Dollar weakens broadly in relatively quiet Asian session today, while Australian Dollar is strengthening. Asia markets are trading mildly lower, but losses are limited. Month-end flow, plus holiday in the UK and the US, could keep activity subdued today. But the week ahead is extremely busy, with lots of first-tier economic data featured.

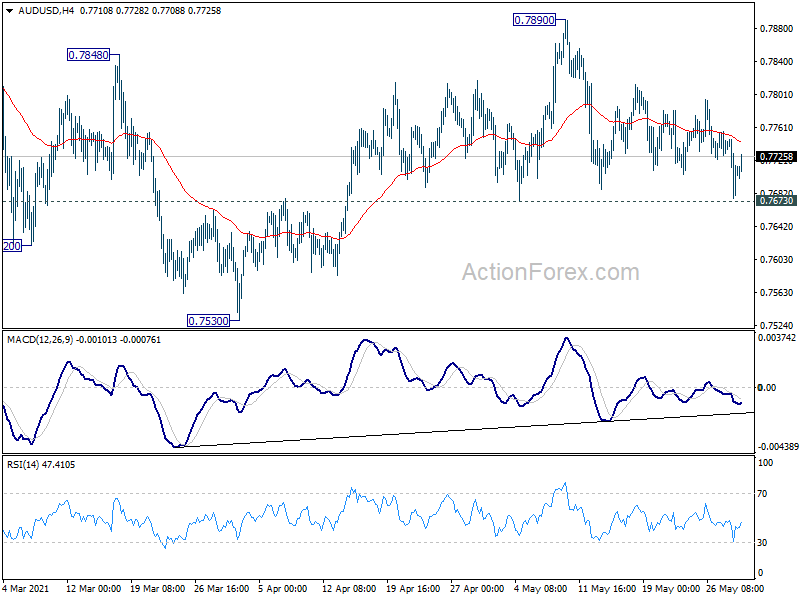

Technically, Dollar’s rebound attempt faltered quickly last Friday. Some near term resistance levels are still intact, keeping the greenback mildly bearish in general. The levels include 1.4090 support in GBP/USD, 0.7673 support in AUD/USD, 0.9046 resistance in USD/CHF and 1.2201 resistance in USD/CAD. We’d pay attention to whether selling in Dollar would come back soon.

In Asia, at the time of writing, Nikkei is down -1.07%. Hong Kong HSI is down -0.5%. China Shanghai SSE is down -0.20%. Singapore Straits Times is down -0.53%. Japan 10-year JGB yield is down -0.0014 at 0.084.

Japan industrial production rose 2.5% mom, retail sales rose 12% yoy

Japan industrial production grew 2.5% mom in April, below expectation of 4.1% mom. Manufacturers surveyed by the Ministry of Economy, Trade and Industry (METI) expected output to contract -1.7% in May, followed by a 5.0% rebound in June.

Retail sales rose 12.0% yoy, below expectation of 15.4% yoy. Over the month, sales dropped -4.5% mom on a seasonally adjusted basis.

China PMI manufacturing edged lower to 51.0, PMI non-manufacturing rose to 55.2

China official PMI manufacturing dropped slightly to 51.0 in May, down from 51.1, below expectation of 51.1. Looking at some details, production rose 0.5 to 52.7. New orders dropped to 51.3, while raw material inventory dropped to 47.7. New export orders also dropped to 48.2.

PMI non-manufacturing rose to 55.2, up from 54.9, above expectation of 52.7.

New Zealand ANZ business confidence rose to 1.8, economy struggling to keep up with demand

New Zealand ANZ business confidence rose to 1.8 in May, up from April’s -2.0, but well below preliminary reading of 7.0. Own activity outlook rose to 27.1, up from April’s 22.2, but below preliminary reading of 32.3.

Looking at some more details, export intentions rose from 9.1 to 12.2. Investment intentions rose from 17.1 to 18.9. Cost expectations rose from 76.1 to 81.3. Employment intentions rose from 16.4 to 20.5. Pricing intentions rose from 55.8 to 57.4.

ANZ said: “The New Zealand economy is struggling to keep up with demand, and cost and inflation pressures continue to build. Firms are having trouble sourcing inputs to production. We wouldn’t read too much into the drop in activity indicators in the second half of the month just yet, as it may have been influenced by Budget uncertainty. We won’t have to wait long to get a fresh read, with the preliminary June data due to be released on 9 June.”

An extremely busy week ahead

It’s an extremely busy, and potentially very volatile week ahead. In particular, US ISMs and NSP will be watched close to gauge how strong the rebound in US economy would be . Eurozone inflation data, Swiss GDP, Canada GDP, China, CPIs are also important. As for Australian Dollar, RBA rate decision is a focus, but it’s unlikely to follow RBNZ to turn hawkish. Instead, GDP and retail sales could be more market moving.

