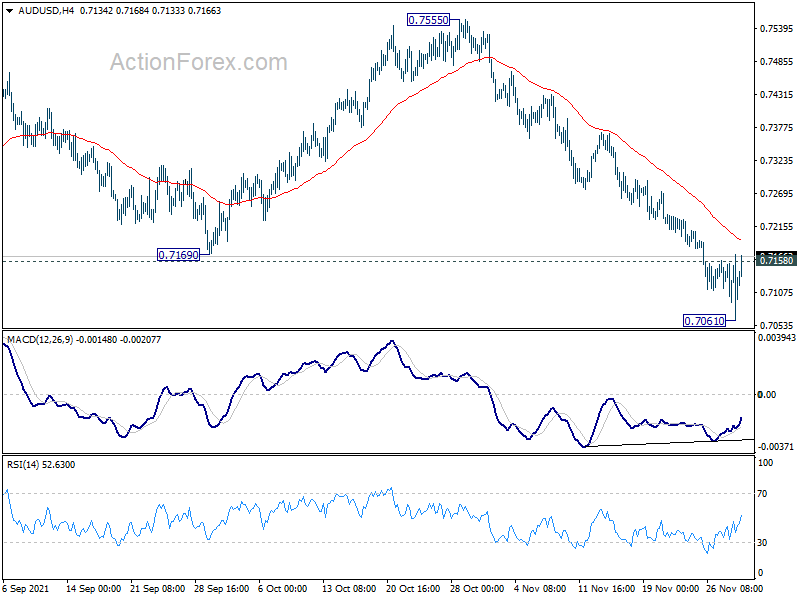

Technically, it looks like Aussie has at least found a temporary bottom, with AUD/USD’s break of 0.7158 minor resistance. we’d keep an eye on AUD/JPY today. Break of 81.39 will bring bring stronger recovery back to 4 hour 55 EMA (now at 82.02), and possibly further to 38.2% retracement of 86.24 to 80.09 at 82.43. We’ll see if overall risk sentiment could give Aussie a hand.

In Asia, at the time of writing, Nikkei is up 0.84%. Hong Kong HSI is up 1.40%. China Shanghai SSE is up 0.11%. Singapore Strait Times is up 1.29%. Japan 10-year JGB yield is up 0.0087 at 0.067. Overnight, DOW dropped -1.86%. S&P 500 dropped -1.90%. NASDAQ dropped -1.55%. 10-year yield dropped -0.087 to 1.443.

S&P 500 tumbled on hawkish Powell, pressing 55 D EMA

US stocks dropped sharply overnight following surprisingly hawkish comments from Fed Chair Jerome Powell. In short, he said that “the threat of persistently higher inflation has grown”. More importantly, Fed is “going to have a conversation at our next meeting about accelerating the taper and ending our asset purchases a few months early”.

More on Fed: Hawkish Powell Expects Fed to End QE Tapering a Few Months Earlier than Previously Anticipated

S&P 500 dropped -1.90% to close at 4567.0 and it’s now pressing 55 day EMA (now at 4564.0). Sustained break there will align the outlook with DOW, and indicates that 4743.83 is a medium term top.

In this case, SPX could have already started a correction to whole up trend from 3233.94. Deeper decline could then be seen back to 38.2% retracement of 3233.94 to 4743.83 at 4167.05. For now, risk will stay on the downside as long as 4743.83 resistance holds, in case of recovery.

Australia GDP contracted -1.9% qoq in Q3, back below pre-pandemic level

Australia GDP contracted -1.9% qoq in Q3, better than expectation of -2.7% qoq. Through the year, GDP was up 3.9%.

Acting Head of National Accounts at the ABS, Sean Crick said: “Domestic demand drove the fall, with prolonged lockdowns across NSW, Victoria and the ACT resulting in a substantial decline in household spending.

“The fall in domestic demand was only partly offset by growth in net trade and public sector expenditure. GDP in the September quarter 2021 was 0.2 per cent below the December quarter 2019 pre-pandemic level.”

Australia AiG manufacturing rose to 54.8, grew more decisively

Australia AiG Performance of Manufacturing Index rose 4.4 pts to 54.8 in November. Looking at some details, production rose 4.7 to 52.5. Employment rose 2.0 to 50.0. New orders rose 1.0 to 59.3. Supplier deliveries rose 12.2 to 53.4. Input prices dropped -3.5 to 78.3. Selling prices rose 4.2 to 68.1. Average wages dropped -1.3 to 62.4.

Ai Group Chief Executive Innes Willox said: “The Australian manufacturing industry grew more decisively in November after a few flat months during which the south-east corner of the country was held back by the delta outbreaks and associated activity restrictions and while the states and territories tightened barriers to the movement of people.”

China Caixin PMI manufacturing dropped to 49.9, recovery not solid

China Caixin PMI Manufacturing dropped from 50.6 to 49.9 in November, below expectation of 50.5. Caixin added that output rose for the first time in four months as power supply issues unwound. But total new orders fell slightly. Inflationary pressures eased markedly.

Wang Zhe, Senior Economist at Caixin Insight Group said: “To sum up, the manufacturing sector remained stable overall in November. Increased downward pressure and easing inflationary pressure were prominent features of the economic situation…. After the shortage of power was alleviated, the supply side began to recover. But due to weak demand, the supply recovery was limited, and the foundation of the recovery was not solid.”

