While US stocks staged a strong rebound overnight, the moves didn’t follow through in mixed Asia. There is also little reaction in the currency markets. Yen and Dollar remain the strongest ones for the week, despite retreating mildly. New Zealand Dollar is the worst performer, followed by Aussie and then Sterling. Euro is not performing too badly, given some support in crosses. With a light economic calendar today, focuses will stay on developments in the risk markets, and then turn to ECB’s new forward guidance tomorrow.

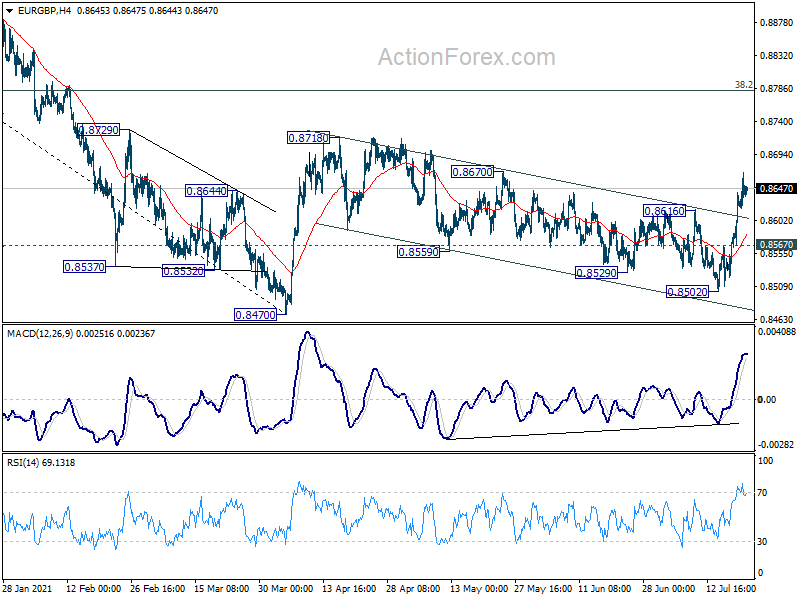

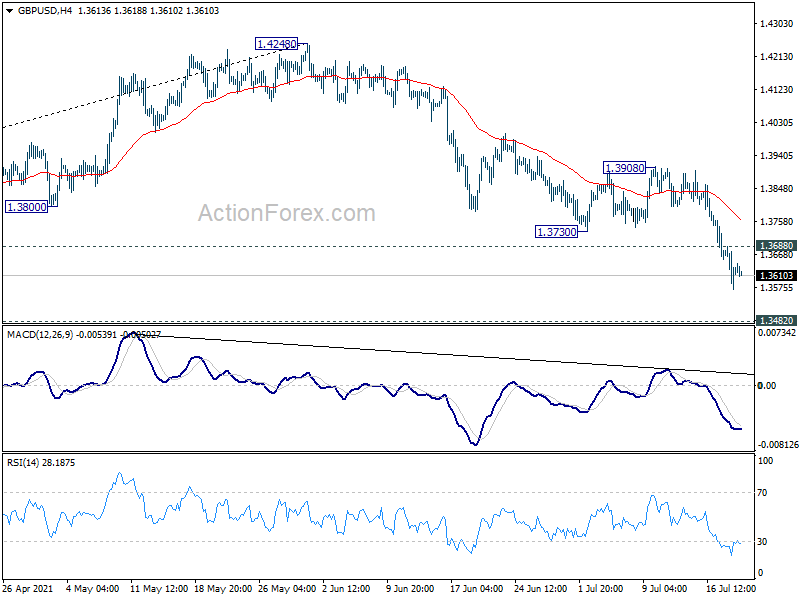

Technically, we’d continue to pay attention to some Sterling pairs. As noted before, firm break of 0.8670 resistance in EUR/GBP could argues that whole rebound from 0.8470 is ready to resume through 0.8718 resistance. Sustained break of 149.03 support in GBP/JPY could open up the bearish case for deeper decline to 142.71 resistance turned support. GBP/USD could also test 1.3482 resistance turned support and firm break there would confirm correction to whole rise from 1.1409.

In Asia, at the time of writing, Nikkei is up 0.44%. Hong Kong HSI is down -0.56%. China Shanghai SSE is up 0.65%. Singapore Strait Times is down -0.07%. Japan 10-year JGB yield is down -0.0037 at 0.011. Overnight, DOW rose 1.62%. S&P 500 rose 1.52%. NASDAQ rose 1.57%. 10-year rose 0.028 to 1.209.

BoJ Masayoshi: Inflation sluggish and powerful easing necessary

BoJ Deputy Governor Amamiya Masayoshi said speech, an uptrend in private consumption is expected to “become evident” as the impact of COVID-19 wanes gradually and employee income increases”. The “virtuous cycle” in the “corporate sector” will spread to the “household sector”, and “intensifying the cycle in the overall economy.” Nevertheless, the baseline scenario entails “high uncertainties” with risks “skewed to the downside” on the spread of variants. But activity could improve more than expected as vaccine rollout accelerates.

Masayoshi also said that it will “take time” to achieve price stability target of 2% inflation. He added, “while the inflation rate has risen clearly of late in the United States and other countries, it has been sluggish in Japan.” Giver this, “it is necessary for the Bank to persistently continue to conduct powerful monetary easing with a view to achieving the price stability target.”

Japan exports rose 48.6% yoy in Jun, 4th month of double-digit growth

Japan’s exports rose 48.6% yoy to JPY 7220B in June. That;s the fourth straight month of double-digit growth, even though it’s largely exaggerated by the pandemic plunge last year. By destination, exports to China jumped 27.7% yoy, led by demand for chip-making equipment, raw materials and plastic. Exports to US also rose 85.5% yoy, driven by cars, auto parts and motors. Imports rose 32.7% yoy to JPY 6837B. Trade surplus came in at JPY 383B.