Here are some highlights for the week:

- Monday: Japan industrial production, retail sales, consumer confidence, housing starts; Australia MI inflation gauge, private sector credit; China PMIs; Germany CPI flash; Eurozone M3 money supply; Canada current account, IPPI and RMPI.

- Tuesday: RBA rate decision, Australia AiG manufacturing, building approvals, current account; Japan capital spending, PMI manufacturing final. China Caixin PMI manufacturing; Swiss GDP, retail sales, PMI manufacturing; Eurozone PMI manufacturing final, CPI flash, unemployment rate; Germany unemployment; UK PMI manufacturing final; Canada GDP, PMI manufacturing; US ISM manufacturing, construction spending.

- Wednesday: Japan monetary base, New Zealand terms of trade; Australia GDP; Germany retail sales; UK M4 money supply, mortgage approvals; Eurozone PPI; Canada building permits; Fed Beige Book report.

- Thursday: Australia retail sales, trade balance; China Caixin PMI services; Eurozone PMI services final; UK PMI services final; US ADP employment, jobless claims, nonfarm productivity, ISM services.

- Friday: Japan household spending; UK PMI construction; Eurozone retail sales; Canada employment, labor productivity, Ivey PMI; US non-farm payrolls, factory orders.

AUD/USD Daily Report

Daily Pivots: (S1) 0.7674; (P) 0.7711; (R1) 0.7744; More…

Intraday bias in AUD/USD remains neutral for the moment, and further rise is in favor with 0.7673 support intact. On the upside, break of 0.7890 will resume the rise from 0.7530 to retest 0.8006 high. However, on the downside, firm break of 0.7673 will suggest that correction from 0.8006 is extending with another falling leg. Intraday bias will be turned back to the downside for 0.7530 support and possibly below.

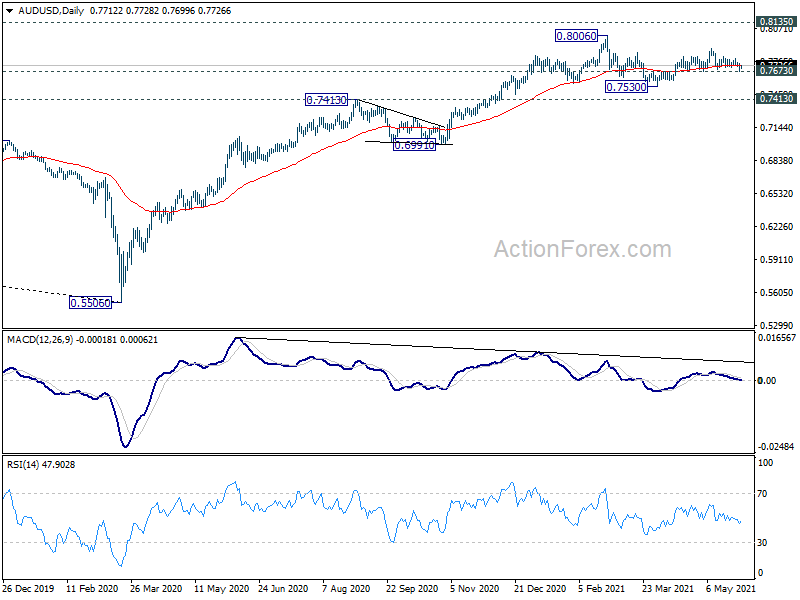

In the bigger picture, whole down trend from 1.1079 (2001 high) should have completed at 0.5506 (2020 low) already. Rise from 0.5506 could either be the start of a long term up trend, or a corrective rise. Reactions to 0.8135 key resistance will reveal which case it is. But in any case, medium term rally is expected to continue as long as 0.7413 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Apr P | 2.50% | 4.10% | 1.70% | |

| 23:50 | JPY | Retail Trade Y/Y Mar | 12.00% | 15.40% | 5.20% | |

| 1:00 | CNY | Manufacturing PMI May | 51 | 51.1 | 51.1 | |

| 1:00 | CNY | Non-Manufacturing PMI May | 55.2 | 52.7 | 54.9 | |

| 1:00 | NZD | ANZ Business Confidence May | 1.8 | 7 | ||

| 1:30 | AUD | Private Sector Credit M/M Apr | 0.20% | 0.40% | 0.40% | |

| 5:00 | JPY | Housing Starts Y/Y Apr | 5.20% | 1.50% | ||

| 5:00 | JPY | Consumer Confidence May | 35.3 | 34.7 | ||

| 8:00 | EUR | Eurozone M3 Money Supply Y/Y Apr | 9.50% | 10.10% | ||

| 12:00 | EUR | Germany CPI M/M May P | 0.30% | 0.70% | ||

| 12:00 | EUR | Germany CPI Y/Y May P | 2.40% | 2.00% | ||

| 12:30 | CAD | Industrial Product Price M/M Apr | 1.60% | |||

| 12:30 | CAD | Raw Material Price Index Apr | 2.30% | |||

| 12:30 | CAD | Current Account (CAD) Q1 | 2.4B | -7.3B |