Japan PMI manufacturing finalized at 54.5 in Nov

Japan PMI Manufacturing was finalized at 54.5 in November, up from October’s 53.2. That’s the best reading since January 2018, and the 10th consecutive month of overall growth. Markit noted that output and new orders rose at faster rates. There was sharp rise in cost burdens amid sustained supply chain disruption. Businesses reported strong optimism regarding future output.

Also released, capital spending rose 1.2% in Q3 versus expectation of 2.7%.

Looking ahead

Swiss CPI and SVME PMI will be released in European session. Germany will release retail sales. Eurozone and UK will release PMI manufacturing.

Later in the day, Canada will release building permits and PMI manufacturing. US will release ISM manufacturing and construction spending. Fed will also publish Beige Book economic report.

AUD/USD Daily Report

Daily Pivots: (S1) 0.7071; (P) 0.7121; (R1) 0.7179; More…

AUD/USD’s break of 0.7158 minor resistance argues that a short term bottom might be formed at 0.7061, on bullish convergence condition in 4 hour MACD. Intraday bias is back on the upside for stronger rebound, possibly towards 55 day EMA (now at 0.7318). In case of another fall, we’d look for support from 0.6991/7051 key support zone to bring rebound. But sustained break there will carry larger bearish implications.

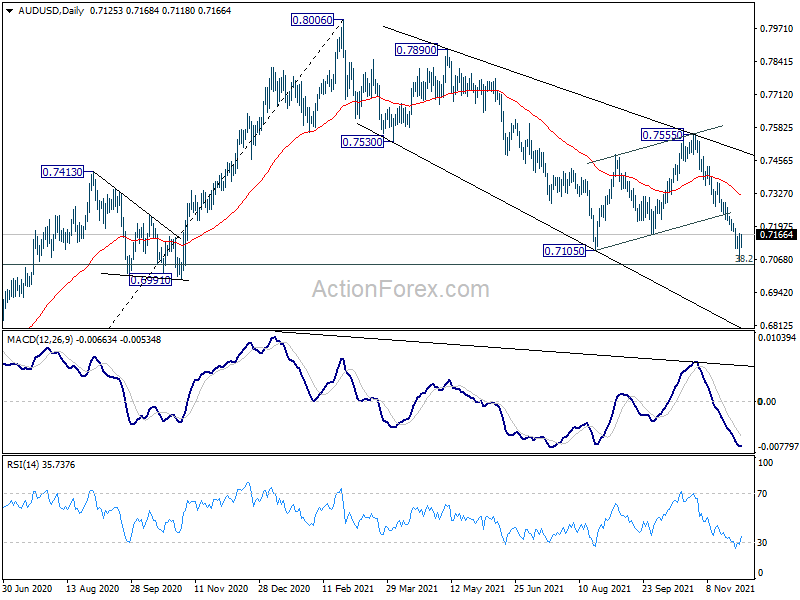

In the bigger picture, with 0.6991 cluster support (38.2% retracement of 0.5506 to 0.8006 at 0.7051) intact, we’re seeing price action from 0.8006 as a correction only. That is, up trend from 0.5506 low would resume after the correction completes. However, sustained break of 0.6991 will argue that the whole medium term trend has probably reversed. Deeper fall would be seen to 61.8% retracement at 0.6461.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Manufacturing Index Nov | 54.8 | 50.4 | ||

| 21:45 | NZD | Building Permits M/M Oct | -2.00% | -1.90% | -2.00% | |

| 23:50 | JPY | Capital Spending Q3 | 1.20% | 2.70% | 5.30% | |

| 00:01 | GBP | BRC Shop Price Index Y/Y Oct | 0.30% | -0.40% | ||

| 00:30 | AUD | GDP Q/Q Q3 | -1.90% | -2.70% | 0.70% | |

| 00:30 | JPY | Manufacturing PMI Nov F | 54.5 | 54.2 | 54.2 | |

| 01:45 | CNY | Caixin Manufacturing PMI Nov | 49.9 | 50.5 | 50.6 | |

| 07:00 | EUR | Germany Retail Sales M/M Oct | 1.00% | -2.50% | ||

| 07:30 | CHF | CPI M/M Nov | -0.10% | 0.30% | ||

| 07:30 | CHF | CPI Y/Y Nov | 1.40% | 1.20% | ||

| 08:30 | CHF | SVME PMI Nov | 64.5 | 65.4 | ||

| 08:45 | EUR | Italy Manufacturing PMI Nov | 61 | 61.1 | ||

| 08:50 | EUR | France Manufacturing PMI Nov F | 54.6 | 54.6 | ||

| 08:55 | EUR | Germany Manufacturing PMI Nov F | 57.6 | 57.6 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Nov F | 58.6 | 58.6 | ||

| 09:30 | GBP | Manufacturing PMI Nov F | 58.2 | 58.2 | ||

| 13:15 | USD | ADP Employment Change Nov | 525K | 571K | ||

| 13:30 | CAD | Building Permits M/M Oct | 0.10% | 4.30% | ||

| 14:30 | CAD | Manufacturing PMI Nov | 57.7 | |||

| 14:45 | USD | Manufacturing PMI Nov F | 59.1 | 59.1 | ||

| 15:00 | USD | ISM Manufacturing PMI Nov | 61 | 60.8 | ||

| 15:00 | USD | ISM Manufacturing Prices Paid Nov | 86 | 85.7 | ||

| 15:00 | USD | ISM Manufacturing Employment Index Nov | 52 | |||

| 15:00 | USD | Construction Spending M/M Oct | 0.40% | -0.50% | ||

| 15:30 | USD | Crude Oil Inventories | -1.5M | 1.0M | ||

| 19:00 | USD | Fed’s Beige Book |