In seasonally adjusted terms, exports rose 2.4% mom to JPY 7040B. Imports rose 4.0% mom to JPY 7130B. Trade balance turned into deficit of JPY 0.09T, versus expectation of JPY 0.02T surplus.

Australia retail sales dropped -1.8% mom in Jun on return to restrictions

According to preliminary estimate, Australia retail sales dropped -1.8% or AUD -515.1m in June 2021. Comparing to June 2020, sales rose 2.9% yoy. Victoria (-3.5 per cent) led the state falls in June, with the impact of the state’s fourth lockdown more pronounced in June than May (-0.9 per cent). New South Wales (-2.0 per cent) and Queensland (-1.5 per cent) also fell due to stay-at-home restrictions and reduced interstate mobility.

Ben James, Director of Quarterly Economy Wide Surveys, said: “June’s fall in turnover was due to the impact of coronavirus restrictions across multiple states. Victoria saw restrictions from the start of the month, which were gradually eased from the 11th of June. New South Wales, in particular Greater Sydney, saw stay-at-home orders issued towards the end of the month. Other states and territories saw interrupted trade due to mini-lockdowns, as well as reduced mobility between states with the tightening of border restrictions.”

Australia Westpac leading index dropped to 1.34, RBA to use flexibility in asset purchases

Australia Westpac leading index slowed from 1.68% to 1.34% in June. The index peaked at 5% back in November last year and then gradually fallen back. It’s still comfortably above zero and signals outlook for above trend growth. Still, Westpac expected -3.1% contraction in GDP in Q3 in New South Wales and -0.1% in Victoria due to renewed lockdowns.

Westpac added that RBA would be advised of significant downward revisions for Q3 growth at the meeting on August 3. It said it’s an “appropriate time” for RBA to use the “flexibility” on asset purchases. At the least it could announce to defer the tapering from AUD 5B to AUD 4B a week, which is scheduled to start in September. Further, “a decision to immediately lift purchases to $6 billion per week would certainly send the right signal that the Bank is responsive to economic developments and is prepared to use its new flexible policy tool accordingly.”

Looking ahead

Economic calendar continues to be light today, with UK public sector net borrowing and Canada new housing price index featured.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3570; (P) 1.3630; (R1) 1.3687; More….

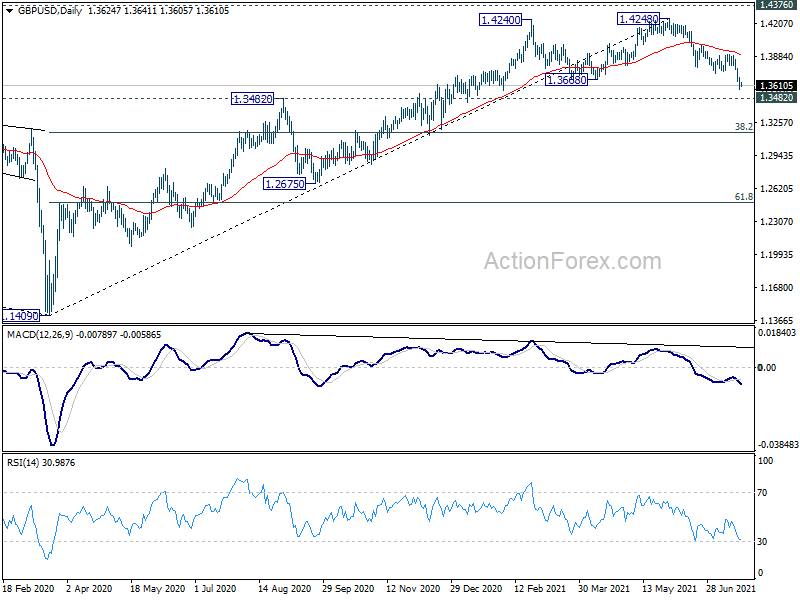

Intraday bias in GBP/USD remains on the downside at this point. Current fall from 1.4248 is in progress for 1.3482 resistance turned support next. Decisive break there will indicate that it’s already correcting whole up trend from 1.1409. Next target will then be 38.2% retracement of 1.1409 to 1.4248 at 1.3164. On the upside, above 1.3688 minor resistance will turn intraday bias neutral first. But further fall will remain in favor as long as 1.3908 resistance holds.

In the bigger picture, as long as 1.3482 resistance turned support holds, up trend from 1.1409 should still continue. Decisive break of 1.4376 resistance will carry larger bullish implications. However, firm break of 1.3482 support will argue that the rise from 1.1409 has completed. GBP/USD would then be seen in another leg of long term range pattern between 1.1409 and 1.4376. Deeper fall could then be seen to 61.8% retracement of 1.1409 to 1.4248 at 1.2493, and even below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Jun | -0.09T | 0.02T | 0.04T | 0.02T |

| 23:50 | JPY | BoJ Minutes | ||||

| 0:30 | AUD | Westpac Leading Index M/M Jun | -0.10% | -0.10% | 0.10% | |

| 1:30 | AUD | Retail Sales M/M Jun P | -1.80% | -0.50% | 0.40% | |

| 6:00 | GBP | Public Sector Net Borrowing (GBP) Jun | 21.5B | 23.6B | ||

| 12:30 | CAD | New Housing Price Index M/M Jun | 1.10% | 1.40% | ||

| 14:30 | USD | Crude Oil Inventories | -7.9M |

#optionbuying #optionstrading#trading#nifty #scalping #sharemarket #shorts #ytshorts

#optionbuying #optionstrading#trading#nifty #scalping #sharemarket #shorts #ytshorts