Dollar and Yen rebound notably today as consolidative trading continues, with help from mixed sentiments. European indices are mixed while US futures point to lower open. Major global trading yields are trading lower, with US 10-year yield below 1.6 handle. New Zealand Dollar is leading Australian Dollar lower, followed by Sterling.

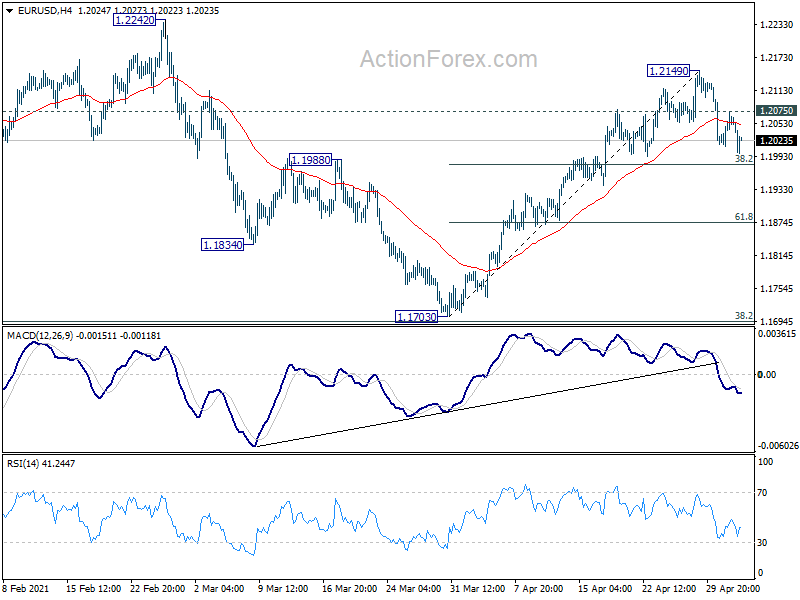

Technically, we’d maintain the current recoveries in Dollar and Yen are just part of consolidations, rather than reversal. Indeed, we’ll keep an eye on 1.2075 minor resistance in EUR/USD. Break will suggest that pull back in EUR/USD, and recovery in Dollar, has completed.

In Europe, at the time of writing, FTSE is up 0.06%. DAX is down -1.50%. CAC is down -0.46%. Germany 10-year yield is down -0.0297 at -0.230. Earlier in Asia, Hong Kong HSI rose 0.70%. Singapore Strait Times dropped -0.18%. Japan and China were on holiday.

US trade deficit widened to USD 74.4B in March

US exports in goods and services rose 6.6% mom to USD 200B in March. Imports rose 6.3% mom to USD 274.5B. Trade deficit widened to USD 74.4B, slightly above expectation of USD 73.4B.

Trade deficit with China increased USD 6.7B to USD 36.9B. Exports increased USD 0.9B to USD 11.3B and imports increased USD 7.6B to USD 48.2B.

Trade deficit with the European Union decreased USD 2.1B to USD 16.9 B in March. Exports decreased USD 0.5B to USD 20.1B and imports decreased USD 2.6B to USD 37.0B.

From Canada trade balance turned into CAD 1.1B deficit in March. Building permits rose 5.7% mom in March.

UK PMI manufacturing finalized at 60.9, marked growth spurt beset by supply chain issues

UK PMI Manufacturing was finalized t 60.9 in April, up from 58.9. That’s also the highest reading since July 1994’s record high at 61.0. Markit said production and new order growth strengthened. Output prices rose at record pace.

Rob Dobson, Director at IHS Markit, said: “Further loosening of COVID-19 restrictions at home and abroad led to another marked growth spurt at UK factories. The headline PMI rose to a near 27-year high, as output and new orders expanded at increased rates. The outlook for the sector is also increasingly positive, with two-thirds of manufacturers expecting output to be higher in one year’s time. Export growth remains relatively subdued, however, as small manufacturers struggle to export.

“The sector also remains beset by supply-chain issues and rising inflationary pressures. Disruption following Brexit and COVID-19, especially at ports, caused a further near-record lengthening of supplier delivery times. The resulting input shortages kept producer price inflation among the highest over the past four years. Manufacturers have generally passed on these costs to customers, as highlighted by a survey-record rise in selling prices, but it is hoped that this inflationary backdrop will subside once supply and demand come back into line as covid-related logistic delays ease.”

Swiss SECO consumer climate rose to -7.1, back at pre-crisis level

Swiss SECO consumer climate rose to -7.1 in Q2, up from -14.2. The reading was approximately back at pre-pandemic level, and closing in on its long-term average at -5. Looking at some details, expected economic development rose form -17.7 to 3.4, turned positive. Expected financial situation edged up from -7.2 to -6.4.

