The BOE would maintain an upbeat tone at this week’s meeting. However, the uncertainty, in particular a third wave of the pandemic which has caused a delay in restriction easing, suggests that it would be too early to hint about tapering of monetary policy or pushing forward the first rate hike.

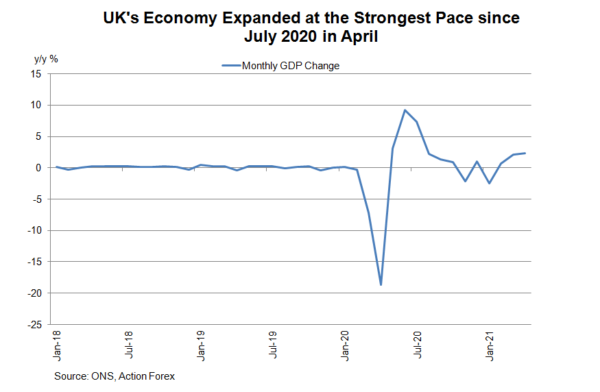

Economic data released since the last meeting have been strong. GDP growth accelerated to +2.3% y/y in April, strongest since July 2020, as pandemic-related restrictions loosened. Service activities expanded +3.4%, while production and construction activities dropped -1.3% and -2% respectively. April’s GDP remains 3.7% below the pre-pandemic levels seen in February 2020. Yet, it’s 1.2 ppt above its initial recovery peak in October 2020. The strong April data points to upside risks to BOE’s forecast of +4.3% q/q in 2Q21. Confederation of British Industry (CBI) now projects that GDP would expand by +8.2% this year and by +6.1% next year.

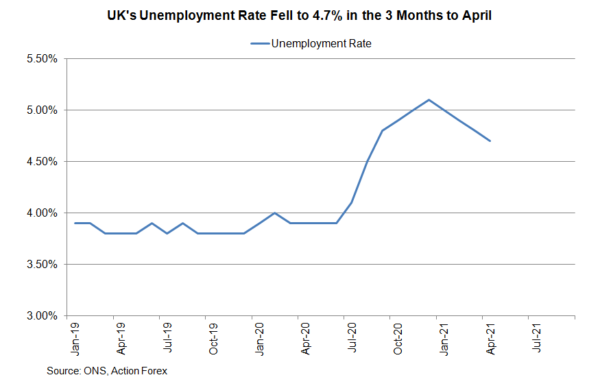

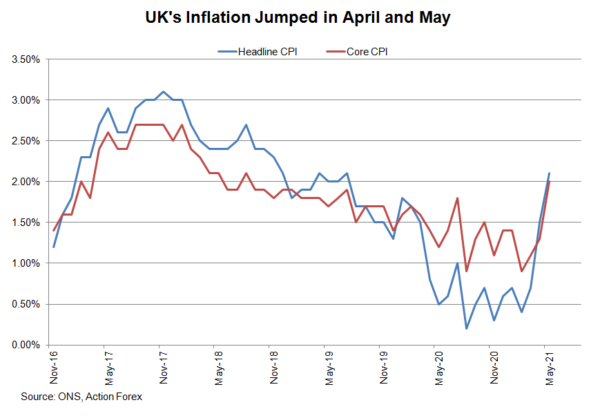

The unemployment rate fell to 4.7% in the 3 months through April. While this is the fourth consecutive monthly decline, the BOE would refrain from being too optimistic about the job market situation. It is likely the unemployment rate would rise later this year after end of the job support scheme. In May, the BOE projected that the unemployment rate will increase to 5.2% in 2Q21. On inflation, headline CPI accelerated to +2.1% y/y, highest since July 2019, in May. Core CPI also jumped to +2%, from April’s +1.3%. However, policymakers should continue to attribute the strong price level to temporary factors. Rising inflation in May is unlikely a trigger to reduce stimulus, in particular when inflation expectations have eased quite significantly over the past 2 weeks.

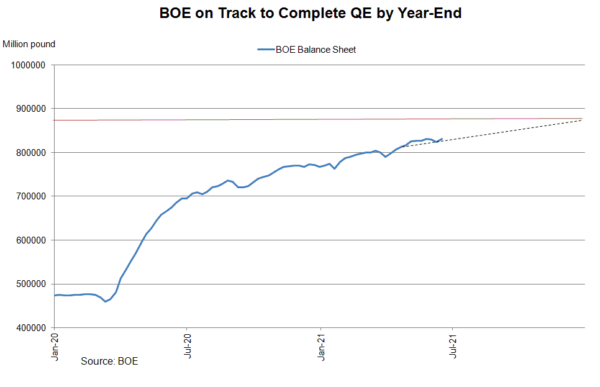

Despite the high vaccination rate, the country is in the midst of a third wave of the coronavirus pandemic. The government have delayed for a month the last phase of lifting of lockdown measures. The risk to the recovery outlook is to the downside. It would be prudent for policymakers to leave all monetary policy tools unchanged this month. We expect the members to vote unanimously to keep the Bank rate at 0.1% and 8-1 to keep QE purchases at 875B pound of gilts.

Despite the high vaccination rate, the country is in the midst of a third wave of the coronavirus pandemic. The government have delayed for a month the last phase of lifting of lockdown measures. The risk to the recovery outlook is to the downside. It would be prudent for policymakers to leave all monetary policy tools unchanged this month. We expect the members to vote unanimously to keep the Bank rate at 0.1% and 8-1 to keep QE purchases at 875B pound of gilts.