Selloff in Yen and Swiss Franc remain a main theme in the markets in Asia today, while Euro is also weak. Dollar is staying firm but it’s struggling to extend gain against commodity currencies and Sterling for now. Indeed, Aussie and Loonie are now trying to reverse some of this week’s losses against the greenback. Rally in US treasury yields continues to be a main driving force overall, as supported by upbeat comments from Fed officials Focuses will turn to US ADP job report today, as prelude to Friday’s non-farm payrolls.

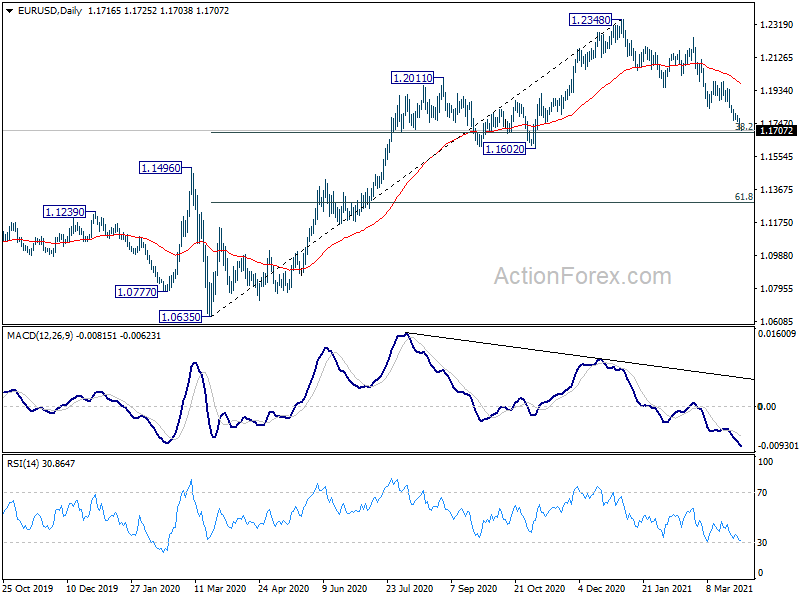

Technically, EUR/USD is going to enter into an important support zone between 1.1602 and 38.2% retracement of 1.0635 to 1.2348 at 1.1694. We’re expecting strong support from this zone to complete the correction from 1.2348. But firm break there will raise the odds of larger bearishness, that could shape the trend for Q2 at least.

In Asia, Nikkei is currently down -0.79%. Hong Kong HSI is down -0.17%. China Shanghai SSE is down -0.63%. Singapore Strait Times is down -0.06%. Japan 10-year JGB yield is down -0.0043 at 0.089. Overnight, DOW dropped -0.31%. S&P 500 dropped -0.32%. NASDAQ dropped -0.11%. 10-year yield rose 0.005 to 1.726, after hitting as high as 1.765.

Japan industrial production dropped -2.1% mom in Feb, more contraction expected in Mar

Japan industrial production dropped -2.1% mom in February, worse than expectation of -1.3% mom. In addition to pandemic restrictions, production was disrupted by the 7.3-earthquake off the coast of eastern Japan on February 13.

Manufacturers surveyed by the Ministry of Economy, Trade and Industry expected output to drop another -1.9% mom in March, followed by 9.3% mom rebound in April. But the actual figure could be worse as the impact of the March 19 fire at a Renesas Electronics chip-making plant was not reflected in the forecasts yet.

China PMI manufacturing rose to 51.9, PMI non-manufacturing rose to 56.3

China official PMI Manufacturing rose to 51.9 in March, up from 50.6, above expectation of 51.0. That’s also the highest level in 2021. 17 of the 21 industries saw expansion in the month. New order index rose 2.1 pts to 53.6. New export orders rose 2.4 pts to 51.1. PMI Non-Manufacturing jumped to 56.3, up from 51.4, above expectation of 52.6. PMI Composite rose to 55.3, up from 51.6.

“After the Lunar New Year, the recovery of production accelerated, and the manufacturing industry rebounded significantly in March,” said Zhao Qinghe, a senior statistician at the NBS. “As the results of pandemic controls being consolidated, consumer demand continues to be released, and the service industry accelerated its recovery.”