SECO said: “Sentiment amongst Swiss households is improving. The results of the April survey show that expectations regarding general economic development in particular are becoming more positive. The likelihood of households making major purchases has also risen.”

RBA stands pat, upgrades GDP forecasts further

RBA maintained monetary policy settings as widely expected. Cash rate and 3-year yield target are held at 0.10%. Parameters of the Term Funding Facility and bond purchases are held unchanged too. It also maintained that the condition for raising the cash rate is unlikely to be reached until 2024 at the earliest.

At its “July meeting”, RBA will consider whether to retail April 2024 bond as the 3-year yield target, or shift to next maturity, “at its July meeting”. But the board is “not considering a change to the target of 10 basis points”. At the meeting, RBA will also consider future bond purchases after current program completes in September.

Central scenario for GDP growth was “revised up further”. RBA now sees 4.75% GDP growth over 2021, 3.50% over 2022. Unemployment rate is projected to decline to around 5% at the end of this year and further to 4.5% at the end of 2022.

But CPI data “confirmed that inflation pressures remain subdued” in most parts of the economy. Underlying inflation is expected to be 1.5% in 2021 and 2% in mid-2023, even though CPI inflation might rise temporarily to above 3% in June quarter.

More on RBA:

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2025; (P) 1.2050; (R1) 1.2088; More….

EUR/USD is staying in consolidation below 1.2149 and intraday bias remains neutral. Downside should be contained by 38.2% retracement of 1.1703 to 1.2149 at 1.1979 to bring rebound. On the upside, above 1.2075 minor resistance will turn bias back to the upside for 1.2149 resistance. Break there will resume the rise from 1.1703 to 1.2242/2348 resistance zone. However, firm break of 1.1979 will bring deeper fall to 1.1873.

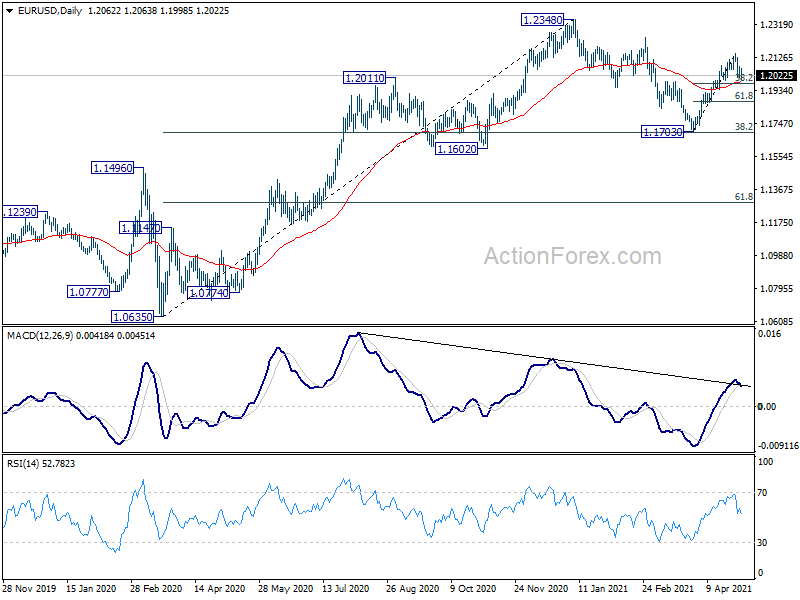

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. However, sustained break of 1.1602 will argue that whole rise from 1.10635 has completed. Deeper fall would be seen to 61.8% retracement of 1.0635 to 1.2348 at 1.1289.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Mar | 5.57B | 8.30B | 7.53B | 7.60B |

| 04:30 | AUD | RBA Rate Decision | 0.10% | 0.10% | 0.10% | |

| 07:00 | CHF | SECO Consumer Climate Q2 | -7 | -11 | -15 | |

| 08:30 | GBP | Mortgage Approvals Mar | 83KK | 85K | 88K | |

| 08:30 | GBP | Manufacturing PMI Apr F | 60.9 | 60.7 | 60.7 | |

| 08:30 | GBP | M4 Money Supply M/M Mar | 0.60% | 0.80% | 0.80% | |

| 12:30 | CAD | Building Permits M/M Mar | 5.70% | 1.60% | 2.10% | 3.10% |

| 12:30 | CAD | Trade Balance (CAD) Mar | -1.1B | 0.5B | 1.0B | 1.4B |

| 12:30 | USD | Trade Balance (USD) Mar | -74.4B | -73.4B | -71.1B | -70.5B |

| 14:00 | USD | Factory Orders M/M Mar | 1.10% | -0.80% |

#shorts #crypto #forex #trading #patterns

#shorts #crypto #forex #trading #patterns