New Zealand ANZ business confidence dropped to -4.1, demand overshoot wanes

New Zealand ANZ Business Confidence dropped to -4.1 in March, comparing to preliminary reading at 0, and down from February’s 7. Own Activity Outlook dropped to 16.6 (prelim. at 17.4), down from 21.3. Export intentions dropped to 4.5, down from 5.1. Investment intentions dropped to 11.9, down from 15.6. Employment intentions rose to 14.4, up from 10.6. Pricing intentions rose to 47.3, up from 46.2.

ANZ said: “The March snap lockdowns make Business Outlook data a little harder to interpret. However, it is consistent with our view that as the demand overshoot wanes and the tourists are missed more and more, the economy will go largely sideways this year. The quicker cooling we now expect in the housing market plays into this theme as well. The vaccine rollout and the subsequent border re-opening will be game-changers, though it won’t be click-of-a-switch stuff. But there’s a path to the new normal, whatever precisely that looks like, and we’re on it. We’ll be keeping an eye on construction for possible bumps in the road.”

From Australia, private sector credit rose 0.2% mom in February. Building permits jumped 21.6% mom in February.

Fed officials optimistic on strong recovery ahead

Some Fed official expressed their optimism over the economic recovery ahead. Atlanta Fed President Raphael Bostic said, “we could see a burst of activity and performance coming into the summer which could lead us to see even more robust recovery.” He’s upbeat about the economy, as “a million jobs a month could become the standard through the summer.”

Richmond Fed President Thomas Barkin said he’s “bullish” on the economy this year. “People just have a lot of money in their pockets,” he said. The money will be spent as people are comfortable to go out again. that would help fuel growth into 2022 and 2023 too.

New York Fed President John Williams said he’s “optimism about the overall economy”, as “we’re making great strides on the vaccination program”. Also, “we have a lot of positives going forward.”

Fed Vice Chair Randal Quarles said he’s “one of the biggest optimist” on the economy. Yet, “we shouldn’t jump the gun. Let’s wait until we see those outcomes,” he added. “And clearly the performance of the macro economy, and the performance of monetary policy, not just over the last decade but really even 15, 20 years, would argue that that leads to superior outcomes.”

Looking ahead

UK GDP final, France CPI and consumer spending, Germany unemployment, Swiss economic expectations, and Eurozone CPI flash will be released in European session.

Later in the day, US will release ADP employment, Chicago PMI and pending home sales. Canada will release GDP, IPPI and RMPI.

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.92; (P) 110.18; (R1) 110.60; More…

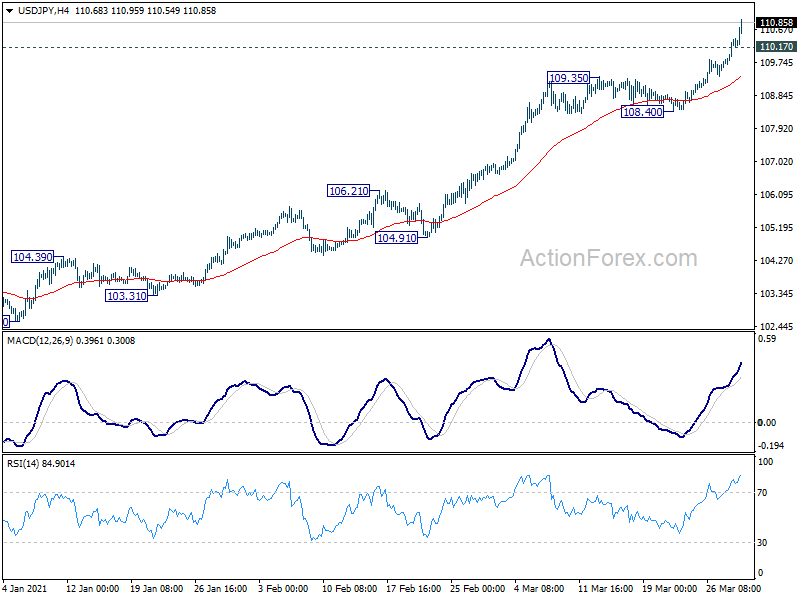

USD/JPY’s rise accelerates to as high as 110.95 so far. Intraday bias stays on the upside for 111.71/112.22 resistance. Firm break there will solidify medium term bullishness. On the downside, below 110.17 minor support will turn intraday bias neutral and bring consolidations first. But outlook will remain bullish as long as 108.40 support holds, in case of pull back.

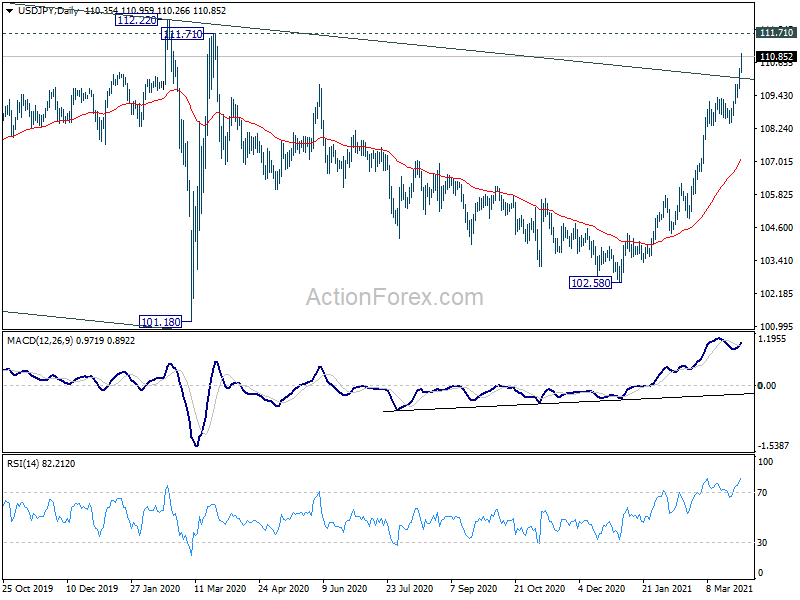

In the bigger picture, current development suggests that the corrective down trend from 118.65 (Dec 2016) has completed at 101.18. Firm break of 112.22 resistance should confirms this bullish case. A medium term up trend could then has started for 100% projection of 101.18 to 111.71 from 102.58 at 113.11 and then 161.8% projection at 119.61. Rejection by 111.71, however, will keep medium term outlook neutral first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Feb P | -2.10% | -1.30% | 4.30% | |

| 0:00 | NZD | ANZ Business Confidence Mar | -4.1 | 0 | ||

| 0:30 | AUD | Private Sector Credit M/M Feb | 0.20% | 0.30% | 0.20% | |

| 0:30 | AUD | Building Permits M/M Feb | 21.60% | 5.10% | -19.40% | |

| 1:00 | CNY | NBS Manufacturing PMI Mar | 51.9 | 51 | 50.6 | |

| 1:00 | CNY | Non-Manufacturing PMI Mar | 56.3 | 52.6 | 51.4 | |

| 5:00 | JPY | Housing Starts Y/Y Feb | -4.80% | -3.10% | ||

| 6:00 | GBP | GDP Q/Q Q4 F | 1.00% | 1.00% | ||

| 6:00 | GBP | Current Account (GBP) Q4 | -34.8B | -15.7B | ||

| 6:45 | EUR | France CPI M/M Mar P | 0.70% | 0.00% | ||

| 6:45 | EUR | France CPI Y/Y Mar P | 1.30% | 0.80% | ||

| 6:45 | EUR | France Consumer Spending M/M Feb | 0.70% | -4.60% | ||

| 7:55 | EUR | Germany Unemployment Change Feb | -5K | 9K | ||

| 7:55 | EUR | Germany Unemployment Rate s.a. Feb | 6.00% | 6.00% | ||

| 8:00 | CHF | Credit Suisse Economic Expectations Mar | 55.5 | |||

| 9:00 | EUR | Eurozone CPI Y/Y Mar P | 0.90% | 0.90% | ||

| 9:00 | EUR | Eurozone CPI Core Y/Y Mar P | 1.10% | 1.10% | ||

| 12:15 | USD | ADP Employment Change Mar | 550K | 117K | ||

| 12:30 | CAD | Industrial Product Price M/M Feb | 2.00% | |||

| 12:30 | CAD | Raw Material Price Index Feb | 5.70% | |||

| 12:30 | CAD | GDP M/M Jan | 0.10% | |||

| 13:45 | USD | Chicago PMI Mar | 60.3 | 59.5 | ||

| 14:00 | USD | Pending Home Sales M/M Feb | -2.60% | -2.80% | ||

| 14:30 | USD | Crude Oil Inventories | 1.9M |